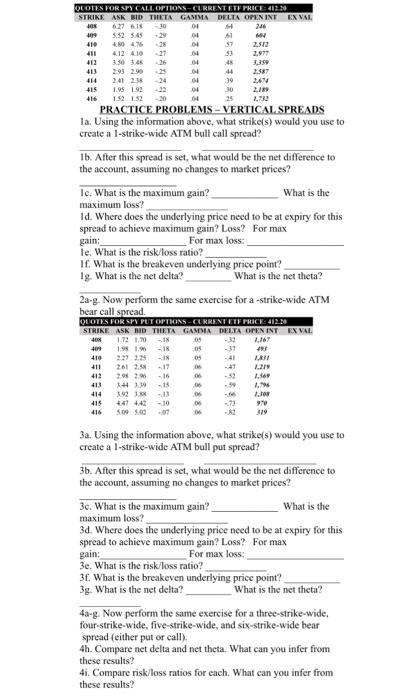

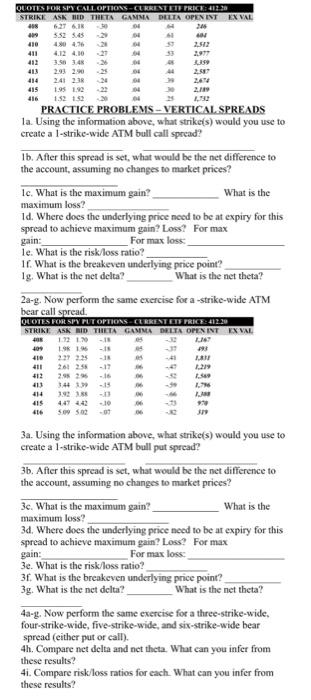

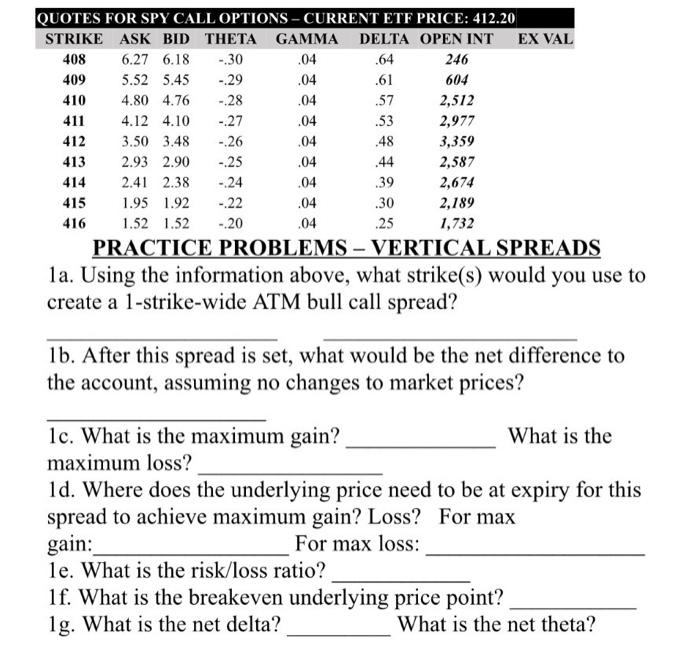

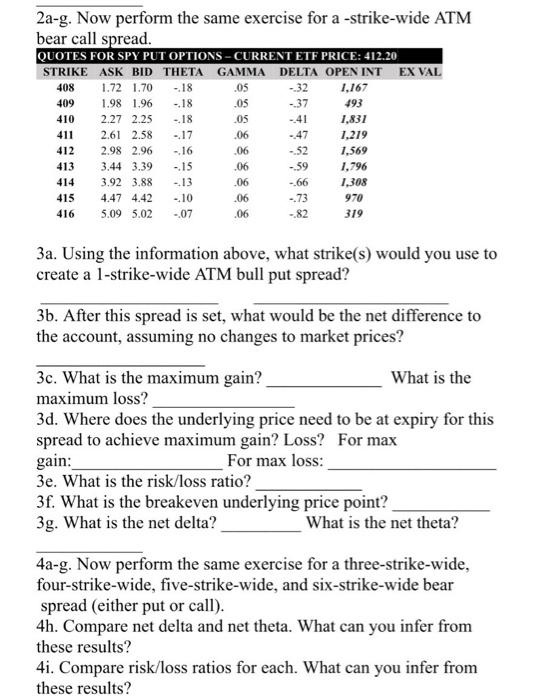

1a. Using the information above, what strike(s) would you use to create a I-strike-wide ATM bull call spread? 1b. After this spread is set, what would be the net difference to the account, assuming no changes to market prices? Ic. What is the maximum gain? What is the maximum loss? Id. Where does the underlying price need to be at expiry for this spread to achieve maximum gain? Loss? For max gain: For max loss: le. What is the risk/loss ratio? If. What is the breakeven underlying price point? lg. What is the net delta? What is the net theta? 2a-g. Now perform the same exercise for a -strike-wide ATM hear call snread 3a. Using the information above, what strike(s) would you use to create a I-strike-wide ATM bull put spread? 3b. After this spread is set, what would be the net difference to the account, assuming no changes to market prices? 3c. What is the maximum gain? What is the maximum loss? 3d. Where does the underlying price need to be at expiry for this spread to achicve maximum gain? Loss? For max gain For max loss: 3e. What is the riskloss ratio? 3f. What is the breakeven underlying price point? 3g. What is the net delta? What is the net theta? 4a-g. Now perform the same exercise for a three-strike-wide. four-strike-wide, five-strike-wide, and six-strike-wide bear spread (either put or call). 4h. Compare net delta and net theta. What can you infer from these results? 4i. Compare risk/loss ratios for each. What can you infer from these results? la. Using the information above, what strike(s) would you use to create a 1-strike-wide ATM bull call spread? 1b. After this spread is set, what would be the net difference to the account, assuming no changes to market prices? 1c. What is the maximum gain? What is the maximum loss? 1d. Where does the underlying price need to be at expiry for this spread to achieve maximum gain? Loss? For max gain: For max loss le. What is the risk/loss ratio? 1f. What is the breakeven underlying price point? 1g. What is the net delta? What is the net theta? 2a-g. Now perform the same exercise for a-strike-wide ATM hear call snresal 3a. Using the information above, what strike(s) would you use to create a 1-strike-wide ATM bull put spread? 3b. After this spread is set, what would be the net difference to the account, assuming no changes to market prices? 3c. What is the maximum gain? What is the maximum loss? 3d. Where does the underlying price need to be at expiry for this spread to achieve maximum gain? Loss? For max gain: For max loss: 3e. What is the risk/loss ratio? 3f. What is the breakeven underlying price point? 3g. What is the net delta? What is the net theta? 4a-g. Now perform the same exercise for a three-strike-wide, four-strike-wide, frve-strike-wide, and six-strike-wide bear spread (either put or call). 4h. Compare net delta and net theta. What can you infer from these results? 4i. Compare risk/loss ratios for each. What ean you infer from these results? 1b. After this spread is set, what would be the net difference to the account, assuming no changes to market prices? 1c. What is the maximum gain? What is the maximum loss? 1d. Where does the underlying price need to be at expiry for this spread to achieve maximum gain? Loss? For max gain:- For max loss: 1e. What is the risk/loss ratio? 1f. What is the breakeven underlying price point? 1g. What is the net delta? What is the net theta? 2a-g. Now perform the same exercise for a -strike-wide ATM bear call spread. 3a. Using the information above, what strike(s) would you use to create a 1-strike-wide ATM bull put spread? 3b. After this spread is set, what would be the net difference to the account, assuming no changes to market prices? 3c. What is the maximum gain? What is the maximum loss? 3d. Where does the underlying price need to be at expiry for this spread to achieve maximum gain? Loss? For max gain: For max loss: 3e. What is the risk/loss ratio? 3f. What is the breakeven underlying price point? 3g. What is the net delta? What is the net theta? 4ag. Now perform the same exercise for a three-strike-wide, four-strike-wide, five-strike-wide, and six-strike-wide bear spread (either put or call). 4h. Compare net delta and net theta. What can you infer from these results? 4i. Compare risk/loss ratios for each. What can you infer from these results? 1a. Using the information above, what strike(s) would you use to create a I-strike-wide ATM bull call spread? 1b. After this spread is set, what would be the net difference to the account, assuming no changes to market prices? Ic. What is the maximum gain? What is the maximum loss? Id. Where does the underlying price need to be at expiry for this spread to achieve maximum gain? Loss? For max gain: For max loss: le. What is the risk/loss ratio? If. What is the breakeven underlying price point? lg. What is the net delta? What is the net theta? 2a-g. Now perform the same exercise for a -strike-wide ATM hear call snread 3a. Using the information above, what strike(s) would you use to create a I-strike-wide ATM bull put spread? 3b. After this spread is set, what would be the net difference to the account, assuming no changes to market prices? 3c. What is the maximum gain? What is the maximum loss? 3d. Where does the underlying price need to be at expiry for this spread to achicve maximum gain? Loss? For max gain For max loss: 3e. What is the riskloss ratio? 3f. What is the breakeven underlying price point? 3g. What is the net delta? What is the net theta? 4a-g. Now perform the same exercise for a three-strike-wide. four-strike-wide, five-strike-wide, and six-strike-wide bear spread (either put or call). 4h. Compare net delta and net theta. What can you infer from these results? 4i. Compare risk/loss ratios for each. What can you infer from these results? la. Using the information above, what strike(s) would you use to create a 1-strike-wide ATM bull call spread? 1b. After this spread is set, what would be the net difference to the account, assuming no changes to market prices? 1c. What is the maximum gain? What is the maximum loss? 1d. Where does the underlying price need to be at expiry for this spread to achieve maximum gain? Loss? For max gain: For max loss le. What is the risk/loss ratio? 1f. What is the breakeven underlying price point? 1g. What is the net delta? What is the net theta? 2a-g. Now perform the same exercise for a-strike-wide ATM hear call snresal 3a. Using the information above, what strike(s) would you use to create a 1-strike-wide ATM bull put spread? 3b. After this spread is set, what would be the net difference to the account, assuming no changes to market prices? 3c. What is the maximum gain? What is the maximum loss? 3d. Where does the underlying price need to be at expiry for this spread to achieve maximum gain? Loss? For max gain: For max loss: 3e. What is the risk/loss ratio? 3f. What is the breakeven underlying price point? 3g. What is the net delta? What is the net theta? 4a-g. Now perform the same exercise for a three-strike-wide, four-strike-wide, frve-strike-wide, and six-strike-wide bear spread (either put or call). 4h. Compare net delta and net theta. What can you infer from these results? 4i. Compare risk/loss ratios for each. What ean you infer from these results? 1b. After this spread is set, what would be the net difference to the account, assuming no changes to market prices? 1c. What is the maximum gain? What is the maximum loss? 1d. Where does the underlying price need to be at expiry for this spread to achieve maximum gain? Loss? For max gain:- For max loss: 1e. What is the risk/loss ratio? 1f. What is the breakeven underlying price point? 1g. What is the net delta? What is the net theta? 2a-g. Now perform the same exercise for a -strike-wide ATM bear call spread. 3a. Using the information above, what strike(s) would you use to create a 1-strike-wide ATM bull put spread? 3b. After this spread is set, what would be the net difference to the account, assuming no changes to market prices? 3c. What is the maximum gain? What is the maximum loss? 3d. Where does the underlying price need to be at expiry for this spread to achieve maximum gain? Loss? For max gain: For max loss: 3e. What is the risk/loss ratio? 3f. What is the breakeven underlying price point? 3g. What is the net delta? What is the net theta? 4ag. Now perform the same exercise for a three-strike-wide, four-strike-wide, five-strike-wide, and six-strike-wide bear spread (either put or call). 4h. Compare net delta and net theta. What can you infer from these results? 4i. Compare risk/loss ratios for each. What can you infer from these results