Answered step by step

Verified Expert Solution

Question

1 Approved Answer

please discuss this in two full paragraphs veld-schemes Pay Refunds Credits & Deductions Forms & Instructions Search English Espaol Abusive tax schemes have evolved from

please discuss this in two full paragraphs

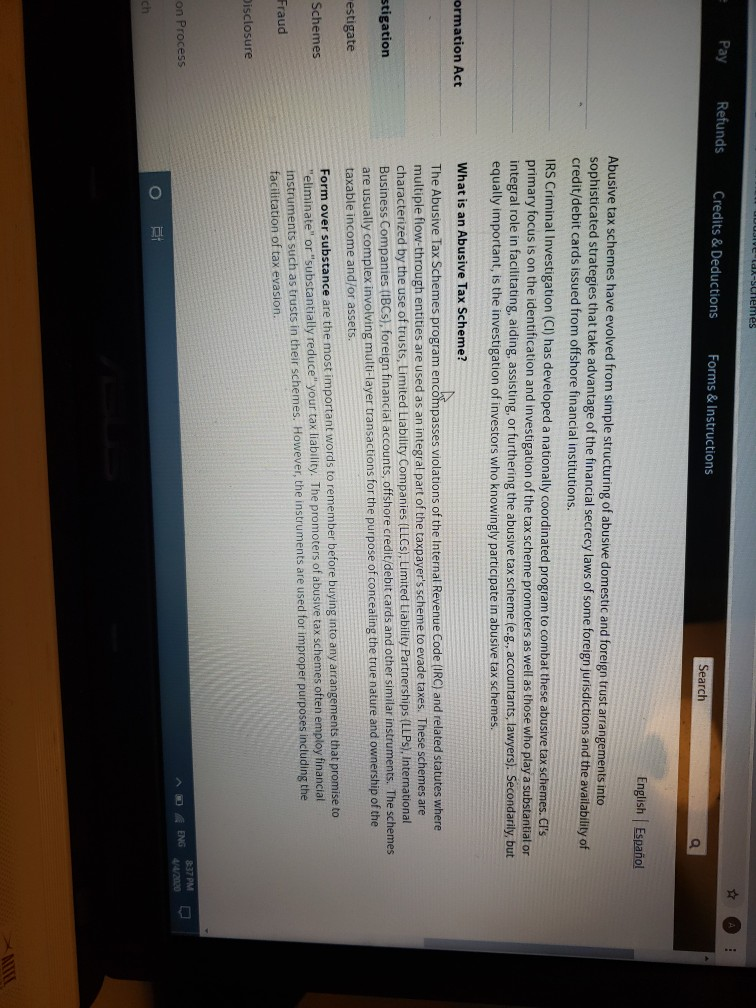

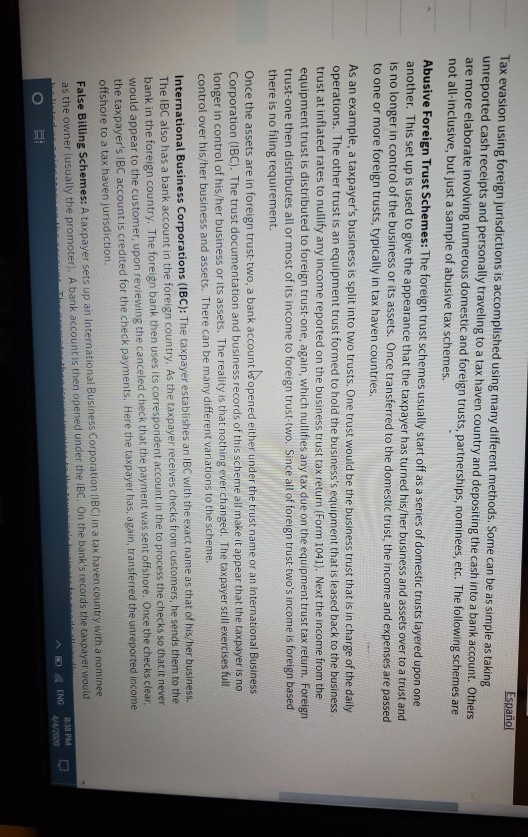

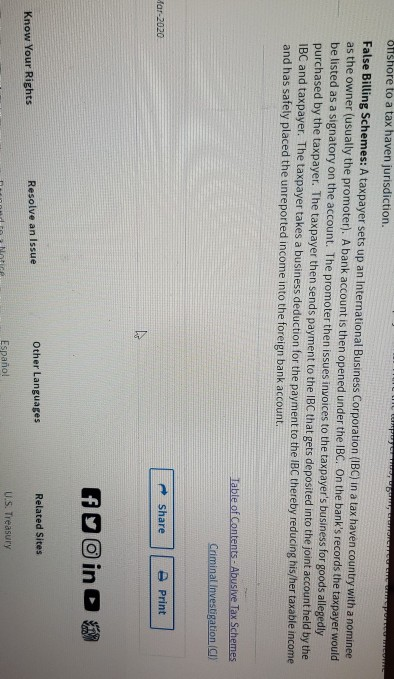

veld-schemes Pay Refunds Credits & Deductions Forms & Instructions Search English Espaol Abusive tax schemes have evolved from simple structuring of abusive domestic and foreign trust arrangements into sophisticated strategies that take advantage of the financial secrecy laws of some foreign jurisdictions and the availability of credit/debit cards issued from offshore financial institutions. IRS Criminal Investigation (CI) has developed a nationally coordinated program to combat these abusive tax schemes. Ci's primary focus is on the identification and investigation of the tax scheme promoters as well as those who play a substantial or integral role in facilitating, aiding, assisting, or furthering the abusive tax scheme (e.g., accountants, lawyers). Secondarily, but equally important, is the investigation of investors who knowingly participate in abusive tax schemes. ormation Act What is an Abusive Tax Scheme? stigation estigate The Abusive Tax Schemes program encompasses violations of the Internal Revenue Code (IRC) and related statutes where multiple flow-through entities are used as an integral part of the taxpayer's scheme to evade taxes. These schemes are characterized by the use of trusts, Limited Liability Companies (LLCs), Limited Liability Partnerships (LLPs), International Business Companies (IBCS), foreign financial accounts, offshore credit/debit cards and other similar instruments. The schemes are usually complex involving multi-layer transactions for the purpose of concealing the true nature and ownership of the taxable income and/or assets. Form over substance are the most important words to remember before buying into any arrangements that promise to "eliminate" or "substantially reduce your tax liability. The promoters of abusive tax schemes often employ financial instruments such as trusts in their schemes. However, the instruments are used for improper purposes including the facilitation of tax evasion. Schemes Fraud Disclosure 337 PMD on Process A E NG 4/4/2020 Tax evasion using foreign jurisdictions is accomplished using many different methods. Some can be as simple as taking Espaol unreported cash receipts and personally traveling to a tax haven country and depositing the cash into a bank account. Others are more elaborate involving numerous domestic and foreign trusts, partnerships, nominees, etc. The following schemes are not all-inclusive, but just a sample of abusive tax schemes. Abusive Foreign Trust Schemes: The foreign trust schemes usually start off as a series of domestic trusts layered upon one another. This set up is used to give the appearance that the taxpayer has turned his/her business and assets over to a trust and is no longer in control of the business or its assets. Once transferred to the domestic trust the income and expenses are passed to one or more foreign trusts, typically in tax haven countries. As an example, a taxpayer's business is split into two trusts. One trust would be the business trust that is in charge of the daily operations. The other trust is an equipment trust formed to hold the business's equipment that is leased back to the business trust at inflated rates to nullify any income reported on the business trust tax return (Form 1041). Next the income from the equipment trust is distributed to foreign trust-one, again, which nullifies any tax due on the equipment trust tax return. Foreign trust one then distributes all or most of its income to foreign trust two. Since all of foreign trust two's income is foreign based there is no filing requirement. Once the assets are in foreign trust-two, a bank account opened either under the trust name or an International Business Corporation (IBC). The trust documentation and business records of this scheme all make it appear that the taxpayer is no longer in control of his/her business or its assets. The reality is that nothing ever changed. The taxpayer still exercises full control over his/her business and assets. There can be many different variations to the scheme. International Business Corporations (IBC): The taxpayer establishes an IBC with the exact name as that of his/her business. The IBC also has a bank account in the foreign country. As the taxpayer receives checks from customers, he sends them to the bank in the foreign country. The foreign bank then uses its correspondent account in the to process the checks so that it never would appear to the customer, upon reviewing the canceled check that the payment was sent offshore. Once the checks clear the taxpayer's IBC account is credited for the check payments. Here the taxpayer has, again, transferred the unreported income offshore to a tax haven jurisdiction. False Billing Schemes: A taxpayer sets up an International Business Corporation (IBC) in a tax haven country with a nominee as the owner (usually the promoter). A bank account is then opened under the be. On the bank's records the taxpayer would 8:38 PM A ENG /4/2000 Onshore to a tax haven jurisdiction. False Billing Schemes: A taxpayer sets up an International Business Corporation (IBC) in a tax haven country with a nominee as the owner (usually the promoter). A bank account is then opened under the IBC. On the bank's records the taxpayer would be listed as a signatory on the account. The promoter then issues invoices to the taxpayer's business for goods allegedly purchased by the taxpayer. The taxpayer then sends payment to the IBC that gets deposited into the joint account held by the IBC and taxpayer. The taxpayer takes a business deduction for the payment to the IBC thereby reducing his/her taxable income and has safely placed the unreported income into the foreign bank account. Table of Contents - Abusive Tax Schemes Criminal Investigation (1) far-2020 Share Print foin 3 Related Sites Other Languages Know Your Rights Resolve an Issue U.S. Treasury Espaol NoticeStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Swanson On Internal Auditing Raising The Bar

Authors: IT Governance Publishing

1st Edition

1849280673, 978-1849280679