Answered step by step

Verified Expert Solution

Question

1 Approved Answer

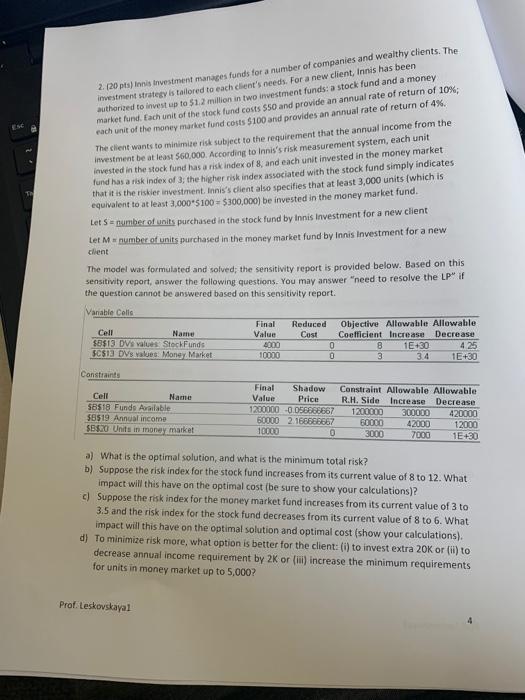

please can you answer this questions? TE 2. (20 pts) Insinvestment manages funds for a number of companies and wealthy clients. The investment strategy is

please can you answer this questions?

TE 2. (20 pts) Insinvestment manages funds for a number of companies and wealthy clients. The investment strategy is allored to each client's needs. For a new client, Innis has been authorized to invest up to $1.2 million in two investment funds: a stock fund and a money market fund. Each unit of the stock fund costs $50 and provide an annual rate of return of 10%; nach unit of the money market fund costs $100 and provides an annual rate of return of 4%. The client wants to minimise risk subject to the requirement that the annual income from the Investment be at least 560,000. According to Innis's risk measurement system, each unit invested in the stock fund has a risk index of 8, and each unit invested in the money market fund has a risk index of 3, the higher risk index associated with the stock fund simply indicates that it is the riskier investment. Innis's client also specifies that at least 3,000 units (which is equivalent to at least 3,000 5100 = $300,000) be invested in the money market fund. Let S = number of units purchased in the stock fund by Innis Investment for a new client Let M a number of units purchased in the money market fund by Innis Investment for a new client The model was formulated and solved; the sensitivity report is provided below. Based on this sensitivity report, answer the following questions. You may answer "need to resolve the LP" if the question cannot be answered based on this sensitivity report. Variable Calls Final Reduced Objective Allowable Allowable Cell Value Cost Coefficient Increase Decrease $8$13 Dve values Stock Funds 4000 0 8. 1E30 4.25 $C$12 DVS values. Mong Market 10000 0 3 3.4 1E+30 Name Constraints Cell Name 58518 Fundo Aailable $8519 Annual income $B$ Units in money market Final Shadow Constraint Allowable Allowable Value Price R.H. Side Increase Decrease 1200000 0.056888667 1200000 300000 420000 60000 2.166666667 60000 42000 12000 10000 0 3000 7800 1E+30 a) What is the optimal solution, and what is the minimum total risk? b) Suppose the risk index for the stock fund increases from its current value of 8 to 12. What impact will this have on the optimal cost (be sure to show your calculations)? c) Suppose the risk index for the money market fund increases from its current value of 3 to 3.5 and the risk index for the stock fund decreases from its current value of 8 to What impact will this have on the optimal solution and optimal cost (show your calculations). d) To minimize risk more, what option is better for the client: (i) to invest extra 20K or (ii) to decrease annual income requirement by 2K or (ii) increase the minimum requirements for units in money market up to 5,000? Prof. Leskovskayal Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Dynamical Corporate Finance

Authors: Umberto Sagliaschi, Roberto Savona

1st Edition

3030778525, 9783030778521