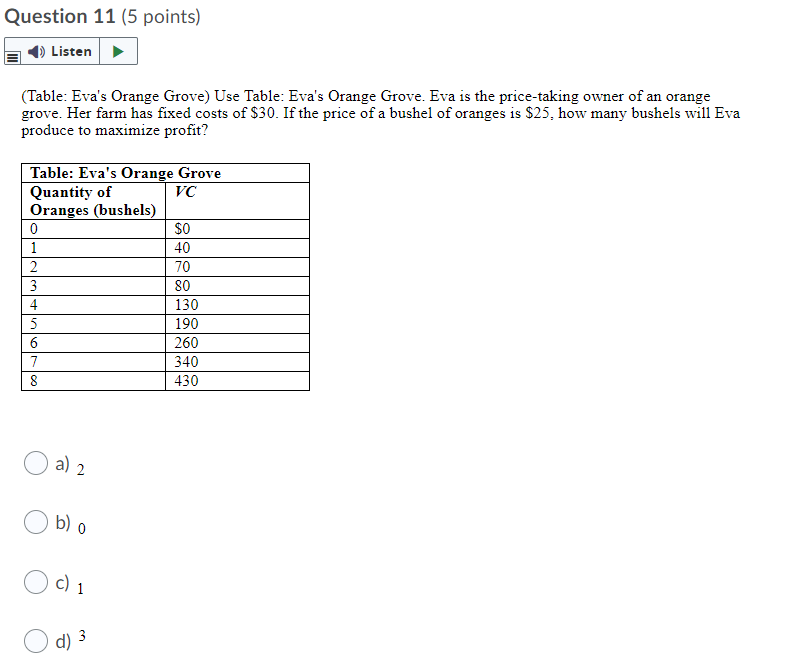

Please explain and answer the questions below Question 11 (5 points) Listen (Table: Eva's Orange Grove) Use Table: Eva's Orange Grove. Eva is the price-taking

Please explain and answer the questions below

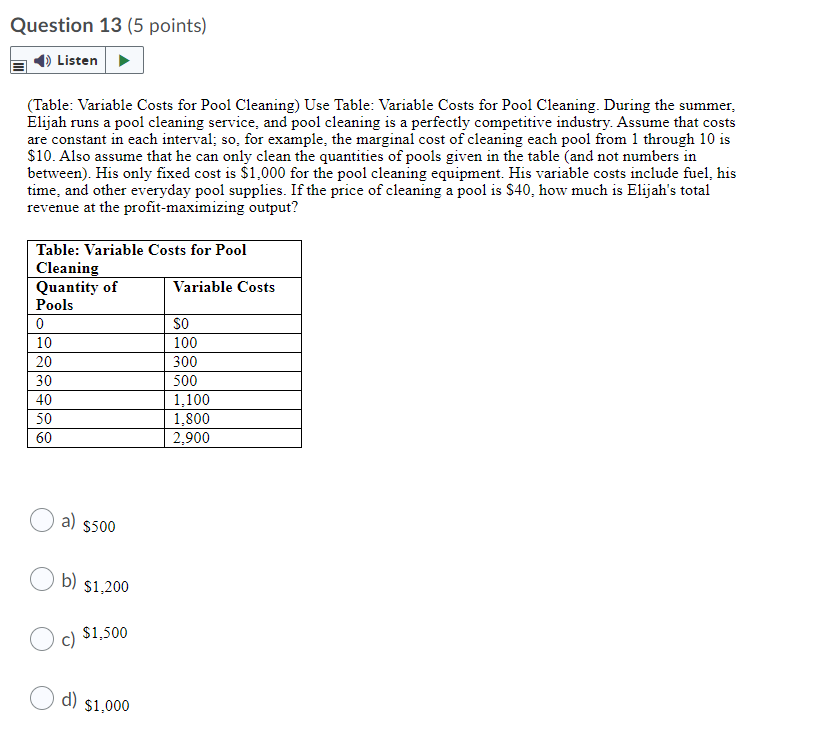

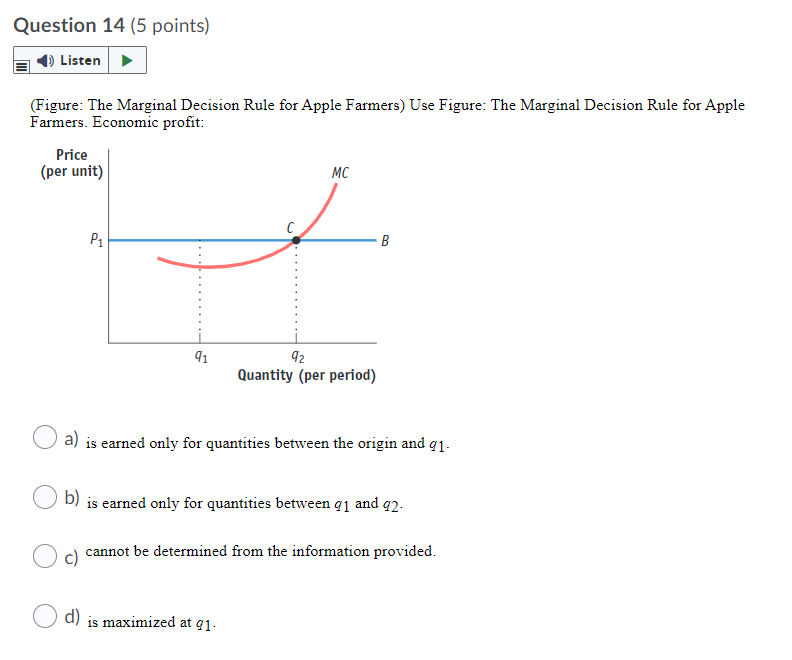

Question 11 (5 points) Listen (Table: Eva's Orange Grove) Use Table: Eva's Orange Grove. Eva is the price-taking owner of an orange grove. Her farm has fixed costs of $30. If the price of a bushel of oranges is $25, how many bushels will Eva produce to maximize profit? Table: Eva's Orange Grove Quantity of VC Oranges (bushels) 0 1 40 2 70 3 80 4 130 5 190 6 260 340 8 430 a) 2 O b) o Oc) 1 O d) 3Question 12 (5 points) Listen In perfect competition, the assumption of easy entry and exit implies that, in the run, all firms in the industry will earn economic profits. a) long: positive (b) short; zero ( c) short; positive ( d) long; zeroQuestion 13 (5 points} all (Table: Variable Costs for Pool Cleaning] Use Table: Variable Costs for Pool Cleaning. During the summer, Elijah runs a pool cleaning service, and pool cleaning is a perfectly competitive industry. Assume that costs are constant in each interval; so, for example, the marginal cost of cleaning each pool from 1 through 10 is $10. Also assume that he can only clean the quantities of pools given in the table {and not numbers in between). His only xed cost is $1,000 for the pool cleaning equipment. His variable costs include fuel, his time, and other everyday pool supplies. If the price of cleaning a pool is $40, hon.r much is Elijah's total revenue at the protmaximizing output? Table: Variable Costs for Pool Cleaning Quantity of Variable Costs Pools __ __ Question 14 {5 points) all (Figure: The Marginal Decision Rule for Apple Farmers} Use Figure: The Marginal Decision Rule for Apple Farmers. Economic prot: Price {per unit} m: q 1 '12 l|.'Iualntit'_b,r {per period} 0 a} is earned only.r for quantities between the origin and gr]. 0 bl is earned only.r for quantities between in and 432. O C} cannot be determined from the information provided. 0 d} is maximized at q]. Question 15 (5 points} all If the longrun market supplyr curve for a perfectly competitive market is horizontal: then this industry exhibits costs. 0 a] constant 0 b] increasing O C} an absence of marginal O c\" decreasing Question 16 (5 points) () Listen Alexi's perfectly competitive RFID (radio-frequency identification) chip-producing factory is making positive economic profits. If the price of RFID chips is $9, Alexi's output is 3,000 chips per month, and his monthly average total cost is $7, what are his monthly profits? ( a) $2 ( b) $6,000 O c) $21,000 O d) $27,000Question 1? (5 points} an A perfectly competitive industry with constant costs initially.r operates in long-run equilibrium. When demand decreases: O 3] prices and prots will be lower than before the demand decrease in both the long run and the short 11.111. 0 b] prices and prots will be higher than before the demand decrease in both the long run and the short 11.111. 0 C) inthe short rim, prices and prots will be higher, but in the long run, price will fall back to its original level, and rms will again earn zero economic prot. 0 Ell in the short run, prices and prots will fall, but in the long run, price will rise hack to its initial level, as will prots. Question 18 (5 points) all Jennifer's Sunglass Hut operates in a perfectly competitive industry and has standard cost curves. The variable costs at Jennifer's Sunglass Hut decrease, so all the cost curves (except xed cost} shi downward. The demand for Jennifer's sunglasses does not change: nor does the rm shirt dorm. To maximize prots aer the variable cost decrease, Jennifer's Sunglass Hut will its price and its level of production. 0 a] raise; increase 0 b] not change; increase 0 C) raise; decrease 0 Cl} not change; decrease Question 19 (5 points} all Suppose Savannah's art studio is charging the market price= which is slightly higher than her average total cost. This means that Savarmah: O a] is incurring a small economic loss. 0 13} should shut down immediately. 0 Cl is earning a small economic prot. 0 d} is breaking even. Question 20 (5 points} all The supply.r curve: obtained through horizontal summation of the individual rm shortrun suppljx.r curves for all rms in a perfectly competitive industry, is called the curve. 0 a] interim market supplyr O b] short11m market supply 0 C} competitive O c\" marginal cost

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance