Answered step by step

Verified Expert Solution

Question

1 Approved Answer

PLEASE DO ALL OF THEM. DONT COPY FROM TUTORS!!! THEY DID IT WRONG!! PLEASE IF YOU CAN DO ALL OF THEM DONT BOTHER DOING IT,

PLEASE DO ALL OF THEM. DONT COPY FROM TUTORS!!! THEY DID IT WRONG!! PLEASE IF YOU CAN DO ALL OF THEM DONT BOTHER DOING IT, every perosn i ask they do JUST A!! PLEASE DO ALL AND I WILL GUVE YOU A THUMBS UP. IF YOU COPY AND JUST do A. i will guve A THUMBS DOWN, BUT IF YOU DO ALL I WILL GIVE THUMBS UP!!

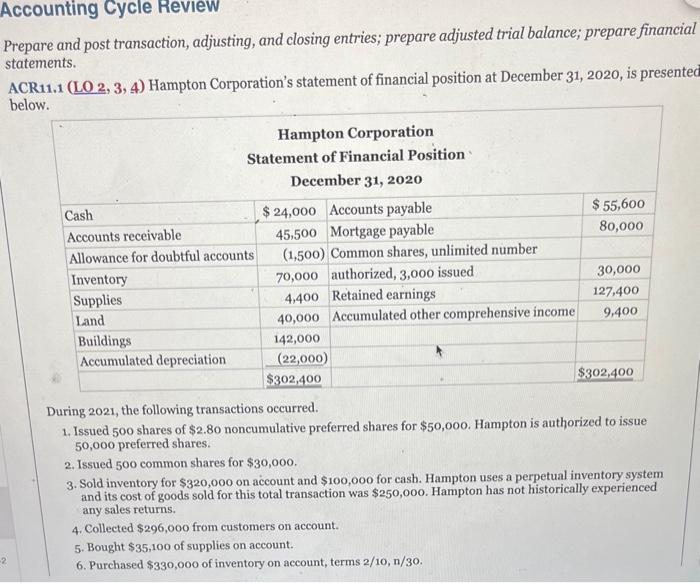

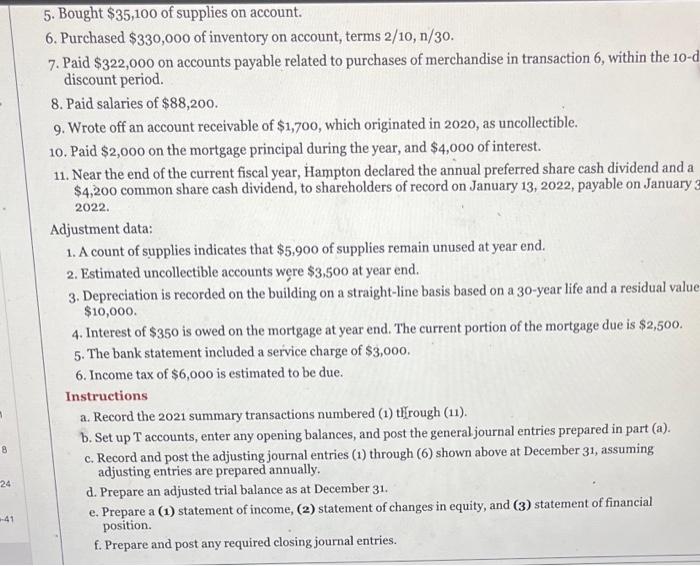

Prepare and post transaction, adjusting, and closing entries; prepare adjusted trial balance; prepare financial statements. ACR11.1 ( LO2,3,4 ) Hampton Corporation's statement of financial position at December 31, 2020, is presentec below. During 2021, the following transactions occurred. 1. Issued 500 shares of $2.80 noncumulative preferred shares for $50,000. Hampton is authorized to issue 50,000 preferred shares. 2. Issued 500 common shares for $30,000. 3. Sold inventory for $320,000 on account and $100,000 for cash. Hampton uses a perpetual inventory system and its cost of goods sold for this total transaction was $250,000. Hampton has not historically experienced any sales returns. 4. Collected $296,000 from customers on account. 5. Bought $35,100 of supplies on account. 6. Purchased $330,000 of inventory on account, terms 2/10,n/30. 5. Bought $35,100 of supplies on account. 6. Purchased $330,000 of inventory on account, terms 2/10, n/30. 7. Paid $322,000 on accounts payable related to purchases of merchandise in transaction 6 , within the 10-1 discount period. 8. Paid salaries of $88,200. 9. Wrote off an account receivable of $1,700, which originated in 2020 , as uncollectible. 10. Paid $2,000 on the mortgage principal during the year, and $4,000 of interest. 11. Near the end of the current fiscal year, Hampton declared the annual preferred share cash dividend and a $4,200 common share cash dividend, to shareholders of record on January 13,2022 , payable on January: 2022. Adjustment data: 1. A count of supplies indicates that $5,900 of supplies remain unused at year end. 2. Estimated uncollectible accounts were $3,500 at year end. 3. Depreciation is recorded on the building on a straight-line basis based on a 30 -year life and a residual valuc $10,000. 4. Interest of $350 is owed on the mortgage at year end. The current portion of the mortgage due is $2,500. 5. The bank statement included a service charge of $3,000. 6 . Income tax of $6,000 is estimated to be due. Instructions a. Record the 2021 summary transactions numbered (1) through (11). b. Set up T accounts, enter any opening balances, and post the general journal entries prepared in part (a). c. Record and post the adjusting journal entries (1) through (6) shown above at December 31 , assuming adjusting entries are prepared annually. d. Prepare an adjusted trial balance as at December 31 . e. Prepare a (1) statement of income, (2) statement of changes in equity, and (3) statement of financial position. f. Prepare and post any required closing journal entries Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding Financial Accounting

Authors: Christopher D. Burnley

3rd Canadian Edition

1119715474, 9781119715474