Question

Please do not respond with answer that are already out there i have check them and they are not completely correct. Hank is a single

Please do not respond with answer that are already out there i have check them and they are not completely correct.

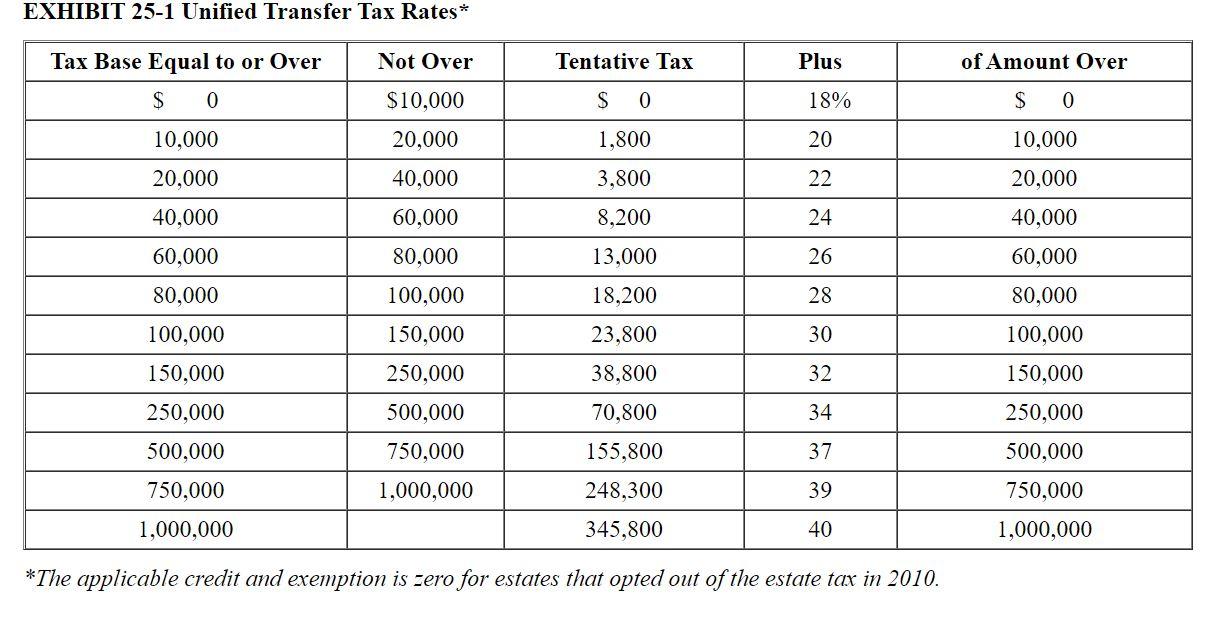

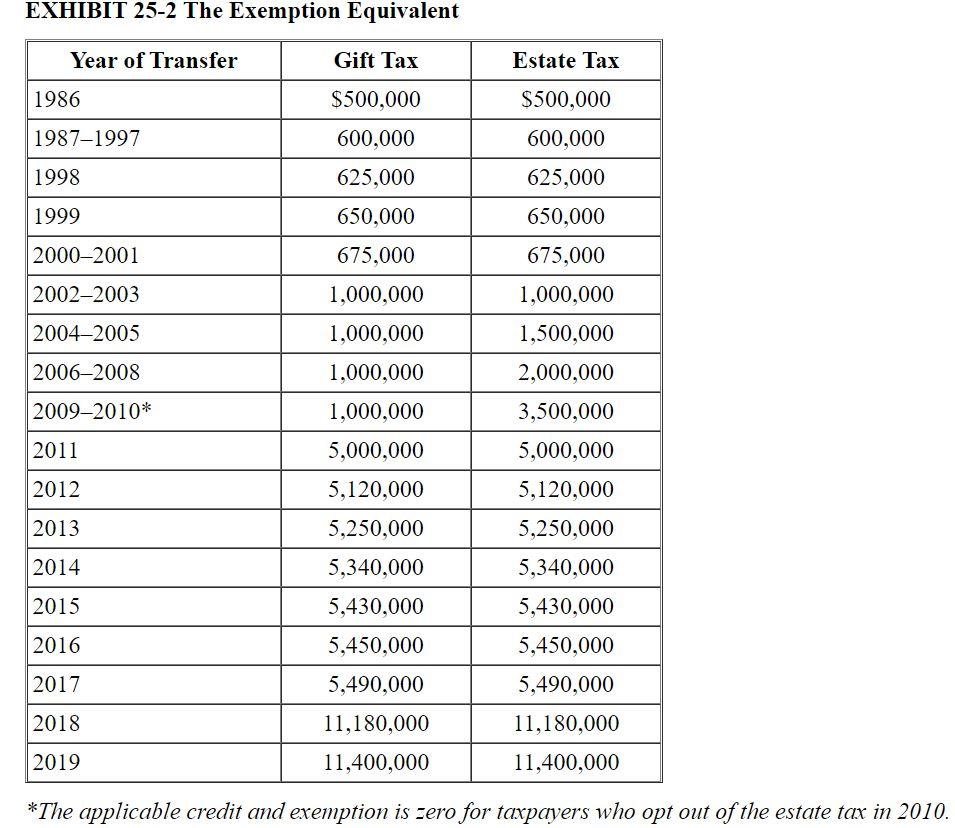

Hank is a single individual who possesses a life insurance policy worth $300,000 that will pay his two children a total of $800,000 upon his death. This year Hank transferred the policy and all incidents of ownership to an irrevocable trust that pays income annually to his two children for 15 years and then distributes the corpus to the children in equal shares.

a. Calculate the amount of gift tax due (if any) on the gift. Assume that Hank has made only one prior taxable gift of $5 million in 2011.

b. Calculate the amount of cumulative taxable transfers for estate tax purposes if Hank dies this year but after the date of the gift. At the time of his death, Hank's probate estate is $10 million and it is to be divided in equal shares between his two children.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managerial Accounting

Authors: John Wild, Ken Shaw

6th Edition

9781259726972