please format the answer in two different exhibits like shown in the two examples provided. thank you!

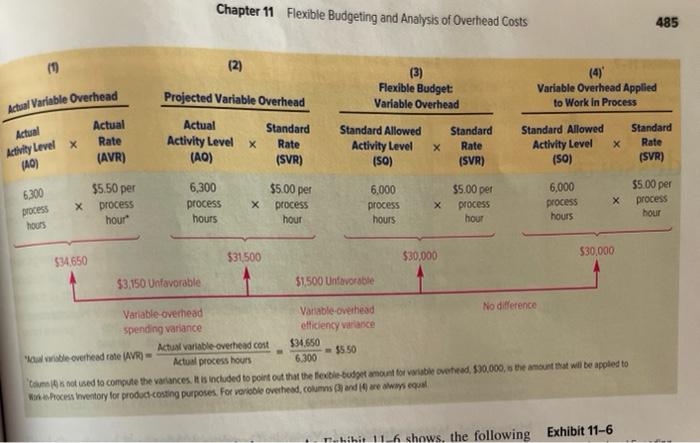

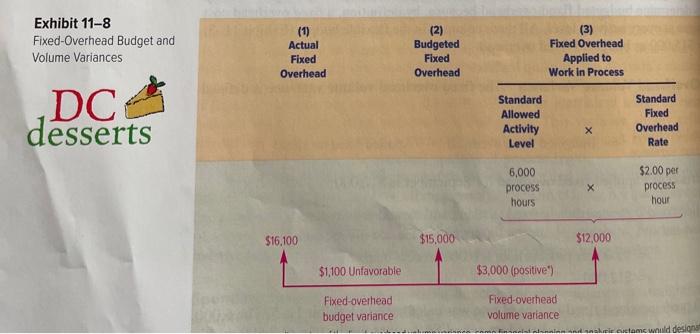

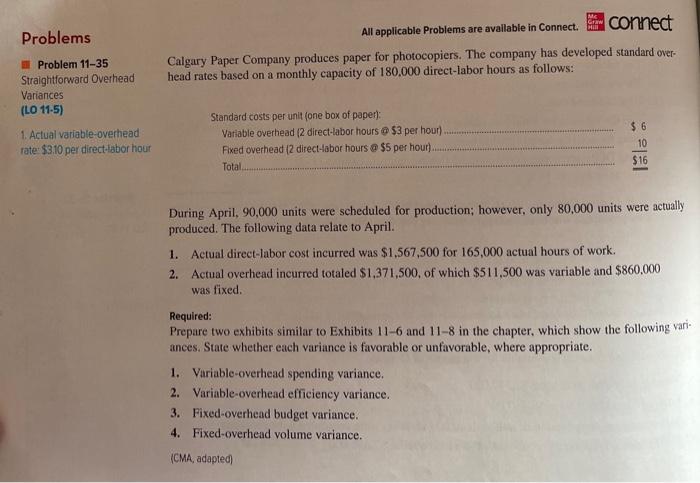

ME Gran Problems All applicable Problems are available in Connect. connect Calgary Paper Company produces paper for photocopiers. The company has developed standard over- head rates based on a monthly capacity of 180.000 direct-labor hours as follows: Problem 11-35 Straightforward Overhead Variances (LO 11-5) 1. Actual variable-overhead rate: $3.10 per direct-labor hour Standard costs per unit (one box of paper): Variable overhead (2 direct-labor hours $3 per hour) Fixed overhead (2 direct-abor hours @ $5 per hour) Total $ 6 10 $16 During April. 90,000 units were scheduled for production; however, only 80,000 units were actually produced. The following data relate to April. 1. Actual direct-labor cost incurred was $1.567,500 for 165,000 actual hours of work. 2. Actual overhead incurred totaled $1,371,500, of which $511,500 was variable and $860,000 was fixed. Required: Prepare two exhibits similar to Exhibits 11-6 and 11-8 in the chapter, which show the following vari- ances. State whether each variance is favorable or unfavorable, where appropriate. 1. Variable-overhead spending variance. 2. Variable-overhead efficiency variance. 3. Fixed-overhead budget variance. 4. Fixed-overhead volume variance. (CMA, adapted Chapter 11 Flexible Budgeting and Analysis of Overhead Costs 485 (2) (3) Flexible Budget Variable Overhead (4) Variable Overhead Applied to Work In Process Projected Variable Overhead Actual Variable Overhead Actual Rate (AVR) Actual Activity Level X (AO) Actual Activity Level x (40) Standard Rate (SVR) Standard Allowed Activity Level (SO) Standard Rate (SVR) Standard Allowed Activity Level (50) Standard Rate (SVR) $5.50 per $5.00 per 6.300 process hours X 6,300 process hours process hour $5.00 per process hour 6,000 process hours X $5.00 per process hour 6,000 process hours process hour $34650 $30,000 $31500 $30,000 $3,150 Unfavorable $1,500 Unfavorable $550 Variable overhead Variable-overhead No difference spending variance efficiency variance Actual variable overhead cost $34650 wie overhead rate (AVR) Actual process hours 6.300 Caminot used to compute the variances. It is included to point out that the fete budget amount for bile ove read, 530,000, the amount that will be applied to Woo Process Inventory for prodoc.costing purposes. For variable overhead, columns 3 andare was equal Tahihit 11 6 shows, the following Exhibit 11-6 Exhibit 11-8 Fixed-Overhead Budget and Volume Variances (1) Actual Fixed Overhead (2) Budgeted Fixed Overhead (3) Fixed Overhead Applied to Work In Process DC desserts Standard Allowed Activity Level Standard Fixed Overhead Rate 6,000 process hours $2.00 per process hour $16,100 $15,000 $12,000 $1,100 Unfavorable $3,000 (positive") Fixed-overhead budget variance Fixed-overhead volume variance Fm Witame would designs