Answered step by step

Verified Expert Solution

Question

1 Approved Answer

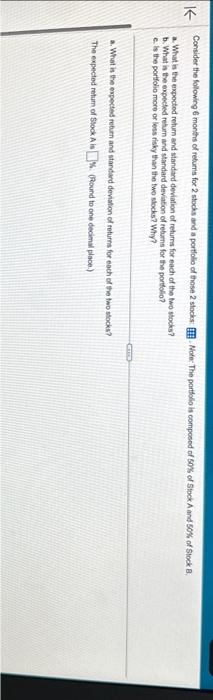

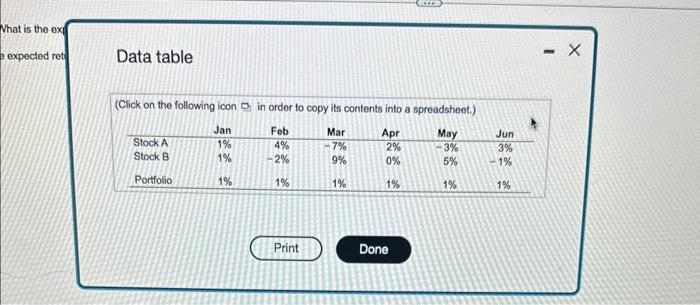

please help me learn Consider the folowing 6 months of rebums foe 2 stocks and a portlolio of these 2 slockst Wore- The partlolio is

please help me learn

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Secret Language Of Money How To Make Smarter Financial Decisions And Live A Richer Life

Authors: David Krueger, John David Mann

1st Edition

0071623396,007171314X