Answered step by step

Verified Expert Solution

Question

1 Approved Answer

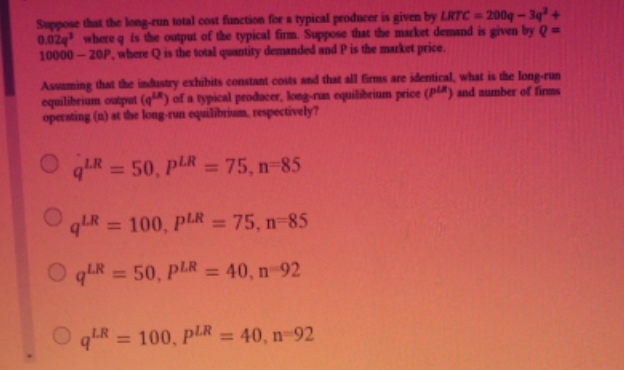

Please help hurry Suppose that the long-run intal cost function for a typical producer is given by LRTC = 200g - 3q' + 0.02q' where

Please help hurry

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Environmental Economics And Policy

Authors: Thomas H Tietenberg

5th Edition

0321348907, 9780321348906