Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please do the following problem in excel, and show the formuals when showing work. Suppose that there are many stocks in the security market and

Please do the following problem in excel, and show the formuals when showing work.

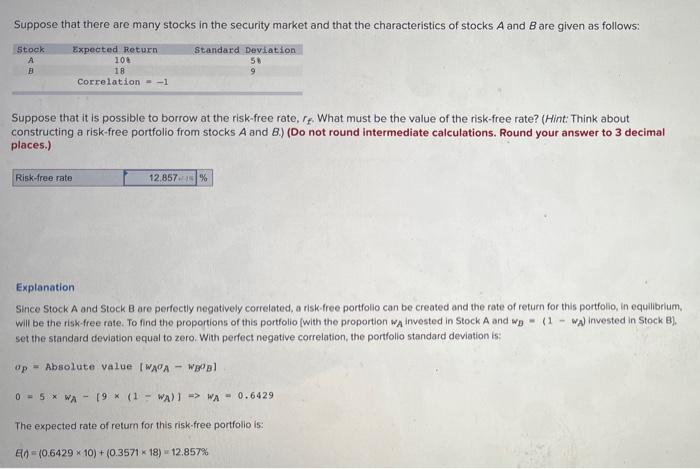

Suppose that there are many stocks in the security market and that the characteristics of stocks A and B are given as follows:

Suppose that it is possible to borrow at the risk-free rate, rf. What must be the value of the risk-free rate? (Hint: Think about constructing a risk-free portfolio from stocks A and B.) (Do not round intermediate calculations. Round your answer to 3 decimal places.)

please show the excel formulas used in excel *

Suppose that there are many stocks in the security market and that the characteristics of stocks A and B are given as follows: Stock B Expected Return 100 18 Correlation-1 Standard Deviation 58 9 Suppose that it is possible to borrow at the risk-free rate, rr. What must be the value of the risk-free rate? (Hint: Think about constructing a risk-free portfolio from stocks A and B.) (Do not round Intermediate calculations. Round your answer to 3 decimal places.) Risk-free rate 12.857% Explanation Since Stock A and Stock Bare perfectly negatively correlated, a risk free portfolio can be created and the rate of return for this portfolio, in equilibrium, will be the risk-free rate. To find the proportions of this portfolio (with the proportion wa invested in Stock A and we - (1 - wa) invested in Stock B), set the standard deviation equal to zero. With perfect negative correlation, the portfolio standard deviation is: Op = Absolute value IWAPA - W] 0 = 5* WA - 19 * (1 - WA) -> WA - 0.6429 The expected rate of return for this risk-free portfolio is: 60 - (0.6429 X 10) + (0.3571 18) 12.857% Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Options Trading QuickStart Guide The Simplified Beginners Guide To Options Trading

Authors: Clydebank Finance

2nd Edition

1945051051, 978-1945051050