Answered step by step

Verified Expert Solution

Question

1 Approved Answer

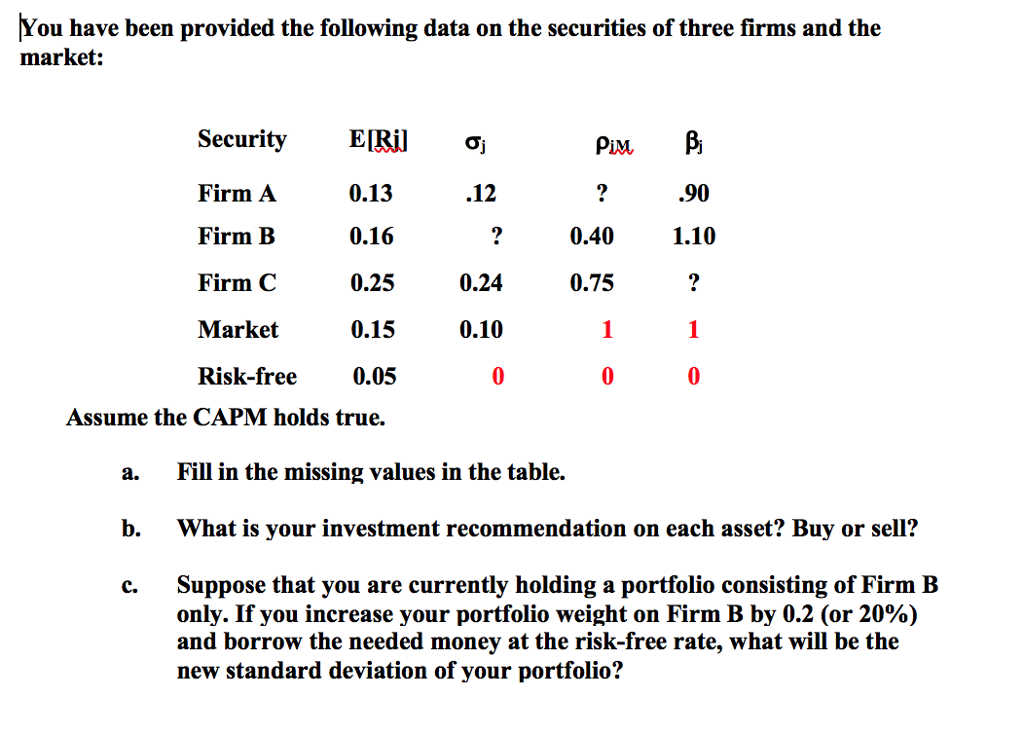

Please be specific, answer all parts step by step, and show the formula you use. Thank you! You have been provided the following data on

Please be specific, answer all parts step by step, and show the formula you use. Thank you!

Please be specific, answer all parts step by step, and show the formula you use. Thank you!

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Mathematics Of Finance

Authors: Robert Brown, Steve Kopp, Petr Zima

8th Edition

0070876460, 978-0070876460