Answered step by step

Verified Expert Solution

Question

1 Approved Answer

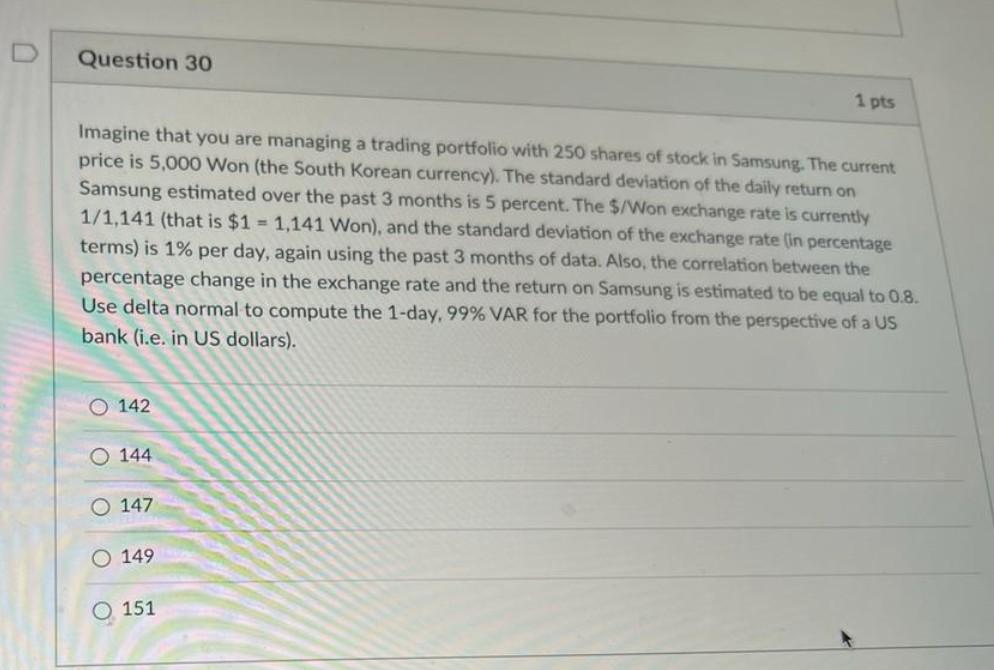

please do it in 20 minutes please urgently... I'll give you up thumb definitely D Question 30 1 pts Imagine that you are managing a

please do it in 20 minutes please urgently... I'll give you up thumb definitely

D Question 30 1 pts Imagine that you are managing a trading portfolio with 250 shares of stock in Samsung. The current price is 5,000 Won (the South Korean currency). The standard deviation of the daily return on Samsung estimated over the past 3 months is 5 percent. The $/Won exchange rate is currently 1/1,141 (that is $1 = 1,141 Won), and the standard deviation of the exchange rate (in percentage terms) is 1% per day, again using the past 3 months of data. Also, the correlation between the percentage change in the exchange rate and the return on Samsung is estimated to be equal to 0.8. Use delta normal to compute the 1-day, 99% VAR for the portfolio from the perspective of a US bank (i.e. in US dollars). O 142 0 144 O 147 O 149 o 151Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Fitness Forever 5 Steps To More Money Less Risk And More Peace Of Mind

Authors: Paul Merriman, Richard Buck

1st Edition

0071786988,0071786996