Please answer the questions, Business development class

Please answer the questions, Business development class

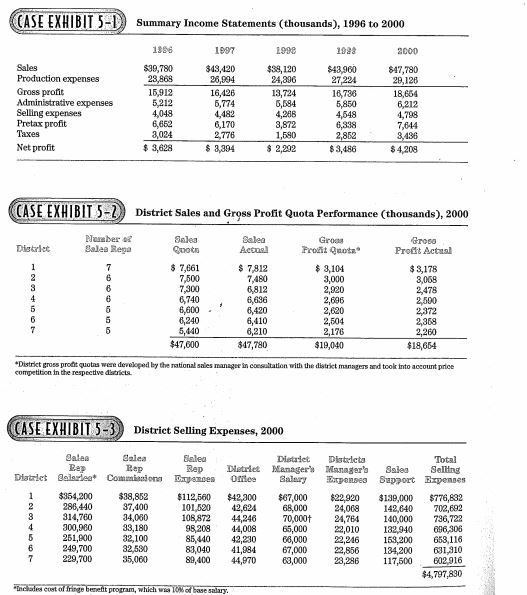

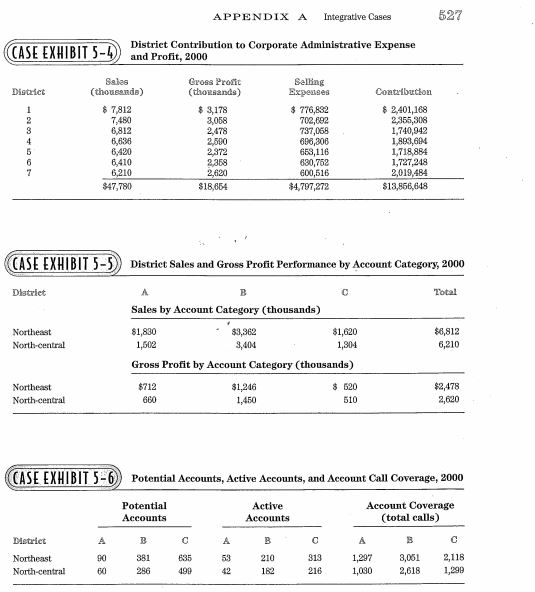

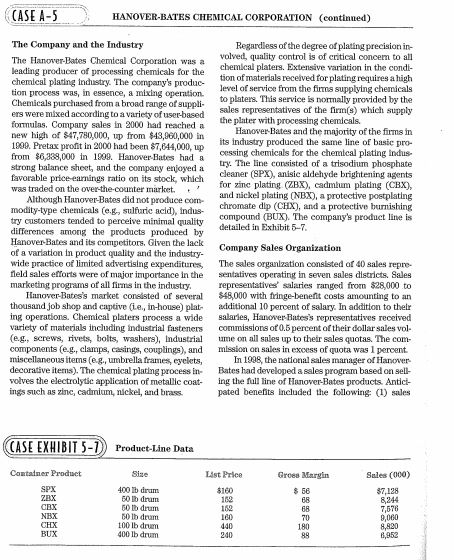

now someone with not much more than two years of selling experience and two years of pushing paper for the national sales manager at corporate headquarters tells me I'm not doing my job... Maybe it's time for me to look for a new job...and since Trumbull Chemical (Hanover-Bates's major competitor) is hiring, maybe that's where I should start looking ... and I'm not the only one who feels this way. Evaluating District Performance James Sprague, newly appointed northeast district sales manager for Hanover-Bates Chemical Corpo- ration, leaned back in his chair as the door to his office slammed shut. "Great beginning," he thought. "Three days into my new job and the dis- trict's most experienced sales representative is threatening to quit." On the previous night, James Sprague, Hank Carver (the district's most experienced sales rep- resentative), and John Follett, another senior member of the district sales staff, had met for din- ner at Jim's suggestion. During dinner, Jim had mentioned that one of his top priorities would be to conduct a sales and profit analysis of the dis- trict's business in order to identify opportunities to improve the district's performance. Jim had stated that he was confident that the analysis would indi- cate opportunities to reallocate district sales ef- forts in a manner that would increase profits. As Jirn had indicated during the conversation, "My ex- perience in analyzing district sales performance data for the national sales manager has convinced me that any district's allocation of sales effort to products and customer categories can be im- proved." Both Carver and Follett had nodded as Jim discussed his plans. Hank Carver was waiting when Jim arrived at the district sales office the next morning. It soon became apparent that Carver was very upset by what he perceived as Jim's criticism of how he and the other district sales representatives were doing their jobs-and more particularly, how they were allocating their time in terms of customers and products. As he concluded his heated comments, Carver had said: As Jim reflected on the scene that had just oc- curred, he wondered what he should do. It had been made clear to him when he had been pro- thoted to manager of the northeast sales district that one of his top priorities should be improve- ment of the district's performance. As the national sales manager had said, "The northeast sales dis- trict may rank third in dollar sales but it's our worst district in terms of profit performance." Prior to assuming his new position, Jim had assembled the data presented in Exhibits 5-1 through 5-7 to assist him in his work. The data had been compiled from records maintained in the national sales manager's office. Although he believed that the data would provide a sound ba- sis for a preliminary analysis of district perform- ance, Jim had recognized that additional data would probably have to be collected when he ar- rived in the northeast district (District 3). To pro- vide himself with a frame of reference, Jim had also requested data on the north-central sales dis- trict (District 7). This district was generally con- sidered to be one of the best, if not the best in the company. Furthermore, the north-central district sales manager, who was only three years older than Jim, was highly regarded by the national sales manager This company has made it damed clear that 34 years of experience don't count for anything... and CASE EXHIBIT 5-1 1396 $39,780 Sales Production expenses Gross pront Administrative expenses Selling expenses Pretax profit Taxes Net profit 15,912 5.212 4,048 6,652 3,024 $ 3,628 1997 343,420 26,994 16,426 5,714 4,482 6,170 2,776 $3,394 1998 $38,120 24,896 13,724 6,684 4.268 3,872 1,680 $2,222 2928 $43.900 27 224 16736 5,850 4,548 6,838 2,812 $3,486 2000 817,780 29,126 18 664 6.212 4,798 7.644 3,436 $4,209 CASE EXHIBIT 5-2) District Sales and Gross Profit Quota Performance (thousands), 2000 District Nestero Ja Rega Balea Accel Groc Prot Quote Groso Prodit Actual Coots $ 7,661 7,500 7.300 6,740 8,600 6,240 5,440 $47,600 $ 7,912 7.480 8,812 6,696 8,420 6,410 6.210 $17,780 $ 3,104 3,000 2,820 2.696 2.620 2,504 2,176 $19,040 $ 3,178 3,068 2,478 2.500 2372 2.319 2,260 $18,654 Distritos prot guotas were developed by the rational sales manager in cotation with the district an competition in the respective data d took into account price CASE EXHIBIT 5-3) District Selling Expenses, 2000 Dieta ax's penses Total Sale Saling Support Prpenses Baina Rep Dlatelet Bore $354,200 290 410 314,780 300,900 251,900 249,700 229,700 Balea Sales Rep Rep Commons Expenses $38,852 $112.560 37,000 BOL 520 34,060 108.872 33 180 98 208 32,100 85.400 32,530 83,040 35,000 89,400 Diet Dlatret Managers M orie teary $42,300 $67,000 2,624 68,000 70,000+ 44,008 65,000 4220 66,000 41,984 67,000 44,970 63,000 $22.920 24,068 24,764 22.010 22,246 22,856 23,286 $139,000 142,640 140,000 140,000 132940 153,200 134,200 117,500 $776,832 702,682 736,722 080306 6116 631 310 602.916 $4,797830 de con trol, which w asesale APPENDIX A Integrative Cases 527 (CASE EXHIBIT)-9 CASE EXHIBIT 5-4) District Contribution to Corporate Administrative Expense and Profit, 2000 District Sales (thousands) Gross Profit (thousands) Selling Expenses $ 3.178 3058 2.678 6 7812 7.480 6.812 6.638 6.420 1410 6210 $47,780 2500 2.372 2.358 $ 776,832 702.682 737,066 620,306 653,116 630,762 600,516 $4,707,272 Contbucion $2.401.16 2,355,308 1,740,942 1.888.614 1.718.884 1,727,248 2,019,484 $13,856,648 2.630 $18,654 CASE EXHIBIT 5-5) District Sales and Gross Profit Performance by Account Category, 2000 Dlatret Total Sales by Account Category (thousands) Northeast North-central $1,830 1,502 $3,362 3,404 81,620 1,304 $4,812 6,210 Gross Profit by Account Category (thousands) Northeast North-central $712 680 $1,216 1,450 $ 620 510 $2,478 2,620 (CASE EXHIBIT 5-6 Potential Accounts, Active Accounts, and Account Call Coverage, 2000 Potential Accounts Active Accounts Account Coverage (total calls) District Northeast North-central BCA B 381 635 53 210 256 499 42 1 62 1 313 216 ,207 1,030 3,061 2,618 2,118 1,299 60 CASE A-5 HANOVER-BATES CHEMICAL CORPORATION (continued) The Company and the Industry Regardless of the degree of plating precision in- volved quality control is of critical concem to all The Hanover-Bates Chemical Corporation was a chemical platers. Extensive variation in the condi- leading producer of processing chemicals for the tion of materials received for plating requires a high chemical plating Industry. The company's produc- level of service from the firm supplying chemicals tion process was, in essence, & mixing operation. Chemicals purchased from a broad range of suppli- to platers. This service is normally provided by the sales representatives of the firm(s) which supply ers were mixed according to a variety of user-based the plater with processing chemicals formulas, Company sales in 2000 had reached a new high of $47,780,000, up from $49,960,000 in Hanover Bates and the majority of the firms in its industry produced the same line of basic pro- 1999. Pretax profit in 2000 had been $7,644,000, up cessing chemicals for the chemical plating Indus from $6,339,000 in 1909. Hanower Hates had a try. The line consisted of a trisodium phosphate strong balance sheet, and the company enjoyed a cleaner (SPX anisic aldehyde brightening agents favorable price earnings ratio on its stock, which for zinc plating (ZBX), cadmium plating (CBX) was traded on the over-the-counter market. ? Although Hanover-Bates did not produce com and nickel plating (NBX), a protective postplating chromate dip (CHX), and a protective burnishing modity-type chemicals (eg, sulfuric acid), indus- compound (BUX). The company's product line is try customers tended to perceive minimal quality detailed in xhibit 5-7 differences among the products produced by Hanover Bates and its competitors. Given the lack Company Sales Organization of a variation in product quality and the industry- wide practice of limited advertising expenditures, The sales organization consisted of 40 sales repre- fleld sales efforts were of major iniportance in the sentatives operating in seven sales districts. Sales marketing programs of all firms in the industry, representatives' salaries ranged from $28,000 to Tanaver-Rates's market consisted of several $48,000 with fringe-benent costs amounting to an thousand job shop and captive (ie, in-house) plat aditional 10 percent of salary. In addition to their ing operations, Chemical platers process a wide salles, Hanover Bates's representatives received variety of materials including industrial tenen commissions op0.5 percent of their dollar sales vol- (e.g.. screws, rivets, bolts, washery), Industrial ume on all sales up to their sales quotas. The com- components (e.g., clamps, Casings, couplings, and mission on sales in excess of ouota was 1 percent miscellaneous items (eg, umbrella frames, eyelets. In 1998, the national sales manager of Hanover decorative items). The chemical plating process in Bates had developed a sales program based on sell- wolves the electrolytic application of metallic conting the fall line of Hanover-Bates products. Antici- ings such as zinc, cadmium, nickel, and brass. pated benefits included the following: (1) sales CASE EXHIBIT 5-1 Product-Line Data Container Product List Price Gross Margin Sales (000) $ 58 37.128 ZBX CBX NEX 400 lb drum Both drum Both drum O ih drum 100 lb drum 400 lb drum CHX 9.000 8,890 2,852 BUX APPENDIX A Integrative Cases 529 volume per account would be greater and selling costs as a percentage of sales would decrease; (2) a Hanover-Bates sales representative could justify spending more time with such an account, thus be- coming more lanowledgeable about the account's business and better able to provide technical assis tance and identify selling opportunities; (3) full-line sales would strengthen Hanover-Bates's competi- tive position by reducing the likelihood of account loss to other plating chemical suppliers (a problem that existed in multiple supplier situations). The national sales manager's 1998 sales pro. gram had also included the following account call frequency guidelines: A accounts (major accounts generating $24,000 or more in yearly sales)-two calls per month; B accounts (medium-sized ac counts generating $12,000 to $23,999 in yearly sales)-one call per month; Caccounts (small ac counts generating less than $12,000 yearly in sales)-one call every two months. The account call frequency guidelines were developed by the national sales manager after discussions with the district managers. The national sales manager had been concerned about the optimum allocation of sales efforts to accounts and felt that the guide lines would increase the efficiency of the com- pany's sales force, although not all of the district sales managers agreed with this conclusion It was common knowledge in Hanover-Bates's corporate sales office that Jim Sprague's predecey sor as northeast district sales manager had not been one of the company's better district sales managers. His attitude toward the sales plans and programs of the national sales manager had been one of reluctant compliance rather than accept ance and support. When the national sales man ager succeeded in persuading Jim Sprague's pred- ecessor to take early retirement, he had been faced with the lack of an available qualified replacement, Although most of the sales representatives had assumed Hank Carver would get the district manager's job, he had been passed over in part be- cause he would be 65 in three years. The national sales manager had not wanted to face the same replacement problem again in three years and had wanted someone in the position who would be more likely to be responsive to the company's sales plans and policies. The appointment of Jim Sprague as district manager had caused consider- able talk, not only in the district but also at corpo- rate headquarters. In fact, the national sales man- ager had warned Jim that "a lot of people are expecting you to fall on your face. They don't think you have the experience to handle the job, and in particular, to manage and motivate a group of sales representatives most of whom are consid- erably older and more experienced than you." The national sales manager had concluded by saying, "I think you can handle the job, Jim. I think you can manage those sales reps and improve the dis trict's profit performance, and I'm depending on you to do both." Questions: 1. Evaluate the performance of the northeast dis- trict in comparison with the other Hanover Bates sales districts. 2. What are the weak spots in the northeast dis- trict's performance? 8. What should management do to improve areas of poor performance in the northeast district? now someone with not much more than two years of selling experience and two years of pushing paper for the national sales manager at corporate headquarters tells me I'm not doing my job... Maybe it's time for me to look for a new job...and since Trumbull Chemical (Hanover-Bates's major competitor) is hiring, maybe that's where I should start looking ... and I'm not the only one who feels this way. Evaluating District Performance James Sprague, newly appointed northeast district sales manager for Hanover-Bates Chemical Corpo- ration, leaned back in his chair as the door to his office slammed shut. "Great beginning," he thought. "Three days into my new job and the dis- trict's most experienced sales representative is threatening to quit." On the previous night, James Sprague, Hank Carver (the district's most experienced sales rep- resentative), and John Follett, another senior member of the district sales staff, had met for din- ner at Jim's suggestion. During dinner, Jim had mentioned that one of his top priorities would be to conduct a sales and profit analysis of the dis- trict's business in order to identify opportunities to improve the district's performance. Jim had stated that he was confident that the analysis would indi- cate opportunities to reallocate district sales ef- forts in a manner that would increase profits. As Jirn had indicated during the conversation, "My ex- perience in analyzing district sales performance data for the national sales manager has convinced me that any district's allocation of sales effort to products and customer categories can be im- proved." Both Carver and Follett had nodded as Jim discussed his plans. Hank Carver was waiting when Jim arrived at the district sales office the next morning. It soon became apparent that Carver was very upset by what he perceived as Jim's criticism of how he and the other district sales representatives were doing their jobs-and more particularly, how they were allocating their time in terms of customers and products. As he concluded his heated comments, Carver had said: As Jim reflected on the scene that had just oc- curred, he wondered what he should do. It had been made clear to him when he had been pro- thoted to manager of the northeast sales district that one of his top priorities should be improve- ment of the district's performance. As the national sales manager had said, "The northeast sales dis- trict may rank third in dollar sales but it's our worst district in terms of profit performance." Prior to assuming his new position, Jim had assembled the data presented in Exhibits 5-1 through 5-7 to assist him in his work. The data had been compiled from records maintained in the national sales manager's office. Although he believed that the data would provide a sound ba- sis for a preliminary analysis of district perform- ance, Jim had recognized that additional data would probably have to be collected when he ar- rived in the northeast district (District 3). To pro- vide himself with a frame of reference, Jim had also requested data on the north-central sales dis- trict (District 7). This district was generally con- sidered to be one of the best, if not the best in the company. Furthermore, the north-central district sales manager, who was only three years older than Jim, was highly regarded by the national sales manager This company has made it damed clear that 34 years of experience don't count for anything... and CASE EXHIBIT 5-1 1396 $39,780 Sales Production expenses Gross pront Administrative expenses Selling expenses Pretax profit Taxes Net profit 15,912 5.212 4,048 6,652 3,024 $ 3,628 1997 343,420 26,994 16,426 5,714 4,482 6,170 2,776 $3,394 1998 $38,120 24,896 13,724 6,684 4.268 3,872 1,680 $2,222 2928 $43.900 27 224 16736 5,850 4,548 6,838 2,812 $3,486 2000 817,780 29,126 18 664 6.212 4,798 7.644 3,436 $4,209 CASE EXHIBIT 5-2) District Sales and Gross Profit Quota Performance (thousands), 2000 District Nestero Ja Rega Balea Accel Groc Prot Quote Groso Prodit Actual Coots $ 7,661 7,500 7.300 6,740 8,600 6,240 5,440 $47,600 $ 7,912 7.480 8,812 6,696 8,420 6,410 6.210 $17,780 $ 3,104 3,000 2,820 2.696 2.620 2,504 2,176 $19,040 $ 3,178 3,068 2,478 2.500 2372 2.319 2,260 $18,654 Distritos prot guotas were developed by the rational sales manager in cotation with the district an competition in the respective data d took into account price CASE EXHIBIT 5-3) District Selling Expenses, 2000 Dieta ax's penses Total Sale Saling Support Prpenses Baina Rep Dlatelet Bore $354,200 290 410 314,780 300,900 251,900 249,700 229,700 Balea Sales Rep Rep Commons Expenses $38,852 $112.560 37,000 BOL 520 34,060 108.872 33 180 98 208 32,100 85.400 32,530 83,040 35,000 89,400 Diet Dlatret Managers M orie teary $42,300 $67,000 2,624 68,000 70,000+ 44,008 65,000 4220 66,000 41,984 67,000 44,970 63,000 $22.920 24,068 24,764 22.010 22,246 22,856 23,286 $139,000 142,640 140,000 140,000 132940 153,200 134,200 117,500 $776,832 702,682 736,722 080306 6116 631 310 602.916 $4,797830 de con trol, which w asesale APPENDIX A Integrative Cases 527 (CASE EXHIBIT)-9 CASE EXHIBIT 5-4) District Contribution to Corporate Administrative Expense and Profit, 2000 District Sales (thousands) Gross Profit (thousands) Selling Expenses $ 3.178 3058 2.678 6 7812 7.480 6.812 6.638 6.420 1410 6210 $47,780 2500 2.372 2.358 $ 776,832 702.682 737,066 620,306 653,116 630,762 600,516 $4,707,272 Contbucion $2.401.16 2,355,308 1,740,942 1.888.614 1.718.884 1,727,248 2,019,484 $13,856,648 2.630 $18,654 CASE EXHIBIT 5-5) District Sales and Gross Profit Performance by Account Category, 2000 Dlatret Total Sales by Account Category (thousands) Northeast North-central $1,830 1,502 $3,362 3,404 81,620 1,304 $4,812 6,210 Gross Profit by Account Category (thousands) Northeast North-central $712 680 $1,216 1,450 $ 620 510 $2,478 2,620 (CASE EXHIBIT 5-6 Potential Accounts, Active Accounts, and Account Call Coverage, 2000 Potential Accounts Active Accounts Account Coverage (total calls) District Northeast North-central BCA B 381 635 53 210 256 499 42 1 62 1 313 216 ,207 1,030 3,061 2,618 2,118 1,299 60 CASE A-5 HANOVER-BATES CHEMICAL CORPORATION (continued) The Company and the Industry Regardless of the degree of plating precision in- volved quality control is of critical concem to all The Hanover-Bates Chemical Corporation was a chemical platers. Extensive variation in the condi- leading producer of processing chemicals for the tion of materials received for plating requires a high chemical plating Industry. The company's produc- level of service from the firm supplying chemicals tion process was, in essence, & mixing operation. Chemicals purchased from a broad range of suppli- to platers. This service is normally provided by the sales representatives of the firm(s) which supply ers were mixed according to a variety of user-based the plater with processing chemicals formulas, Company sales in 2000 had reached a new high of $47,780,000, up from $49,960,000 in Hanover Bates and the majority of the firms in its industry produced the same line of basic pro- 1999. Pretax profit in 2000 had been $7,644,000, up cessing chemicals for the chemical plating Indus from $6,339,000 in 1909. Hanower Hates had a try. The line consisted of a trisodium phosphate strong balance sheet, and the company enjoyed a cleaner (SPX anisic aldehyde brightening agents favorable price earnings ratio on its stock, which for zinc plating (ZBX), cadmium plating (CBX) was traded on the over-the-counter market. ? Although Hanover-Bates did not produce com and nickel plating (NBX), a protective postplating chromate dip (CHX), and a protective burnishing modity-type chemicals (eg, sulfuric acid), indus- compound (BUX). The company's product line is try customers tended to perceive minimal quality detailed in xhibit 5-7 differences among the products produced by Hanover Bates and its competitors. Given the lack Company Sales Organization of a variation in product quality and the industry- wide practice of limited advertising expenditures, The sales organization consisted of 40 sales repre- fleld sales efforts were of major iniportance in the sentatives operating in seven sales districts. Sales marketing programs of all firms in the industry, representatives' salaries ranged from $28,000 to Tanaver-Rates's market consisted of several $48,000 with fringe-benent costs amounting to an thousand job shop and captive (ie, in-house) plat aditional 10 percent of salary. In addition to their ing operations, Chemical platers process a wide salles, Hanover Bates's representatives received variety of materials including industrial tenen commissions op0.5 percent of their dollar sales vol- (e.g.. screws, rivets, bolts, washery), Industrial ume on all sales up to their sales quotas. The com- components (e.g., clamps, Casings, couplings, and mission on sales in excess of ouota was 1 percent miscellaneous items (eg, umbrella frames, eyelets. In 1998, the national sales manager of Hanover decorative items). The chemical plating process in Bates had developed a sales program based on sell- wolves the electrolytic application of metallic conting the fall line of Hanover-Bates products. Antici- ings such as zinc, cadmium, nickel, and brass. pated benefits included the following: (1) sales CASE EXHIBIT 5-1 Product-Line Data Container Product List Price Gross Margin Sales (000) $ 58 37.128 ZBX CBX NEX 400 lb drum Both drum Both drum O ih drum 100 lb drum 400 lb drum CHX 9.000 8,890 2,852 BUX APPENDIX A Integrative Cases 529 volume per account would be greater and selling costs as a percentage of sales would decrease; (2) a Hanover-Bates sales representative could justify spending more time with such an account, thus be- coming more lanowledgeable about the account's business and better able to provide technical assis tance and identify selling opportunities; (3) full-line sales would strengthen Hanover-Bates's competi- tive position by reducing the likelihood of account loss to other plating chemical suppliers (a problem that existed in multiple supplier situations). The national sales manager's 1998 sales pro. gram had also included the following account call frequency guidelines: A accounts (major accounts generating $24,000 or more in yearly sales)-two calls per month; B accounts (medium-sized ac counts generating $12,000 to $23,999 in yearly sales)-one call per month; Caccounts (small ac counts generating less than $12,000 yearly in sales)-one call every two months. The account call frequency guidelines were developed by the national sales manager after discussions with the district managers. The national sales manager had been concerned about the optimum allocation of sales efforts to accounts and felt that the guide lines would increase the efficiency of the com- pany's sales force, although not all of the district sales managers agreed with this conclusion It was common knowledge in Hanover-Bates's corporate sales office that Jim Sprague's predecey sor as northeast district sales manager had not been one of the company's better district sales managers. His attitude toward the sales plans and programs of the national sales manager had been one of reluctant compliance rather than accept ance and support. When the national sales man ager succeeded in persuading Jim Sprague's pred- ecessor to take early retirement, he had been faced with the lack of an available qualified replacement, Although most of the sales representatives had assumed Hank Carver would get the district manager's job, he had been passed over in part be- cause he would be 65 in three years. The national sales manager had not wanted to face the same replacement problem again in three years and had wanted someone in the position who would be more likely to be responsive to the company's sales plans and policies. The appointment of Jim Sprague as district manager had caused consider- able talk, not only in the district but also at corpo- rate headquarters. In fact, the national sales man- ager had warned Jim that "a lot of people are expecting you to fall on your face. They don't think you have the experience to handle the job, and in particular, to manage and motivate a group of sales representatives most of whom are consid- erably older and more experienced than you." The national sales manager had concluded by saying, "I think you can handle the job, Jim. I think you can manage those sales reps and improve the dis trict's profit performance, and I'm depending on you to do both." Questions: 1. Evaluate the performance of the northeast dis- trict in comparison with the other Hanover Bates sales districts. 2. What are the weak spots in the northeast dis- trict's performance? 8. What should management do to improve areas of poor performance in the northeast district