Answered step by step

Verified Expert Solution

Question

1 Approved Answer

please help. all information and steps are provided. The Smith's are a married couple in their mid-20's. Jane is an associate at a small law

please help. all information and steps are provided.

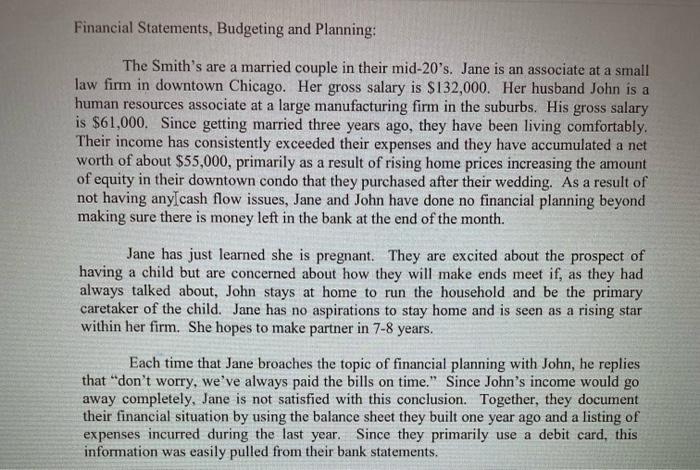

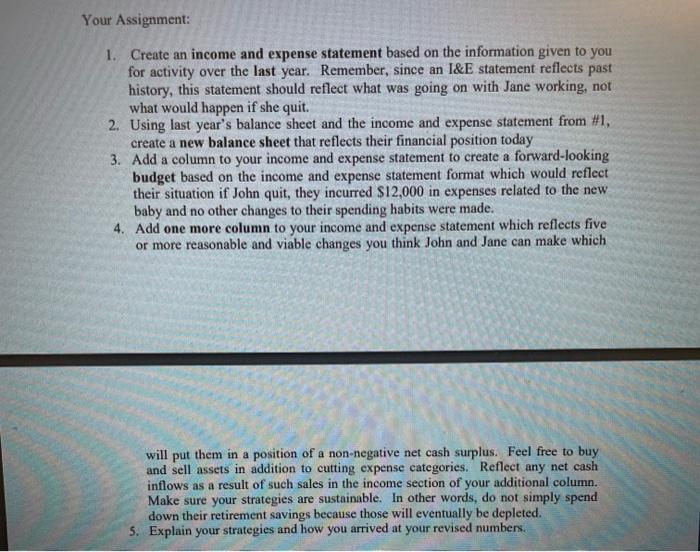

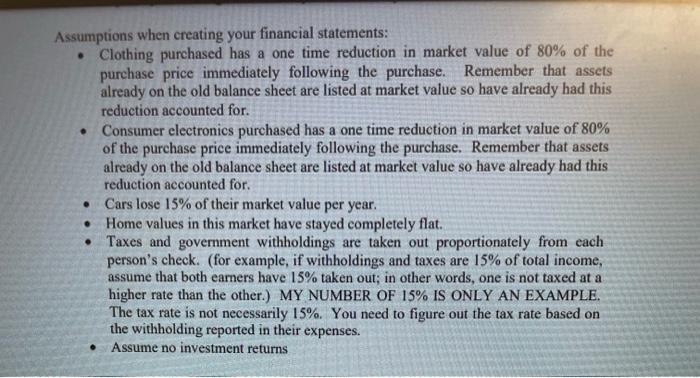

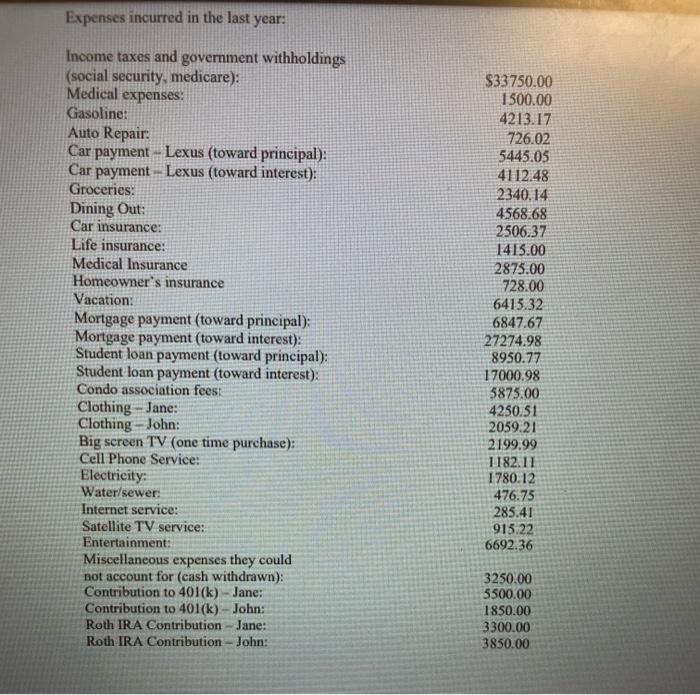

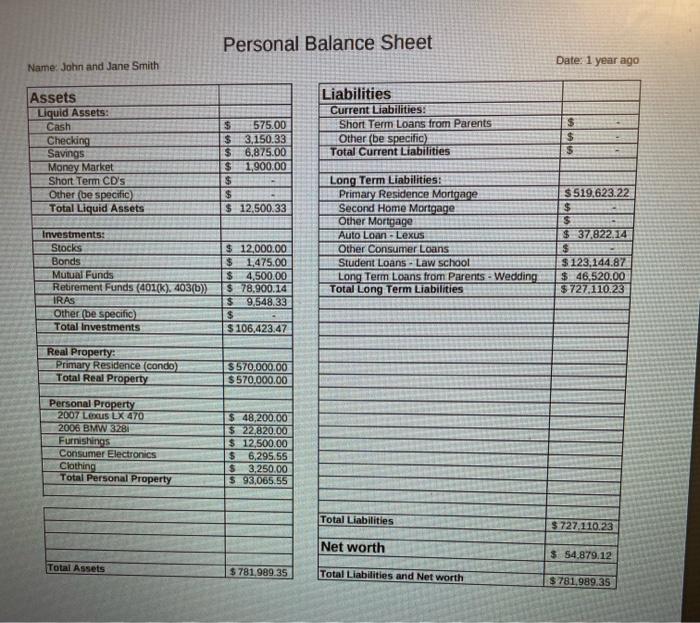

The Smith's are a married couple in their mid-20's. Jane is an associate at a small law firm in downtown Chicago. Her gross salary is $132,000. Her husband John is a human resources associate at a large manufacturing firm in the suburbs. His gross salary is $61,000. Since getting married three years ago, they have been living comfortably. Their income has consistently exceeded their expenses and they have accumulated a net worth of about $55,000, primarily as a result of rising home prices increasing the amount of equity in their downtown condo that they purchased after their wedding. As a result of not having anylcash flow issues, Jane and John have done no financial planning beyond making sure there is money left in the bank at the end of the month. Jane has just learned she is pregnant. They are excited about the prospect of having a child but are concerned about how they will make ends meet if, as they had always talked about, John stays at home to run the household and be the primary caretaker of the child. Jane has no aspirations to stay home and is seen as a rising star within her firm. She hopes to make partner in 7-8 years. Each time that Jane broaches the topic of financial planning with John, he replies that "don't worry, we've always paid the bills on time." Since John's income would go away completely, Jane is not satisfied with this conclusion. Together, they document their financial situation by using the balance sheet they built one year ago and a listing of expenses incurred during the last year. Since they primarily use a debit card, this information was easily pulled from their bank statements. 1. Create an income and expense statement based on the information given to you for activity over the last year. Remember, since an I\&E statement reflects past history, this statement should reflect what was going on with Jane working, not what would happen if she quit. 2. Using last year's balance sheet and the income and expense statement from #1, create a new balance sheet that reflects their financial position today 3. Add a column to your income and expense statement to create a forward-looking budget based on the income and expense statement format which would reflect their situation if John quit, they incurred $12,000 in expenses related to the new baby and no other changes to their spending habits were made. 4. Add one more column to your income and expense statement which reflects five or more reasonable and viable changes you think John and Jane can make which will put them in a position of a non-negative net cash surplus. Feel free to buy and sell assets in addition to cutting expense categories. Reflect any net cash inflows as a result of such sales in the income section of your additional column. Make sure your strategies are sustainable. In other words, do not simply spend down their retirement savings because those will eventually be depleted. 5. Explain your strategies and how you arrived at your revised numbers. Assumptions when creating your financial statements: - Clothing purchased has a one time reduction in market value of 80% of the purchase price immediately following the purchase. Remember that assets already on the old balance sheet are listed at market value so have already had this reduction accounted for. - Consumer electronics purchased has a one time reduction in market value of 80% of the purchase price immediately following the purchase. Remember that assets already on the old balance sheet are listed at market value so have already had this reduction accounted for. - Cars lose 15% of their market value per year. - Home values in this market have stayed completely flat. - Taxes and government withholdings are taken out proportionately from each person's check. (for example, if withholdings and taxes are 15% of total income, assume that both eamers have 15% taken out; in other words, one is not taxed at a higher rate than the other.) MY NUMBER OF 15\% IS ONLY AN EXAMPLE. The tax rate is not necessarily 15%. You need to figure out the tax rate based on the withholding reported in their expenses. - Assume no investment returns Expenses incurred in the last year: Income taxes and government withholdings (social security, medicare): Medical expenses: Gasoline: Auto Repair: Car payment-Lexus (toward principal): Car payment - Lexus (toward interest): Groceries: Dining Out: Car insurance: Life insurance: Medical Insurance Homeowner's insurance Vacation: Mortgage payment (toward principal): Mortgage payment (toward interest): Student loan payment (toward principal): Student loan payment (toward interest): Condo association fees: Clothing-Jane: Big screen TV (one time purchase): Cell Phone Service: Electricity: Water/sewer: Internet service: Satellite TV service: Entertainment: Miscellaneous expenses they could not account for (cash withdrawn): Contribution to 401(k) - Jane: Contribution to 401(k) - John: Roth IRA Contribution - Jane: Roth IRA Contribution - John: Personal Balance Sheet Date: 1 year ago Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Management For Decision Makers

Authors: Peter Atrill

8th Edition

129213433X, 978-1292134338