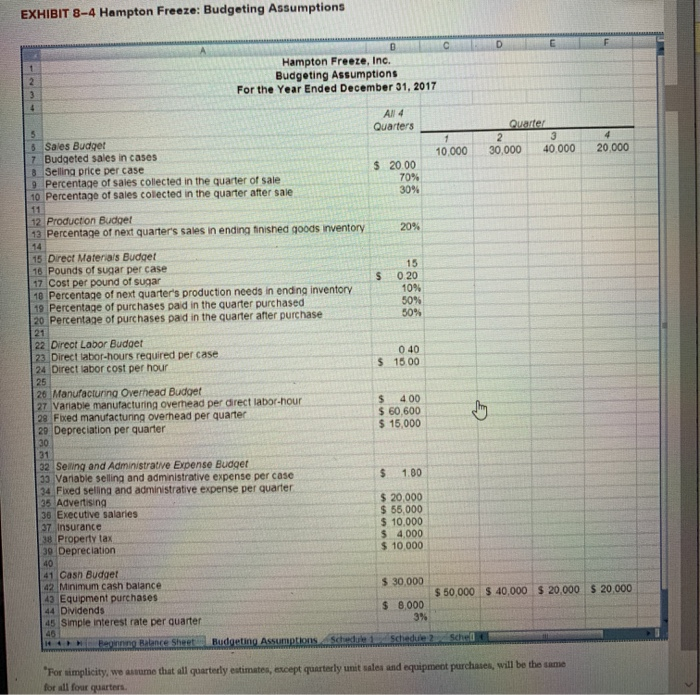

Please help formulate a budgeting assumption page provided by the above photos, please follow the template provided below

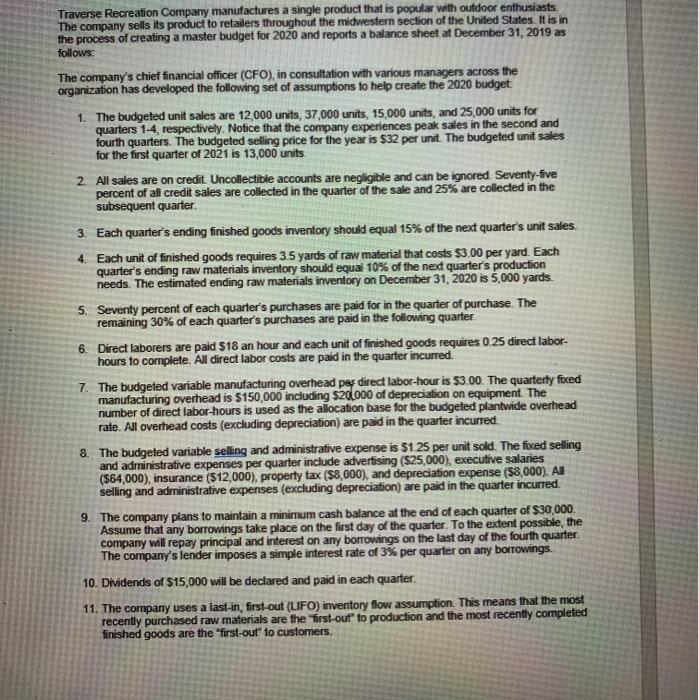

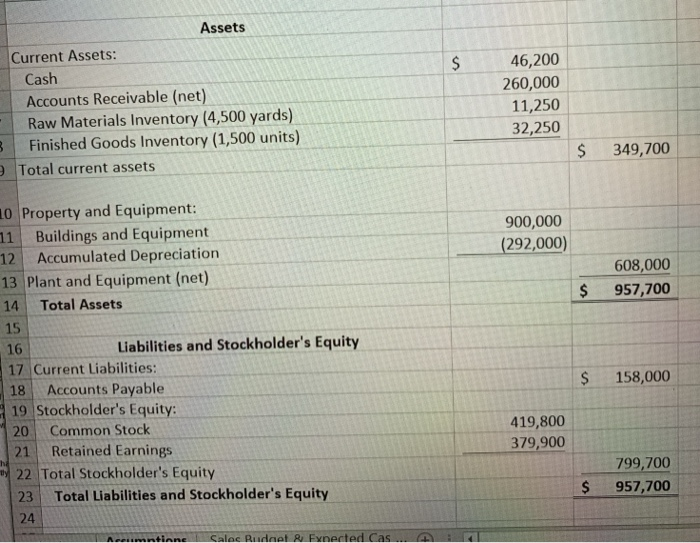

Traverse Recreation Company manufactures a single product that is popular with outdoor enthusiasts The company sells its product to retailers throughout the midwestern section of the United States. It is in haster budget for 2020 and reports a balance sheet at December 31, 2019 as follows: The company's chief financial officer (CFO), in consultation with various managers across the organization has developed the following set of assumptions to help create the 2020 budget 1. The budgeted unit sales are 12,000 units, 37,000 units, 15,000 units, and 25,000 units for quarters 1-4, respectively. Notice that the company experiences peak sales in the second and fourth quarters. The budgeted selling price for the year is $32 per unit. The budgeted unit sales for the first quarter of 2021 is 13,000 units 2. All sales are on credit. Uncollectible accounts are negligible and can be ignored. Seventy-five percent of al credit sales are collected in the quarter of the sale and 25% are collected in the subsequent quarter. 3. Each quarter's ending finished goods inventory should equal 15% of the next quarter's unit sales. 4. Each unit of finished goods requires 3.5 yards of raw material that costs $3.00 per yard. Each quarter's ending raw materials inventory should equal 10% of the ned quarter's production needs. The estimated ending raw materials inventory on December 31, 2020 is 5,000 yards. 5. Seventy percent of each quarter's purchases are paid for in the quarter of purchase. The remaining 30% of each quarter's purchases are paid in the following quarter 6. Direct laborers are paid $18 an hour and each unit of finished goods requires 0.25 direct labor- hours to complete. All direct labor costs are paid in the quarter incurred. 7. The budgeted variable manufacturing overhead pes direct labor-hour is $3.00. The quarterly fored manufacturing overhead is $150,000 including $20.000 of depreciation on equipment. The number of direct labor-hours is used as the allocation base for the budgeted plantwide overhead rate. All overhead costs (excluding depreciation) are paid in the quarter incurred. 8. The budgeted variable selling and administrative expense is $1.25 per unit sold. The fixed selling and administrative expenses per quarter include advertising ($25,000), executive salaries ($64,000), insurance ($12,000), property tax ($8,000), and depreciation expense ($8,000). Al selling and administrative expenses (excluding depreciation) are paid in the quarter incurred The company plans to maintain a minimum cash balance at the end of each quarter of $30,000. Assume that any borrowings take place on the first day of the quarter. To the extent possible, the company will repay principal and interest on any borrowings on the last day of the fourth quarter The company's lender imposes a simple interest rate of 3% per quarter on any borrowings. 10. Dividends of $15,000 will be declared and paid in each quarter. 11. The company uses a last-in, first-out (LIFO) inventory flow assumption. This means that the most recently purchased raw materials are the first-out" to production and the most recently completed finished goods are the "first-out to customers. Assets Current Assets: Cash Accounts Receivable (net) Raw Materials Inventory (4,500 yards) Finished Goods Inventory (1,500 units) Total current assets 46,200 260,000 11,250 32,250 $ 349,700 900,000 (292,000) 608,000 957,700 $ 16 10 Property and Equipment: 11 Buildings and Equipment 12 Accumulated Depreciation 13 Plant and Equipment (net) 14 Total Assets 15 Liabilities and Stockholder's Equity 17 Current Liabilities: 18 Accounts Payable 19 Stockholder's Equity: 20 Common Stock 21 Retained Earnings 22 Total Stockholder's Equity 23 Total Liabilities and Stockholder's Equity 24 Antiane Calec Rudent RFvnected Cas... A $ 158,000 419,800 379,900 799,700 957,700 $ EXHIBIT 8-4 Hampton Freeze: Budgeting Assumptions ODE Hampton Freeze, Inc. Budgeting Assumptions For the Year Ended December 31, 2017 AN 4 Quarters Quarter 10,000 30,000 40.000 20,000 3 Sales Budget 7 Budgeted sales in cases 8 Selling price per case 9 Percentage of sales collected in the quarter of sale 10 Percentage of sales collected in the quarter after sale $ 20.00 70% 30% 20% 15 12 Production Budget 13 Percentage of next quarter's sales in ending finished goods inventory 14 15 Direct Materials Budget 16 Pounds of sugar per case 17 Cost per pound of sugar 10 Percentage of next quarter's production needs in ending inventory 19 Percentage of purchases paid in the quarter purchased 20 Percentage of purchases paid in the quarter after purchase 0 20 10% 50% 50% 22 Direct Labor Budget 23 Direct labor-hours required percase 24 Direct labor cost per hour 0 40 15 00 26 Manufacturing Overhead Budget 27 Variable manufacturing overhead per direct labor-hour 29 Fied manufacturing overhead per quarter 29 Depreciation per quarter $ 400 $ 60,600 $ 15,000 $ 1.80 32 Selling and Administrative Expense Budget 33 Variable selling and administrative expense per case 34 Fixed selling and administrative expense per quarter 35 Advertising 36 Executive salaries 37 Insurance 38 Property tax 39 Depreciation $ 20,000 $ 55,000 $ 10,000 $ 4.000 $ 10.000 40 $ 30.000 $ 50,000 $ 40,000 $ 20.000 $ 20.000 41 Cash Budget 42 Minimum cash balance 43 Equipment purchases 44 Dividends 45 Simple interest rate per quarter ce Sheet $ 8,000 3% Budgeting Assumptions Schedule Schedule Sched "Por simplicity, we mume that all quarterly estimates, except quarterly unit sales and equipment purchases, will be the same for all four quarters