Please help me, I do not really understand these questions

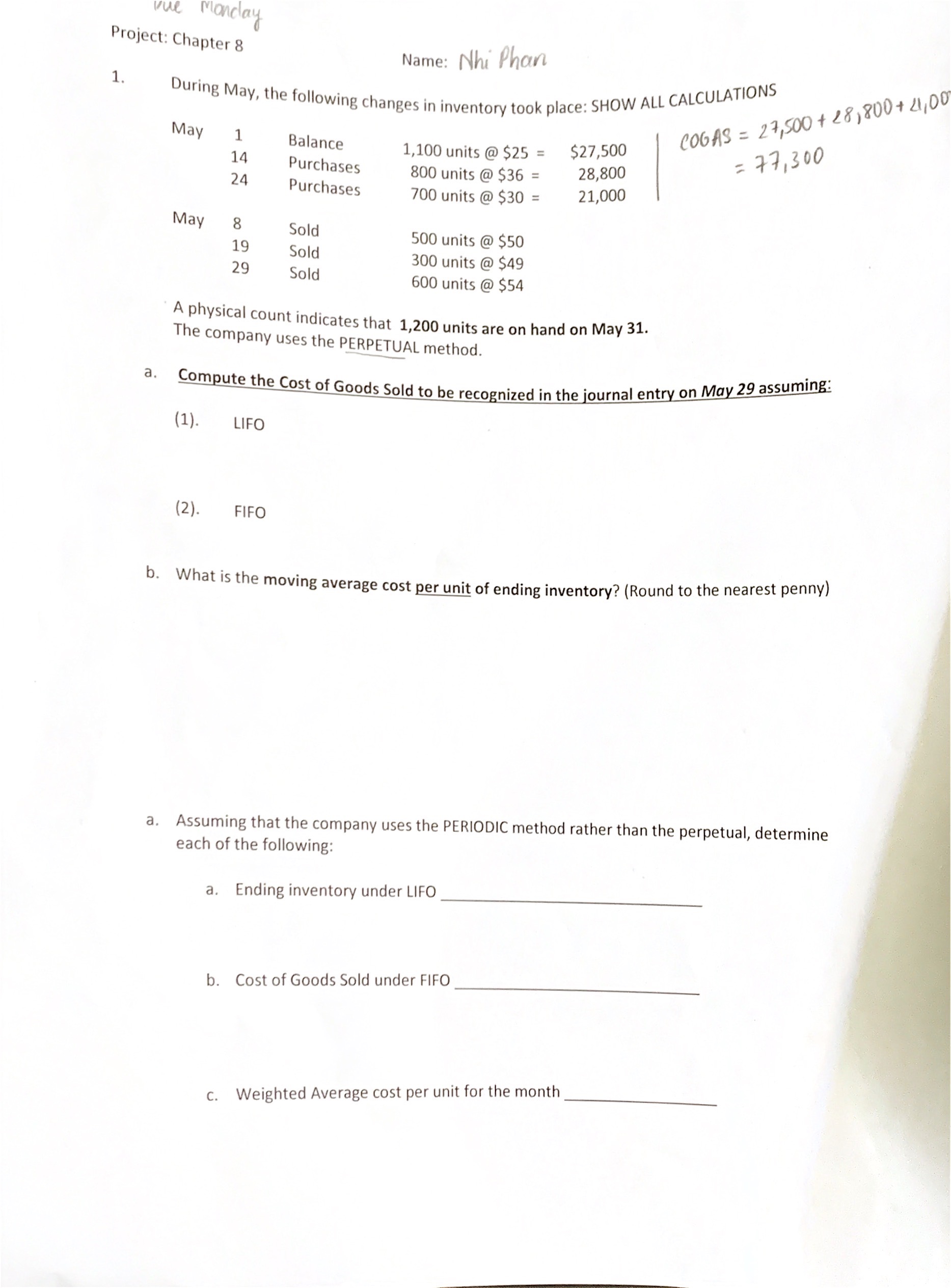

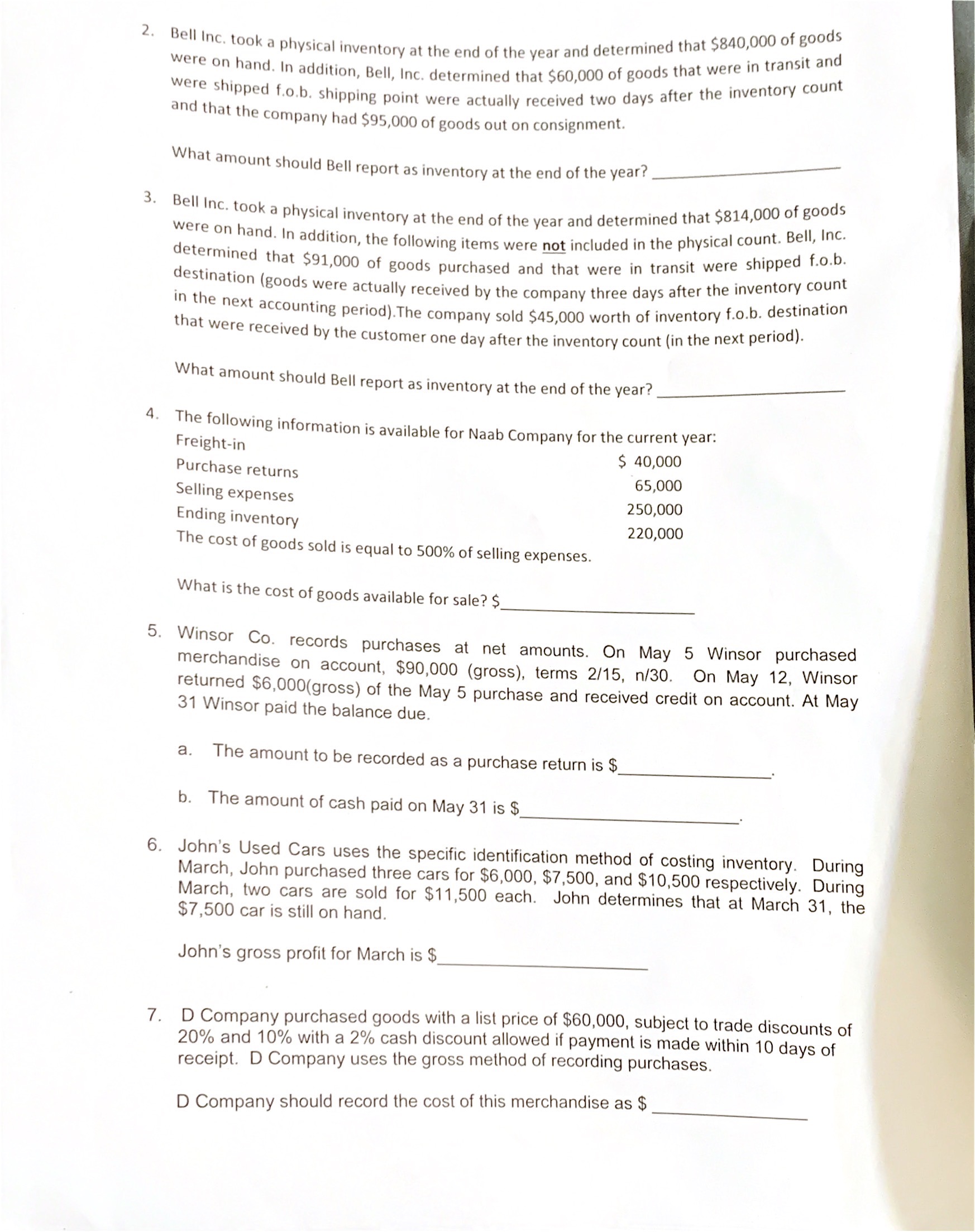

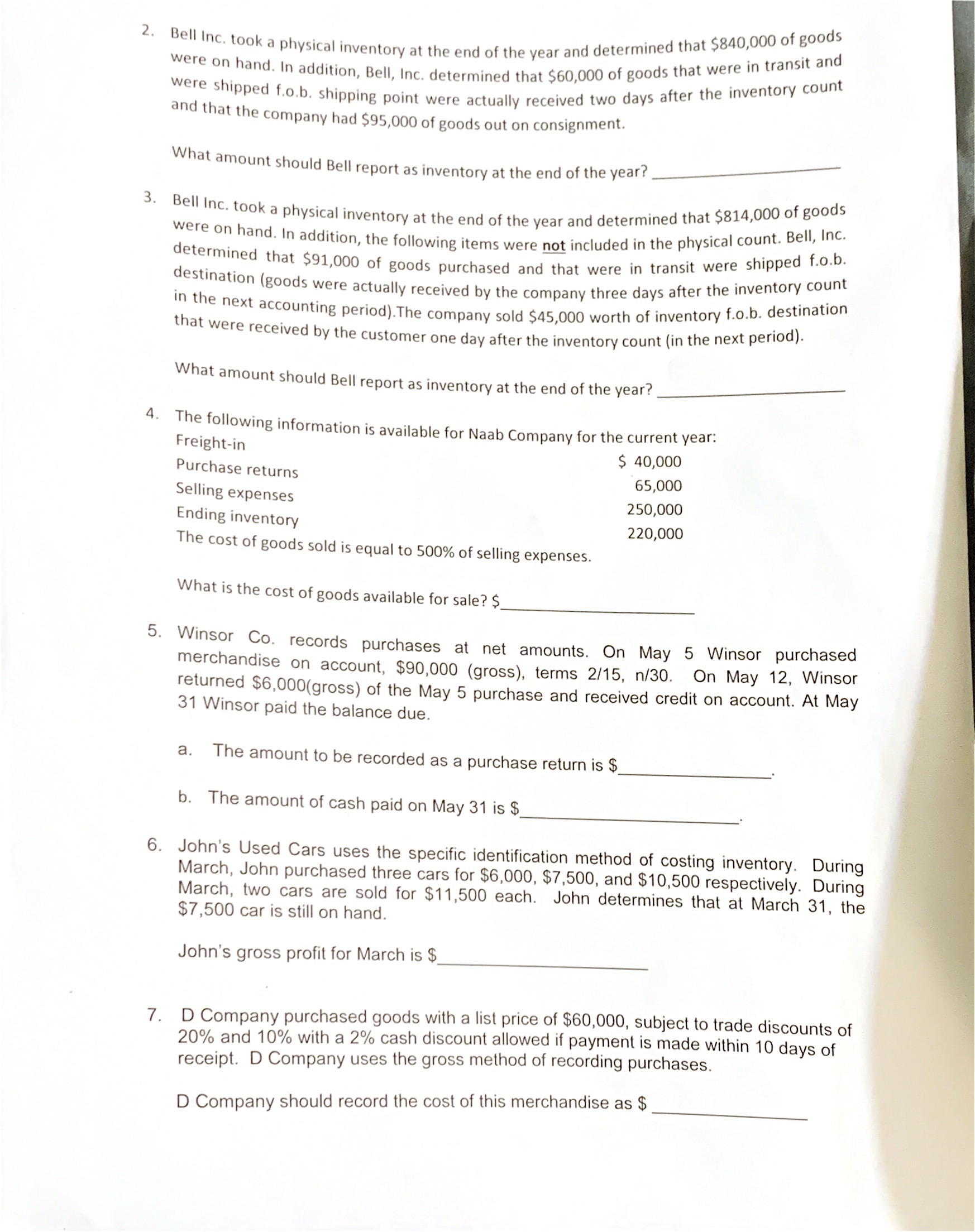

vue Monday Project: Chapter 8 Name: Nhi Phan 1. During May, the following changes in inventory took place: SHOW ALL CALCULATIONS COGAS = 27,500 + 28, 800+ 21,01 May 1 Balance = 77, 300 14 1,100 units @ $25 = $27,500 Purchases 24 800 units @ $36 = 28,800 Purchases 700 units @ $30 = 21,000 May 8 Sold 19 500 units @ $50 Sold 29 300 units @ $49 Sold 600 units @ $54 A physical count indicates that 1,200 units are on hand on May 31. The company uses the PERPETUAL method. a. Compute the Cost of Goods Sold to be recognized in the journal entry on May 29 assuming: (1). LIFO (2). FIFO b. What is the moving average cost per unit of ending inventory? (Round to the nearest penny) a. Assuming that the company uses the PERIODIC method rather than the perpetual, determine each of the following: a. Ending inventory under LIFO b. Cost of Goods Sold under FIFO c. Weighted Average cost per unit for the month2. Bell Inc. took a physical inventory at the end of the year and determined that $840,000 of goods were on hand. In addition, Bell, Inc. determined that $60,000 of goods that were in transit and were shipped f.o.b. shipping point were actually received two days after the inventory count and that the company had $95,000 of goods out on consignment. What amount should Bell report as inventory at the end of the year? 3. Bell Inc. took a physical inventory at the end of the year and determined that $814,000 of goods were on hand. In addition, the following items were not included in the physical count. Bell, Inc. determined that $91,000 of goods purchased and that were in transit were shipped f.o.b. destination (goods were actually received by the company three days after the inventory count in the next accounting period). The company sold $45,000 worth of inventory f.o.b. destination that were received by the customer one day after the inventory count (in the next period). What amount should Bell report as inventory at the end of the year? 4. The following information is available for Naab Company for the current year: Freight-in $ 40,000 Purchase returns 65,000 Selling expenses 250,000 Ending inventory 220,000 The cost of goods sold is equal to 500% of selling expenses. What is the cost of goods available for sale? $. 5. Winsor Co. records purchases at net amounts. On May 5 Winsor purchased merchandise on account, $90,000 (gross), terms 2/15, n/30. On May 12, Winsor returned $6,000(gross) of the May 5 purchase and received credit on account. At May 31 Winsor paid the balance due. a. The amount to be recorded as a purchase return is $. b. The amount of cash paid on May 31 is $. 6. John's Used Cars uses the specific identification method of costing inventory. During March, John purchased three cars for $6,000, $7,500, and $10,500 respectively. During March, two cars are sold for $11,500 each. John determines that at March 31, the $7,500 car is still on hand. John's gross profit for March is $ 7. D Company purchased goods with a list price of $60,000, subject to trade discounts of 20% and 10% with a 2% cash discount allowed if payment is made within 10 days of receipt. D Company uses the gross method of recording purchases. D Company should record the cost of this merchandise as $