Please help me answer this question. I'm doing revison for my upcoming exam.

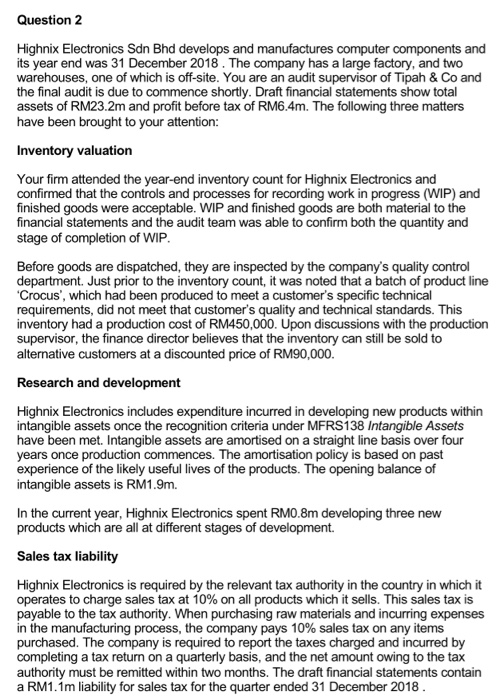

Question 2 Highnix Electronics Sdn Bhd develops and manufactures computer components and its year end was 31 December 2018. The company has a large factory, and two warehouses, one of which is off-site. You are an audit supervisor of Tipah & Co and the final audit is due to commence shortly. Draft financial statements show total assets of RM23.2m and profit before tax of RM6.4m. The following three matters have been brought to your attention: Inventory valuation Your firm attended the year-end inventory count for Highnix Electronics and confirmed that the controls and processes for recording work in progress (WIP) and finished goods were acceptable. WIP and finished goods are both material to the financial statements and the audit team was able to confirm both the quantity and stage of completion of WIP. Before goods are dispatched, they are inspected by the company's quality control department. Just prior to the inventory count, it was noted that a batch of product line Crocus', which had been produced to meet a customer's specific technical requirements, did not meet that customer's quality and technical standards. This inventory had a production cost of RM450,000. Upon discussions with the production supervisor, the finance director believes that the inventory can still be sold to alternative customers at a discounted price of RM90,000. Research and development Highnix Electronics includes expenditure incurred in developing new products within intangible assets once the recognition criteria under MFRS138 Intangible Assets have been met. Intangible assets are amortised on a straight line basis over four years once production commences. The amortisation policy is based on past experience of the likely useful lives of the products. The opening balance of intangible assets is RM1.9m. In the current year, Highnix Electronics spent RM0.8m developing three new products which are all at different stages of development Sales tax liability Highnix Electronics is required by the relevant tax authority in the country in which it operates to charge sales tax at 10% on all products which it sells. This sales tax is payable to the tax authority. When purchasing raw materials and incurring expenses in the manufacturing process, the company pays 10% sales tax on any items purchased. The company is required to report the taxes charged and incurred by completing a tax return on a quarterly basis, and the net amount owing to the tax authority must be remitted within two months. The draft financial statements contain a RM1.1m liability for sales tax for the quarter ended 31 December 2018 Required: Describe any SIX substantive procedures each, the auditor should perform to obtain sufficient and appropriate audit evidence in relation to (a) the VALUATION of Highnix 's inventory. (18 marks) (b) Highnix 's research and development expenditure. [18 marks] (c) Highnix 's year-end sales tax liability. (18 marks] The audit is now almost complete and the auditor's report is due to be signed shortly. The following matter has been brought to your attention: On 3 February 2019, a flood occurred at the off-site warehouse. This resulted in some damage to inventory and property, plant and equipment. However, there have been no significant delays to customer deliveries or complaints from customers. Highnix 's management has investigated the cause of the flooding and believes that the company is unlikely to be able to claim on its insurance. The finance director of Highnix Electronics has estimated that the value of damaged inventory and property, plant and equipment was RM0.7m and that it now has no scrap value. Required: (d) Explain whether the 2018 financial statements of Highnix Electronics require amendment in relation to the flood. [6 marks)