Answered step by step

Verified Expert Solution

Question

1 Approved Answer

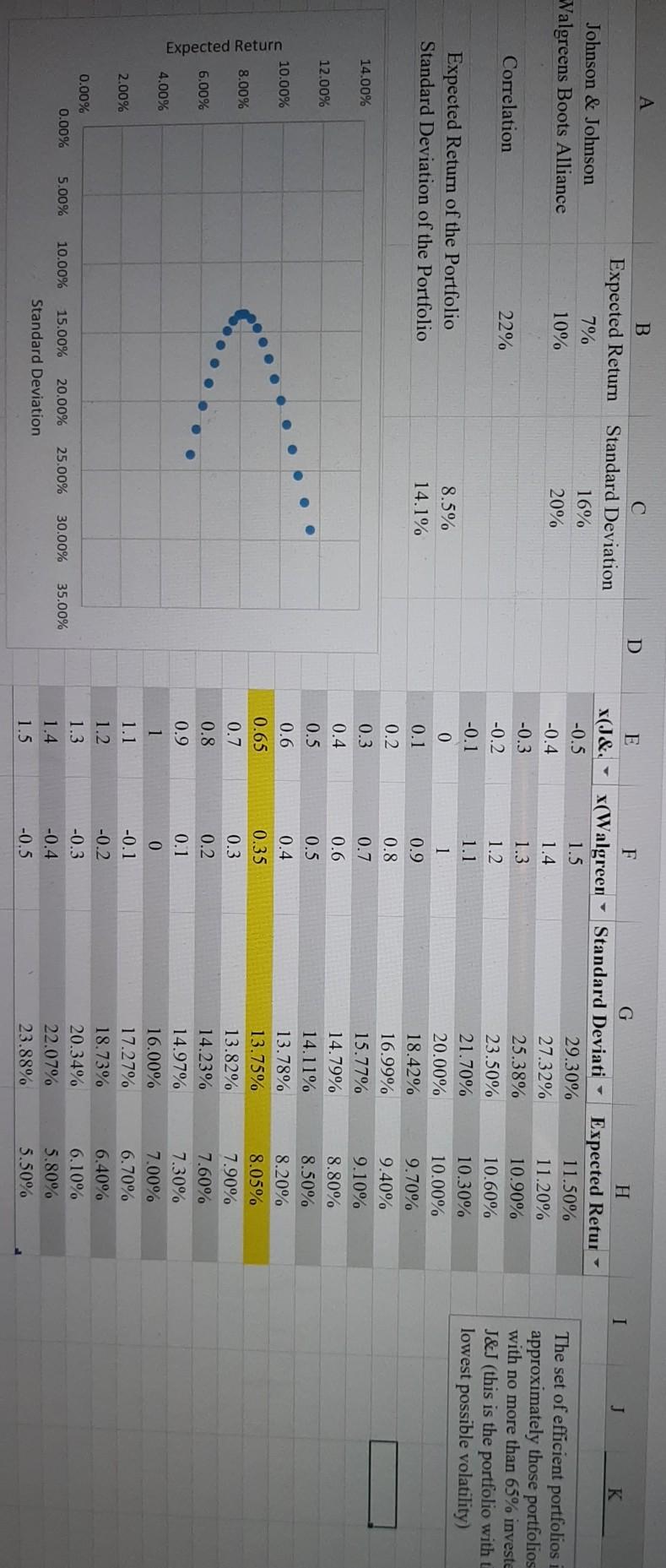

Please explain and comment on the plot This is from question 26 A D I F X(Walgreen J K B Expected Return 7% 10% Johnson

Please explain and comment on the plot

This is from question 26

A D I F X(Walgreen J K B Expected Return 7% 10% Johnson & Johnson Walgreens Boots Alliance Standard Deviation 16% 20% E X(J&, - -0.5 -0.4 -0.3 -0.2 -0.1 1.5 1.4 1.3 Correlation 22% The set of efficient portfolios approximately those portfolios with no more than 65% investe J&J (this is the portfolio with lowest possible volatility) Expected Return of the Portfolio Standard Deviation of the Portfolio 0 8.5% 14.1% 1.2 1.1 1 0.9 0.8 14.00% 0.7 12.00% G Standard Deviati 29.30% 27.32% 25.38% 23.50% 21.70% 20.00% 18.42% 16.99% 15.77% 14.79% 14.11% 13.78% 13.75% 13.82% 14.23% 14.97% 16.00% 17.27% 18.73% 20.34% 22.07% 23.88% 10.00% H Expected Retur 11.50% 11.20% 10.90% 10.60% 10.30% 10.00% 9.70% 9.40% 9.10% 8.80% 8.50% 8.20% 8.05% 7.90% 7.60% 7.30% 7.00% 6.70% 6.40% 6.10% 5.80% 5.50% 0.1 0.2 0.3 0.4 0.5 0.6 0.65 0.7 0.8 0.9 1 1.1 1.2 1.3 1.4 1.5 8.00% Expected Return 0.6 0.5 0.4 0.35 0.3 0.2 0.1 0 -0.1 -0.2 -0.3 -0.4 -0.5 6,00% 4.00% 2.00% 0.00% 0.00% 5.00% 10.00% 15.00% 20.00% 25.00% 30.00% 35.00% Standard Deviation For Problems 23-26, suppose Johnson Johnson and Walgreens Boots Alliance bare expected returns and vola- tilities shou belom, with a correlation of 22%. Expected Return Standard Deviation Johnson & Johnson 7% 16% Walgreens Boots Alliance 10% 20% 23. Calculate (a) the expected return and (b) the volatility (standard deviation) of a portfolio that is equally invested in Johnson & Johnson's and Walgreens' stock. 24. For the portfolio in Problem 23, if the correlation between Johnson & Johnson's and Walgreens stock were to increase, a. Would the expected return of the portfolio rise or fall? b. Would the volatility of the portfolio rise or fall? 25. Calculate (a) the expected return and (b) the volatility (standard deviation of a portfolio that consists of a long position of $10,000 in Johnson & Johnson and a short position of S2000 in Walgreens 26. Using the same data as for Problem 23, calculate the expected return and the volatility (standard deviation) of a portfolio consisting of Johnson & Johnson's and Walgreens' stocks using a wide range of portfolio weights. Plot the expected return as a function of the portfolio volatility Using your graph, identify the range of Johnson & Johnson's portfolio weights that yield ef ficient combinations of the two stocks, rounded to the nearest percentage point. MyLab 27 3Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting The Impact On Decision Makers

Authors: Gary A. Porter, Curtis L. Norton

2nd Edition

0030270995, 978-0030270994