Answered step by step

Verified Expert Solution

Question

1 Approved Answer

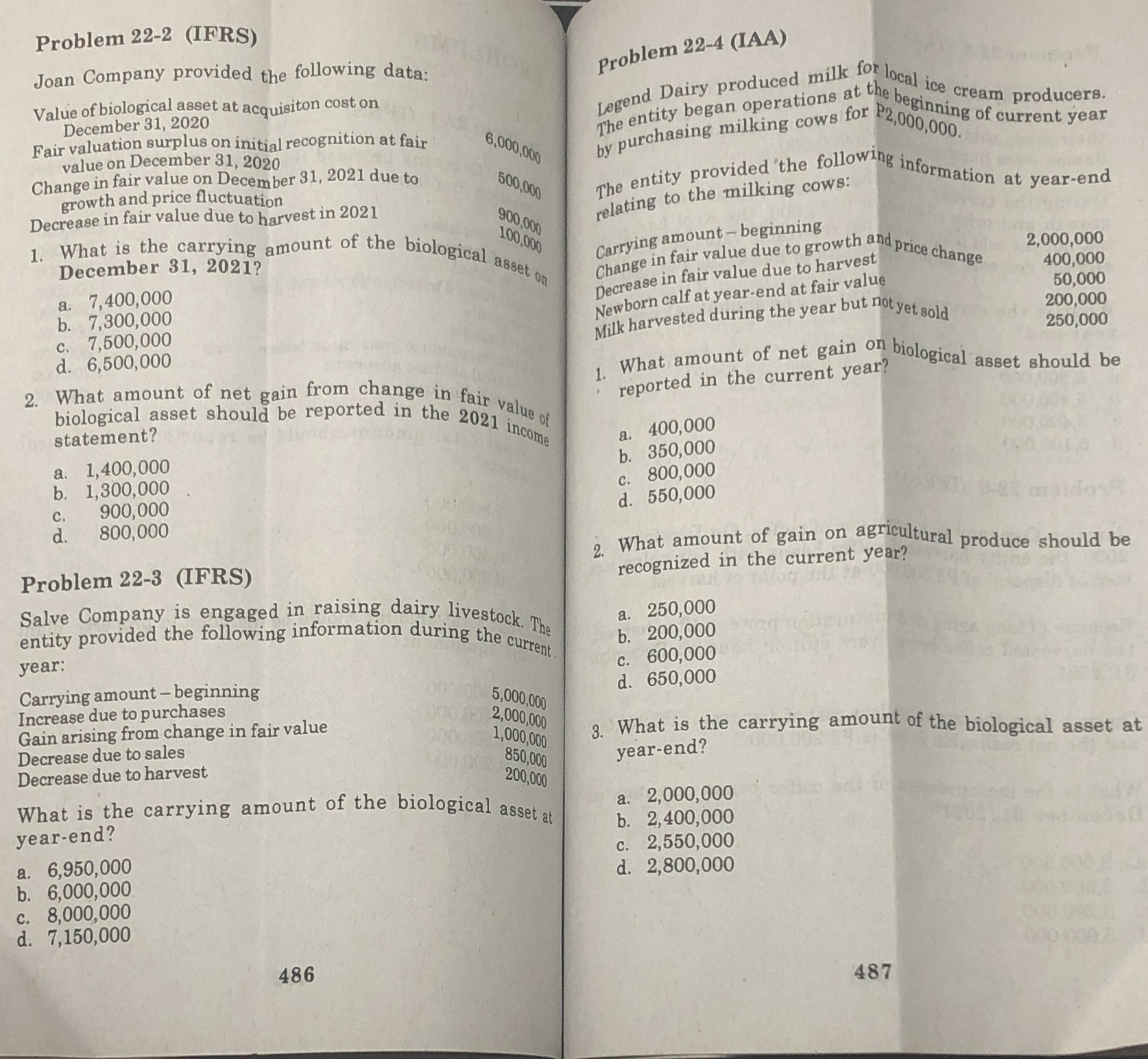

Please help me answer these problem with solution. Thank you Problem 22-2 (IFRS) Joan Company provided the following data: Problem 22-4 (IAA) Value of biological

Please help me answer these problem with solution. Thank you

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamental Financial Accounting Concepts

Authors: Thomas P. Edmonds, Frances M. Mcnair, Philip R. Olds, Mark Edmonds, Christopher Edmonds

10th Edition

126015940X, 978-1260159400