Please fill in the blue blanks :)

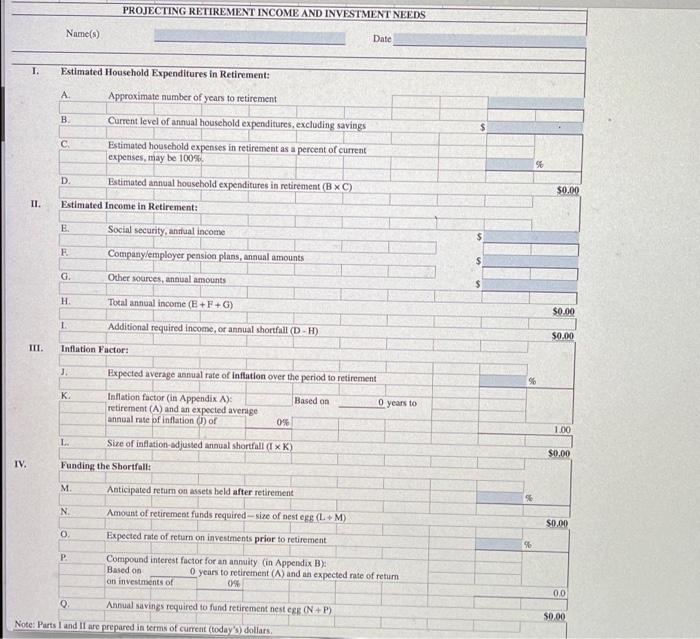

3. LG2 Retirement planning. Use Worksheet 14:1 to assist Lindsay McCoy with her retirement planning needs. She plans to retire in 15 years, and her current household expenditures run about $50,000 per year. Lindsay estimates that she'll spend 80 percent of that amount in retirement. Her Social Security benefit is estimated at $20,000 per year, and she'll receive $12,000 per year from her employer's pension plan (both in today's dollars). Additional assumptions include an inflation rate of 4 percent and a rate of return on retirement assets of 8 percent a year before retirement and 5 percent afterward. Use Worksheet 14.1 to calculate the required size of Lindsay's retirement nest egg and the amount that she must save annually over the next 15 years to reach that goal. > PROJECTING RETIREMENT INCOME AND INVESTMENT NEEDS Name(s) Date I. Estimated Household Expenditures in Retirement: A Approximate number of years to retirement . Current level of annual household expenditures, excluding savings C Estimated household expenses in retirement as a percent of current expenses, may be 100% % D Estimated annual household expenditures in retirement (BXC) $0.00 II. Estimated Income in Retirement: E Social security, annual income E Company employer pension plans, annual amounts $ G Other sources, annual amounts $ H Total annual income (E+F+G) $0.00 1 Additional required income, or annual shortfall (D-H) $0.00 III. Inflation Factor: Expected average annual rate of inflation over the period to retirement 96 K Based on Inflation factor in Appendix A): retirement (A) and an expected average annual rate of inflation () of O years to 0% 1.00 L. Size of inflation-adjusted annual shortfall (x K) $0.00 IV. Funding the Shortfall: M Anticipated return on assets held after retirement (% N Amount of retirement funds required-size of Desteg (L+M $0.00 0 Expected rate of return on investments prior to retirement 96 P Compound interest factor for an annuity (in Appendix B): Based on O years to retirement (A) and an expected rate of retum on investments of 0% 00 0. Annual savings required to fund retirement nestee ( NP) 0.00 Note: Parts and I are prepared in terms of current (today's) dollars 2. LG2 Calculating annual investment to meet retirement target. Use Worksheet 14.1 to help Paul and Crystal Meyer, who'd like to retire in about 20 years. Both have promising careers, and both make good money. As a result, they're willing to put aside whatever is necessary to achieve a comfortable lifestyle in retirement. Their current level of household expenditures (excluding savings) is around $75,000 a year, and they expect to spend even more in retirement; they think they'll need about 125 percent of that amount. (Note: 125 percent equals a multiplier factor of 1.25.) They estimate that their Social Security benefits will amount to $30,000 a year in today's dollars and that they'll receive another $35,000 annually from their company pension plans. They feel that future inflation will amount to about 3 percent a year, and they think they'll be able to earn about 6 percent on their investments before retirement and about 4 percent afterward. Use Worksheet 14.1 to find out how big Paul and Crystal's investment nest egg will have to be and how > and about 4 percent afterward. Use Worksheet 14.1 to find out how big Paul and Crystal's investment nest egg will have to be and how much they'll have to save annually to accumulate the needed amount within the next 20 years