Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please help A dog training business began on December 1 . The following transactions occurred during its first month. December 1 Receives $29,000 cash as

Please help

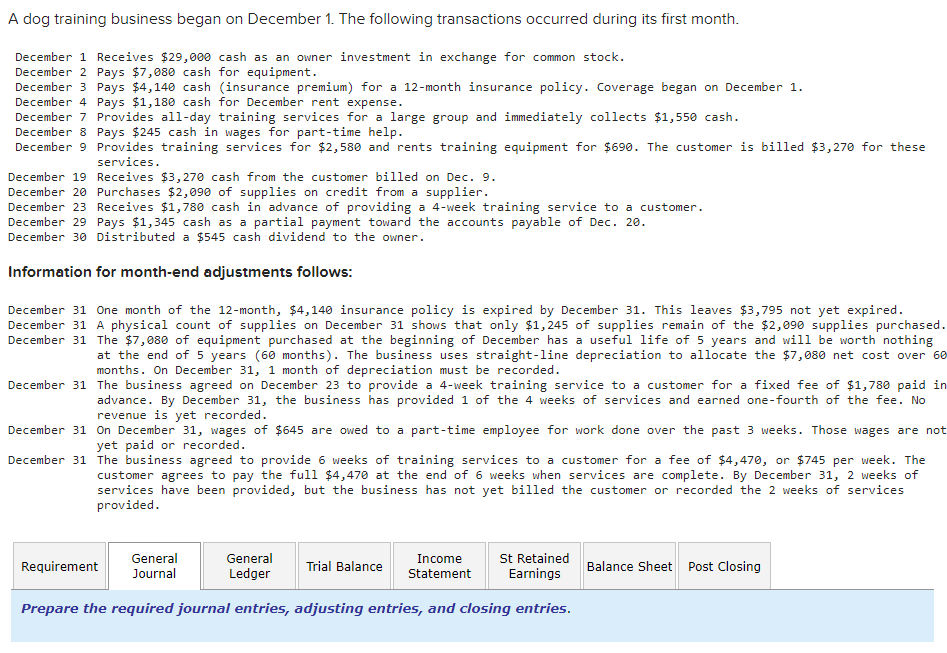

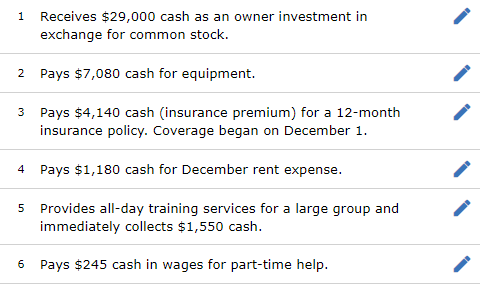

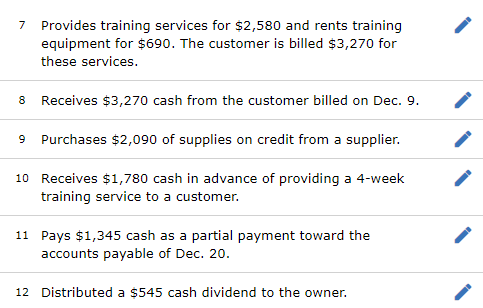

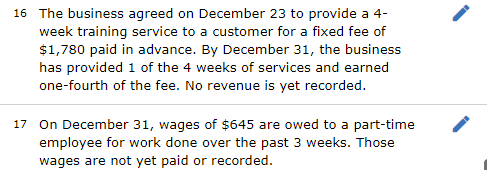

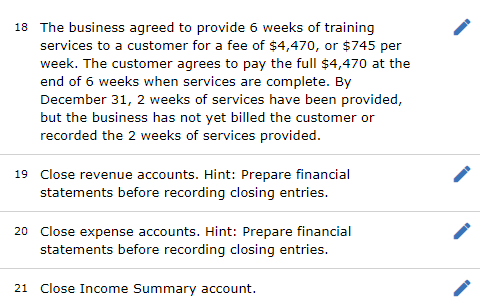

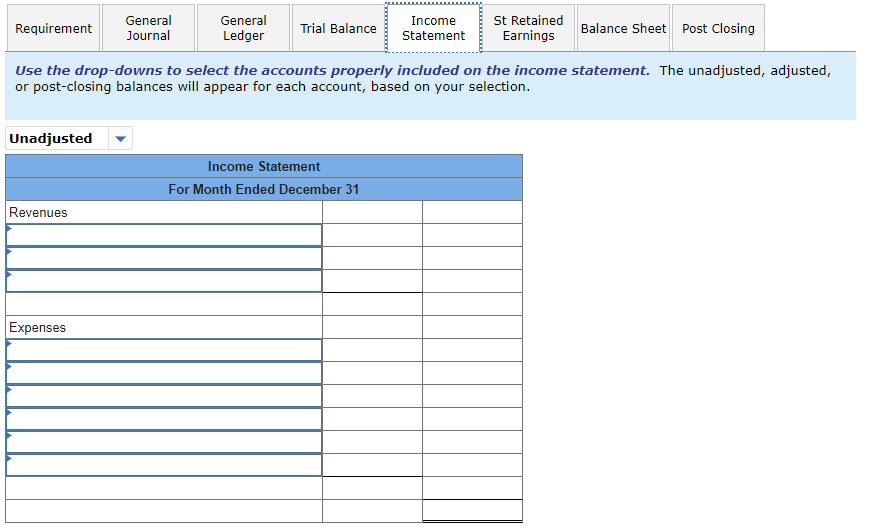

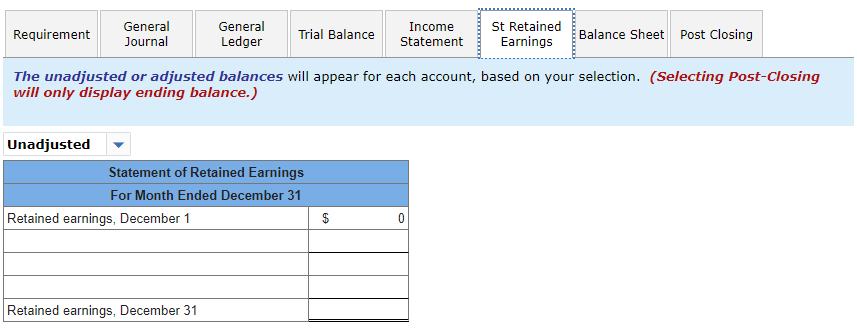

A dog training business began on December 1 . The following transactions occurred during its first month. December 1 Receives $29,000 cash as an owner investment in exchange for common stock. December 2 Pays $7,080 cash for equipment. December 3 Pays $4,140 cash (insurance premium) for a 12-month insurance policy. Coverage began on December 1 . December 4 Pays $1,180 cash for December rent expense. December 7 Provides all-day training services for a large group and immediately collects $1,550 cash. December 8 Pays $245 cash in wages for part-time help. December 9 Provides training services for $2,580 and rents training equipment for $690. The customer is billed $3,270 for these services. December 19 Receives $3,270 cash from the customer billed on Dec. 9. December 20 Purchases $2,090 of supplies on credit from a supplier. December 23 Receives $1,780 cash in advance of providing a 4-week training service to a customer. December 29 Pays $1,345 cash as a partial payment toward the accounts payable of Dec. 20. December 30 Distributed a $545 cash dividend to the owner. Information for month-end adjustments follows: December 31 One month of the 12-month, $4,140 insurance policy is expired by December 31 . This leaves $3,795 not yet expired. December 31 A physical count of supplies on December 31 shows that only $1,245 of supplies remain of the $2, 090 supplies purchased. December 31 The $7,080 of equipment purchased at the beginning of December has a useful life of 5 years and will be worth nothing at the end of 5 years ( 60 months). The business uses straight-line depreciation to allocate the $7,080 net cost over 66 months. On December 31 , 1 month of depreciation must be recorded. December 31 The business agreed on December 23 to provide a 4-week training service to a customer for a fixed fee of $1,780 paid ir advance. By December 31 , the business has provided 1 of the 4 weeks of services and earned one-fourth of the fee. No revenue is yet recorded. December 31 On December 31 , wages of $645 are owed to a part-time employee for work done over the past 3 weeks. Those wages are not yet paid or recorded. December 31 The business agreed to provide 6 weeks of training services to a customer for a fee of $4,470, or $745 per week. The customer agrees to pay the full $4,470 at the end of 6 weeks when services are complete. By December 31 , 2 weeks of services have been provided, but the business has not yet billed the customer or recorded the 2 weeks of services provided. Prepare the required journal entries, adjusting entries, and closing entries. 1 Receives $29,000 cash as an owner investment in exchange for common stock. 2 Pays $7,080 cash for equipment. 3 Pays $4,140 cash (insurance premium) for a 12-month insurance policy. Coverage began on December 1. 4 Pays $1,180 cash for December rent expense. 5 Provides all-day training services for a large group and immediately collects $1,550 cash. 6 Pays $245 cash in wages for part-time help. 7 Provides training services for $2,580 and rents training equipment for $690. The customer is billed $3,270 for these services. 8 Receives $3,270 cash from the customer billed on Dec. 9 . 9 Purchases $2,090 of supplies on credit from a supplier. 10 Receives $1,780 cash in advance of providing a 4-week training service to a customer. 11 Pays $1,345 cash as a partial payment toward the accounts payable of Dec. 20. 12 Distributed a $545 cash dividend to the owner. 13 One month of the 12 -month, $4,140 insurance policy is expired by December 31 . This leaves $3,795 not yet expired. 14 A physical count of supplies on December 31 shows that only $1,245 of supplies remain of the $2,090 supplies purchased. 15 The $7,080 of equipment purchased at the beginning of December has a useful life of 5 years and will be worth nothing at the end of 5 years ( 60 months). The business uses straight-line depreciation to allocate the $7,080 net cost over 60 months. On December 31,1 month of depreciation must be recorded. 16 The business agreed on December 23 to provide a 4week training service to a customer for a fixed fee of $1,780 paid in advance. By December 31 , the business has provided 1 of the 4 weeks of services and earned one-fourth of the fee. No revenue is yet recorded. 17 On December 31 , wages of $645 are owed to a part-time employee for work done over the past 3 weeks. Those wages are not yet paid or recorded. 18 The business agreed to provide 6 weeks of training services to a customer for a fee of $4,470, or $745 per week. The customer agrees to pay the full $4,470 at the end of 6 weeks when services are complete. By December 31,2 weeks of services have been provided, but the business has not yet billed the customer or recorded the 2 weeks of services provided. 19 Close revenue accounts. Hint: Prepare financial statements before recording closing entries. 20 Close expense accounts. Hint: Prepare financial statements before recording closing entries. 21 Close Income Summary account. 22 Close Dividends account. Use the drop-downs to select the accounts properly included on the income statement. The unadjusted, adjusted, or post-closing balances will appear for each account, based on your selection. The unadjusted or adjusted balances will appear for each account, based on your selection. (Selecting Post-Closing will only display ending balance.) Use the drop-downs to select the accounts properly included on the balance sheet. The unadjusted, adjusted, or post-closing balances will appear for each account, based on your selection. Begin by selecting "Post-closing" from the drop-down below. Then, for each account, use the drop-down to indicate whether the account is included on the post-closing trial balance. Based on your decisions, the post-closing trial balance will be created. Compare your results with the Trial Balance tab

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Data Analysis And Sampling Simplified A Practical Guide For Internal Auditors

Authors: Donald A. Dickie PhD

1st Edition

1634540611, 978-1634540612