Answered step by step

Verified Expert Solution

Question

1 Approved Answer

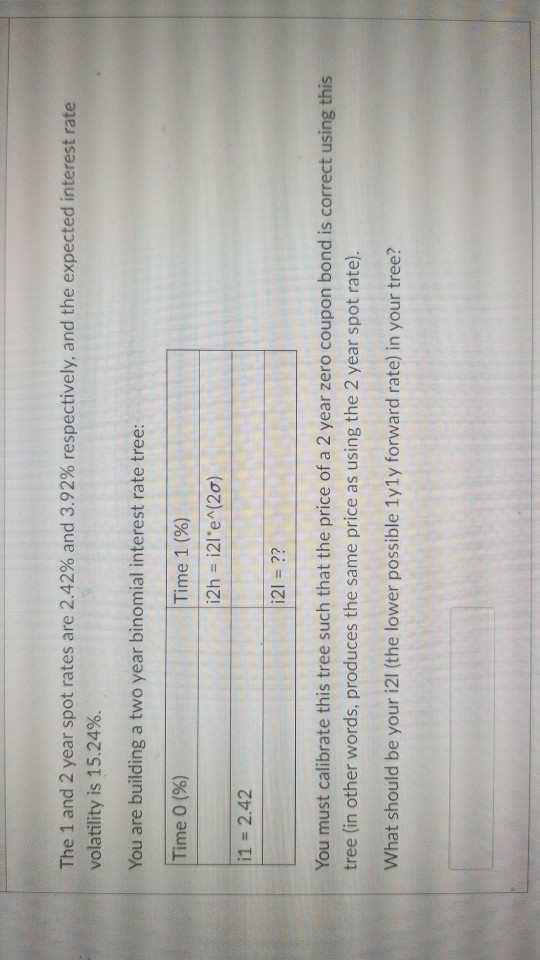

please do the problem on excel. and show your steps. thanks. The 1 and 2 year spot rates are 2.42% and 3.92% respectively, and the

please do the problem on excel. and show your steps. thanks.

The 1 and 2 year spot rates are 2.42% and 3.92% respectively, and the expected interest rate volatility is 15.24%. You are building a two year binomial interest rate tree: Time 0 (%) Time 1 (%) i2h = i21'e (20) i1 = 2.42 i21 = ?? You must calibrate this tree such that the price of a 2 year zero coupon bond is correct using this tree (in other words, produces the same price as using the 2 year spot rate). What should be your i21 (the lower possible lyly forward rate) in your treeStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Essentials Of Health Care Finance

Authors: William O. Cleverley

3rd Edition

0834203413, 978-0834203419