Answered step by step

Verified Expert Solution

Question

1 Approved Answer

please answer the uploaded question. Time Value of Money Analysis Retirement Planning, Inc. 1 Mike Abbott, president of Retirement Planning, Inc., was delighted to receive

please answer the uploaded question.

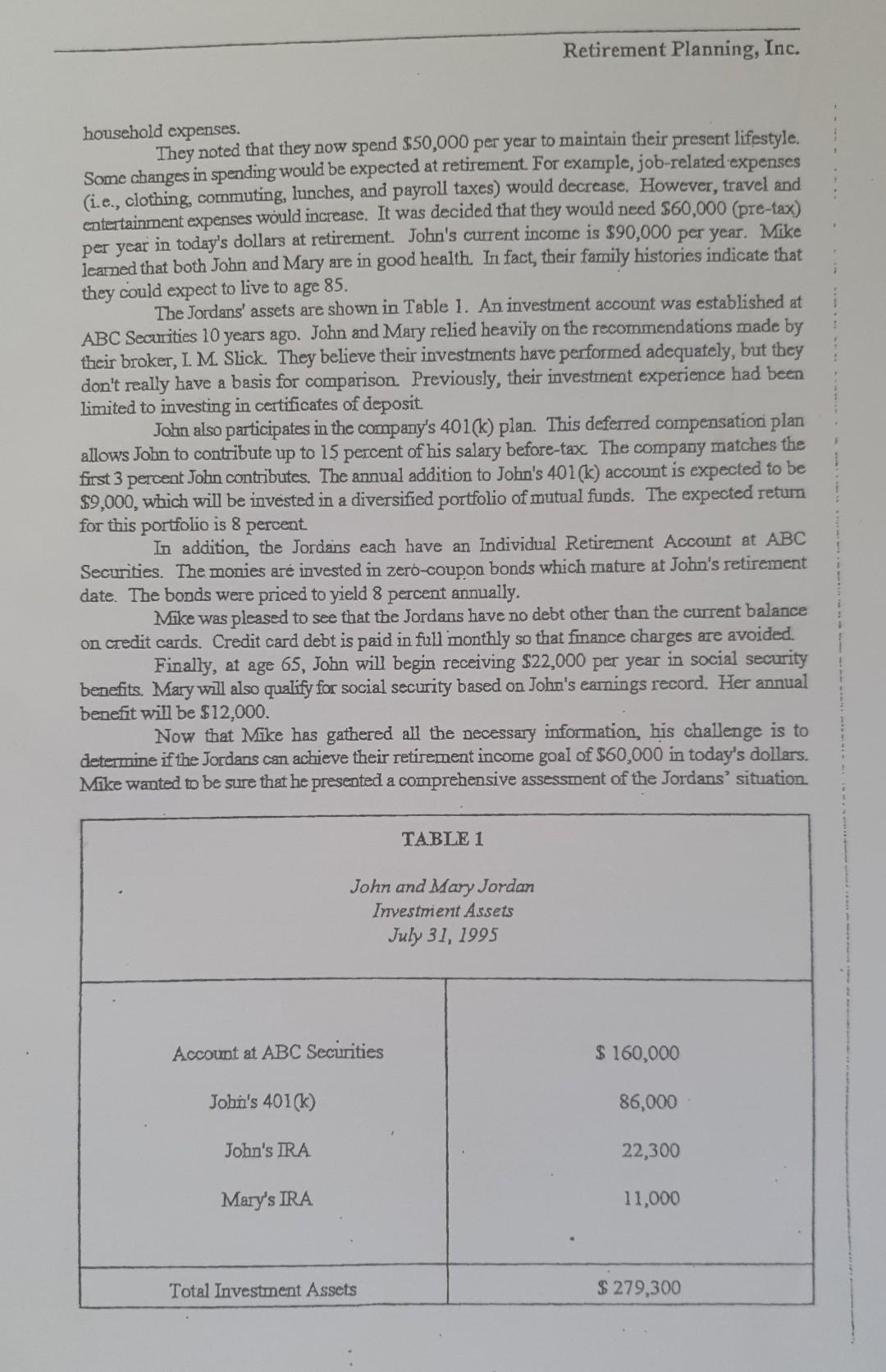

Time Value of Money Analysis Retirement Planning, Inc. 1 Mike Abbott, president of Retirement Planning, Inc., was delighted to receive a call from John Jordan. John had been referred by Joe Jones, a local CPA. John was interested in planning for retirement. He had saved consistently over the years and participated in a company-sponsored retirement plan, John was not sure how comfortable he would be during his retirement years. Mike and John agreed to meet the following Monday to review John's finances. It was agreed that John's wife, Mary, would also attend the meeting. Mike's fimm specializes in personal financial planning. The firm has developed a great deal of expertise in helping individuals develop comprehensive strategies for retirement. This area has proven to be very lucrative with the growing public awareness of the need to begin planning and saving for retirement as soon as possible. The objective of the initial client meeting was to obtain background information, explain the services offered by the firm, and discuss the fees for those services. During this meeting, Mike learned that John and Mary were both 62 years old. John is currently the vice president of marketing for EFC, Inc., a midsized manufacturing company. He has been with the company for 22 years. Mary is a homemaker. Mike asked John and Mary to describe their retirement objective. John said, "I'd like to retire in three years at age 65 and be comfortable. We want to be able to travel and spend time with our grandchildren. We also want to be able to spend a great deal of time on the golf course." It was obvious to Mike that John and Mary had not fully formulated their retirement goals. This was a common occurrence; most clients Mike met with did not have a clear retirement objective established. To plan effectively for retirement, the following factors must be quantified: Target retirement age. Desired retirement income. Estimated life expectancy. Expected rate of inflation over the planning period. John and Mary had established their target retirement age but did not have a specific income. goal in mind. Moreover, they were wosure how to address this question. Mike suggested that they review their current spending patterns. By reviewing their checkbook register for the prior 12 months, John and Mary were able to document how much they spent for food, clothing, travel, entertainment, and other Retirement Planning, Inc. household expenses. They noted that they now spend $50,000 per year to maintain their present lifestyle. Some changes in spending would be expected at retirement For example, job-related expenses (i.e., clothing, commuting, lunches, and payroll taxes) would decrease. However, travel and entertainment expenses would increase. It was decided that they would need $60,000 (pre-tax) per year in today's dollars at retirement. John's current income is $90,000 per year. Mike learned that both John and Mary are in good health. In fact, their family histories indicate that they could expect to live to age 85. The Jordans' assets are shown in Table 1. An investment account was established at ABC Seanities 10 years ago. John and Mary relied heavily on the recommendations made by their broker, I. M. Slick. They believe their investinents have performed adequately, but they don't really have a basis for comparison Previously, their investinent experience had been limited to investing in certificates of deposit John also participates in the company's 401(k) plan. This deferred compensation plan allows John to contribute up to 15 percent of his salary before-tax. The company matches the first 3 percent John contributes. The annual addition to John's 401(k) account is expected to be $9,000, which will be invested in a diversified portfolio of mutual funds. The expected retum for this portfolio is 8 percent In addition, the Jordans each have an Individual Retirement Account at ABC Securities. The monies are invested in zero-coupon bonds which mature at John's retirement date. The bonds were priced to yield 8 percent annually. Mike was pleased to see that the Jordans have no debt other than the current balance on credit cards. Credit card debt is paid in full monthly so that finance charges are avoided. Finally, at age 65, John will begin receiving $22,000 per year in social security benefits. Mary will also qualify for social security based on John's earnings record. Her annual benefit will be $12,000. Now that Mike has gathered all the necessary information, his challenge is to determine if the Jordans can achieve their retirement income goal of $60,000 in today's dollars. Mike wanted to be sure that he presented a comprehensive assessment of the Jordans' situation TABLE 1 John and Mary Jordan Investment Assets July 31, 1995 Account at ABC Securities $ 160,000 Jobi's 401(k) 86,000 John's TRA 22,300 Mary's IRA 11,000 Total Investment Assets $ 279,300 6. What will the 401(k) grow to on July 31, 1998, assuming an 8 percent annual return? Remember to take into account the annual additions made at the end of each year. urity benefits the lordans will Time Value of Money Analysis Retirement Planning, Inc. 1 Mike Abbott, president of Retirement Planning, Inc., was delighted to receive a call from John Jordan. John had been referred by Joe Jones, a local CPA. John was interested in planning for retirement. He had saved consistently over the years and participated in a company-sponsored retirement plan, John was not sure how comfortable he would be during his retirement years. Mike and John agreed to meet the following Monday to review John's finances. It was agreed that John's wife, Mary, would also attend the meeting. Mike's fimm specializes in personal financial planning. The firm has developed a great deal of expertise in helping individuals develop comprehensive strategies for retirement. This area has proven to be very lucrative with the growing public awareness of the need to begin planning and saving for retirement as soon as possible. The objective of the initial client meeting was to obtain background information, explain the services offered by the firm, and discuss the fees for those services. During this meeting, Mike learned that John and Mary were both 62 years old. John is currently the vice president of marketing for EFC, Inc., a midsized manufacturing company. He has been with the company for 22 years. Mary is a homemaker. Mike asked John and Mary to describe their retirement objective. John said, "I'd like to retire in three years at age 65 and be comfortable. We want to be able to travel and spend time with our grandchildren. We also want to be able to spend a great deal of time on the golf course." It was obvious to Mike that John and Mary had not fully formulated their retirement goals. This was a common occurrence; most clients Mike met with did not have a clear retirement objective established. To plan effectively for retirement, the following factors must be quantified: Target retirement age. Desired retirement income. Estimated life expectancy. Expected rate of inflation over the planning period. John and Mary had established their target retirement age but did not have a specific income. goal in mind. Moreover, they were wosure how to address this question. Mike suggested that they review their current spending patterns. By reviewing their checkbook register for the prior 12 months, John and Mary were able to document how much they spent for food, clothing, travel, entertainment, and other Retirement Planning, Inc. household expenses. They noted that they now spend $50,000 per year to maintain their present lifestyle. Some changes in spending would be expected at retirement For example, job-related expenses (i.e., clothing, commuting, lunches, and payroll taxes) would decrease. However, travel and entertainment expenses would increase. It was decided that they would need $60,000 (pre-tax) per year in today's dollars at retirement. John's current income is $90,000 per year. Mike learned that both John and Mary are in good health. In fact, their family histories indicate that they could expect to live to age 85. The Jordans' assets are shown in Table 1. An investment account was established at ABC Seanities 10 years ago. John and Mary relied heavily on the recommendations made by their broker, I. M. Slick. They believe their investinents have performed adequately, but they don't really have a basis for comparison Previously, their investinent experience had been limited to investing in certificates of deposit John also participates in the company's 401(k) plan. This deferred compensation plan allows John to contribute up to 15 percent of his salary before-tax. The company matches the first 3 percent John contributes. The annual addition to John's 401(k) account is expected to be $9,000, which will be invested in a diversified portfolio of mutual funds. The expected retum for this portfolio is 8 percent In addition, the Jordans each have an Individual Retirement Account at ABC Securities. The monies are invested in zero-coupon bonds which mature at John's retirement date. The bonds were priced to yield 8 percent annually. Mike was pleased to see that the Jordans have no debt other than the current balance on credit cards. Credit card debt is paid in full monthly so that finance charges are avoided. Finally, at age 65, John will begin receiving $22,000 per year in social security benefits. Mary will also qualify for social security based on John's earnings record. Her annual benefit will be $12,000. Now that Mike has gathered all the necessary information, his challenge is to determine if the Jordans can achieve their retirement income goal of $60,000 in today's dollars. Mike wanted to be sure that he presented a comprehensive assessment of the Jordans' situation TABLE 1 John and Mary Jordan Investment Assets July 31, 1995 Account at ABC Securities $ 160,000 Jobi's 401(k) 86,000 John's TRA 22,300 Mary's IRA 11,000 Total Investment Assets $ 279,300 6. What will the 401(k) grow to on July 31, 1998, assuming an 8 percent annual return? Remember to take into account the annual additions made at the end of each year. urity benefits the lordans willStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Handbook Of Financial Intermediation And Banking

Authors: Anjan V. Thakor, Arnoud Boot

1st Edition

0444515585, 978-0444515582