Please help help help

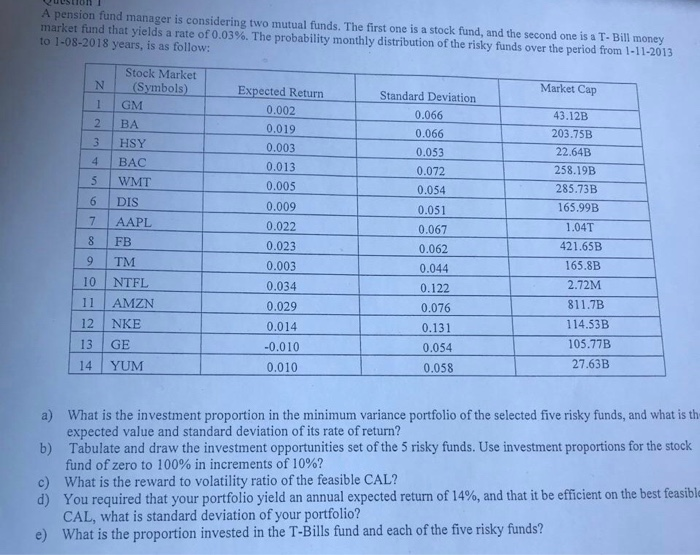

A pension fund manager is considering two mutual funds. The first one is a stock fund, and the second one is a T- Bill money market fund that yields a rate of 0.03%. The probability monthly distribution ofthe risky funds over the period from 1-11-2013 to 1-08-2018 years, is as follow: Stock Market (symbols) NI Market Cap Expected Return 0.002 0.019 0.003 0.013 0.005 0.009 0.022 0.023 0.003 0.034 0.029 0.014 0.010 0.010 GM 2 BA 3 HSY 4 BAC 5 WMT Standard Deviation 0.066 0.066 0.053 0.072 43.12B 203.75B 22.64B 258.19B 285.73B 165.99B 6 DIS 0.051 0.067 0.062 0.044 0.122 0.076 0.131 0.054 0.058 7AAPL 1.04 421.65B 8FB 9 TM 10 NTFL 11 AMZN 12 NKE 165.8B 2.72M 811.7B 114.53B 105.77B 27.63B 13 GE 14 YUM a) b) c) What is the investment proportion in the minimum variance portfolio of the selected five risky funds, and what is th expected value and standard deviation of its rate of return? Tabulate and draw the investment opportunities set of the 5 risky funds. Use investment proportions for the stock fund ofzero to 100% in increments of 10%? What is the reward to volatility ratio of the feasible CAL? You required that your portfolio yield an annual expected return of 14%, and that it be efficient on the best feasible CAL, what is standard deviation of your portfolio? What is the proportion invested in the T-Bills fund and each of the five risky funds? d) e) A pension fund manager is considering two mutual funds. The first one is a stock fund, and the second one is a T- Bill money market fund that yields a rate of 0.03%. The probability monthly distribution ofthe risky funds over the period from 1-11-2013 to 1-08-2018 years, is as follow: Stock Market (symbols) NI Market Cap Expected Return 0.002 0.019 0.003 0.013 0.005 0.009 0.022 0.023 0.003 0.034 0.029 0.014 0.010 0.010 GM 2 BA 3 HSY 4 BAC 5 WMT Standard Deviation 0.066 0.066 0.053 0.072 43.12B 203.75B 22.64B 258.19B 285.73B 165.99B 6 DIS 0.051 0.067 0.062 0.044 0.122 0.076 0.131 0.054 0.058 7AAPL 1.04 421.65B 8FB 9 TM 10 NTFL 11 AMZN 12 NKE 165.8B 2.72M 811.7B 114.53B 105.77B 27.63B 13 GE 14 YUM a) b) c) What is the investment proportion in the minimum variance portfolio of the selected five risky funds, and what is th expected value and standard deviation of its rate of return? Tabulate and draw the investment opportunities set of the 5 risky funds. Use investment proportions for the stock fund ofzero to 100% in increments of 10%? What is the reward to volatility ratio of the feasible CAL? You required that your portfolio yield an annual expected return of 14%, and that it be efficient on the best feasible CAL, what is standard deviation of your portfolio? What is the proportion invested in the T-Bills fund and each of the five risky funds? d) e)