Answered step by step

Verified Expert Solution

Question

1 Approved Answer

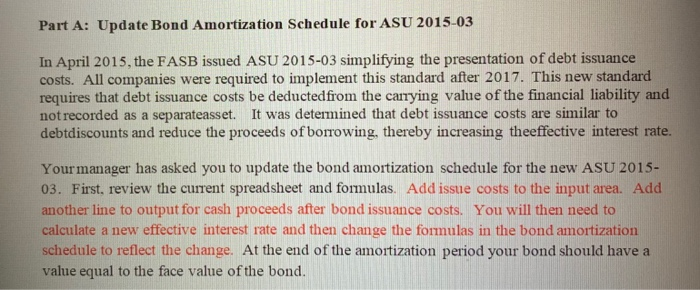

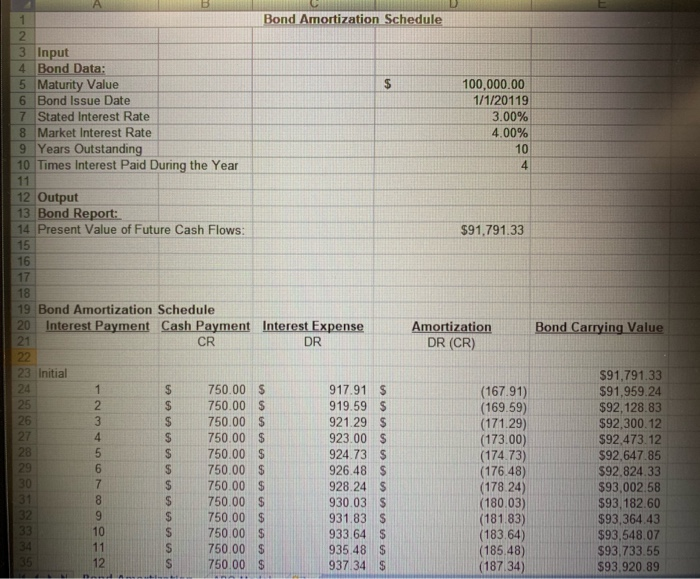

please follow the instructions to help me with the assignment Part A: Update Bond Amortization Schedule for ASU 2015-03 In April 2015, the FASB issued

please follow the instructions to help me with the assignment

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Multicriteria Decision Making Systems Modeling Risk Assessment And Financial Analysis For Technical Projects

Authors: Timothy Havranek, Doug MacNair, James Wolf

3110765640, 978-3110765649