Answered step by step

Verified Expert Solution

Question

1 Approved Answer

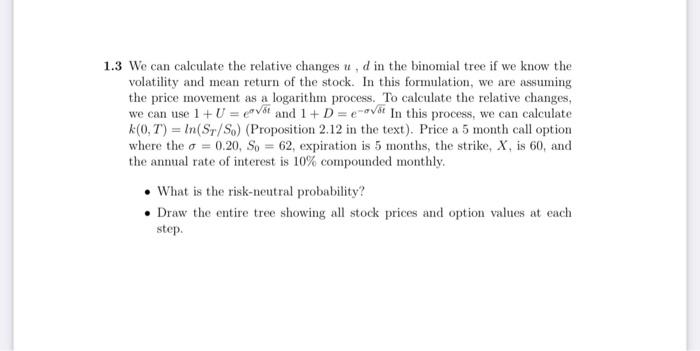

please do this question on the paper. thanks 3 We can calculate the relative changes u,d in the binomial tree if we know the volatility

please do this question on the paper. thanks

3 We can calculate the relative changes u,d in the binomial tree if we know the volatility and mean return of the stock. In this formulation, we are assuming the price movement as a logarithm process. To calculate the relative changes, we can use 1+U=e6t and 1+D=e6t In this process, we can calculate k(0,T)=ln(ST/S0) (Proposition 2.12 in the text). Price a 5 month call option where the =0.20,S0=62, expiration is 5 months, the strike, X, is 60 , and the annual rate of interest is 10% compounded monthly. - What is the risk-neutral probability? - Draw the entire tree showing all stock prices and option values at each step Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Behavioral Finance

Authors: Edwin Burton, Sunit N. Shah

1st Edition

111830019X, 978-1118300190