please help me solve this question

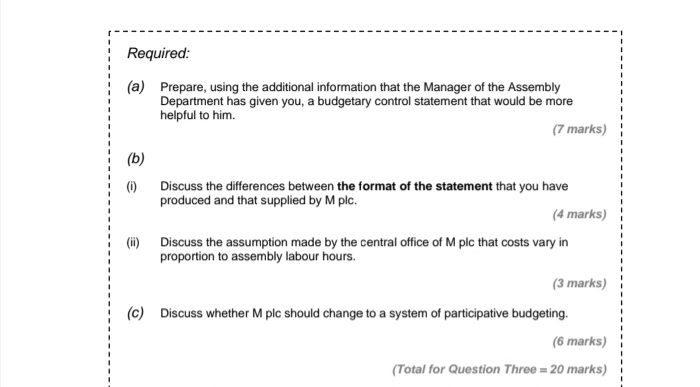

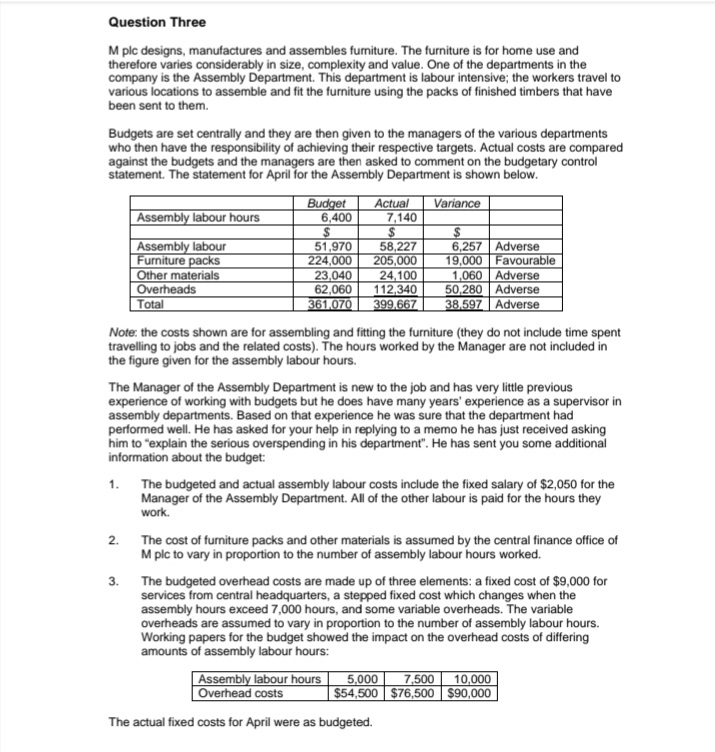

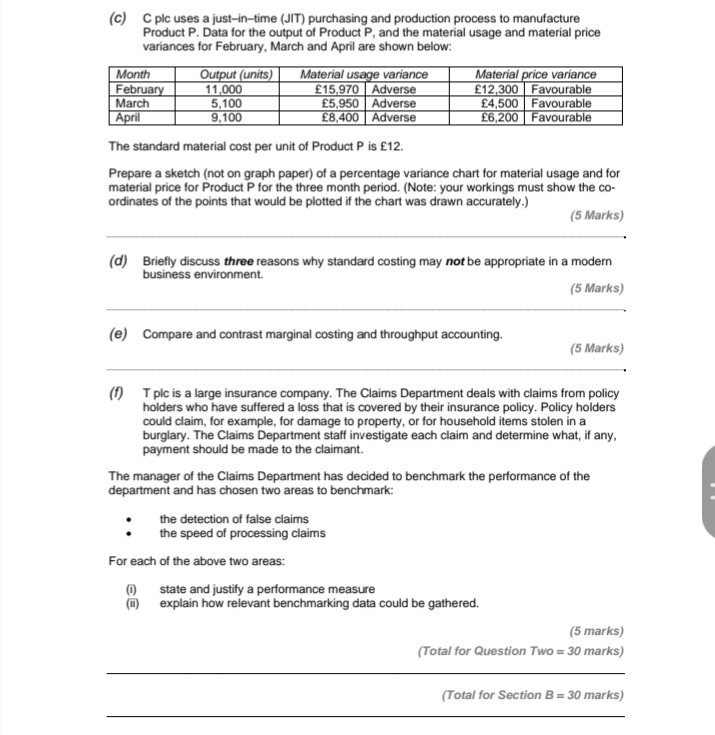

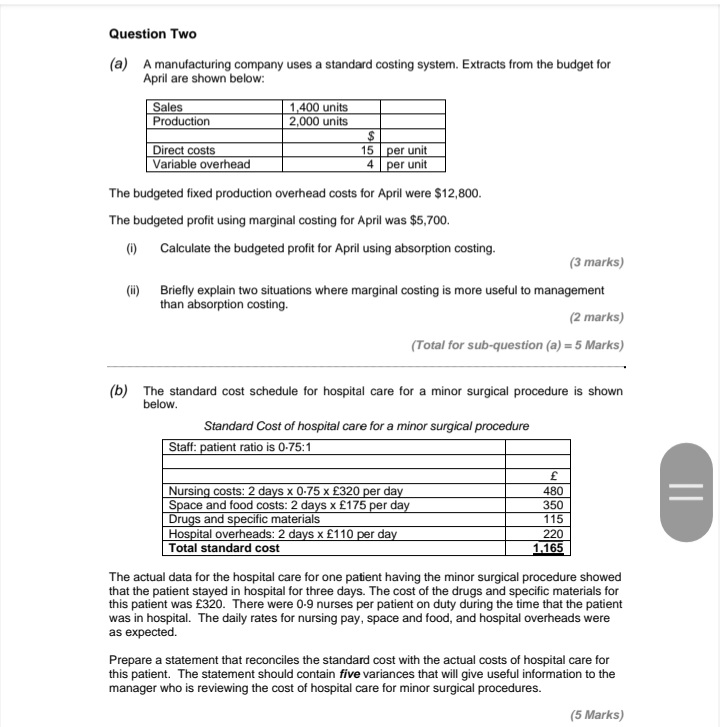

Required: (a) Prepare, using the additional information that the Manager of the Assembly Department has given you, a budgetary control statement that would be more helpful to him. (7 marks) (b) Discuss the differences between the format of the statement that you have produced and that supplied by M plc. (4 marks) (ii) Discuss the assumption made by the central office of M pic that costs vary in proportion to assembly labour hours. (3 marks) (c) Discuss whether M pic should change to a system of participative budgeting. (6 marks) (Total for Question Three = 20 marks)Question Three M plc designs, manufactures and assembles fumiture. The furniture is for home use and therefore varies considerably in size, complexity and value. One of the departments in the company is the Assembly Department. This department is labour intensive; the workers travel to various locations to assemble and fit the furniture using the packs of finished timbers that have been sent to them. Budgets are set centrally and they are then given to the managers of the various departments who then have the responsibility of achieving their respective targets. Actual costs are compared against the budgets and the managers are then asked to comment on the budgetary control statement. The statement for April for the Assembly Department is shown below. Budget Actual Variance Assembly labour hours 6,400 7,140 $ $ Assembly labour 51,970 58,227 6,257 Adverse Furniture packs 224,000 205,000 19,000 Favourable Other materials 23,040 24,100 1,060 Adverse Overheads 62,060 112,340 50,280 | Adverse Tota 361.070 399.667 38.597 | Adverse Note: the costs shown are for assembling and fitting the furniture (they do not include time spent travelling to jobs and the related costs). The hours worked by the Manager are not included in the figure given for the assembly labour hours. The Manager of the Assembly Department is new to the job and has very little previous experience of working with budgets but he does have many years' experience as a supervisor in assembly departments. Based on that experience he was sure that the department had performed well. He has asked for your help in replying to a memo he has just received asking him to "explain the serious overspending in his department". He has sent you some additional information about the budget: 1 . The budgeted and actual assembly labour costs include the fixed salary of $2,050 for the Manager of the Assembly Department. All of the other labour is paid for the hours they work. 2. The cost of furniture packs and other materials is assumed by the central finance office of M pic to vary in proportion to the number of assembly labour hours worked. 3. The budgeted overhead costs are made up of three elements: a fixed cost of $9,000 for services from central headquarters, a stepped fixed cost which changes when the assembly hours exceed 7,000 hours, and some variable overheads. The variable overheads are assumed to vary in proportion to the number of assembly labour hours. Working papers for the budget showed the impact on the overhead costs of differing amounts of assembly labour hours: Assembly labour hours 5,000 7,500 10,000 Overhead costs $54,500 $76,500 $90,000 The actual fixed costs for April were as budgeted.(c) C pic uses a just-in-time (JIT) purchasing and production process to manufacture Product P. Data for the output of Product P, and the material usage and material price variances for February, March and April are shown below: Month Output (units) Material usage variance Material price variance February 11,000 $15,970 Adverse E12,300 Favourable March 5,100 E5,950 Adverse E4,500 Favourable April 9,100 E8,400 Adverse E6,200 Favourable The standard material cost per unit of Product P is $12. Prepare a sketch (not on graph paper) of a percentage variance chart for material usage and for material price for Product P for the three month period. (Note: your workings must show the co- ordinates of the points that would be plotted if the chart was drawn accurately.) (5 Marks) (d) Briefly discuss three reasons why standard costing may not be appropriate in a modern business environment. (5 Marks) (e) Compare and contrast marginal costing and throughput accounting. (5 Marks) (f) T plc is a large insurance company. The Claims Department deals with claims from policy holders who have suffered a loss that is covered by their insurance policy. Policy holders could claim, for example, for damage to property, or for household items stolen in a burglary. The Claims Department staff investigate each claim and determine what, if any, payment should be made to the claimant. The manager of the Claims Department has decided to benchmark the performance of the department and has chosen two areas to benchmark: the detection of false claims . . the speed of processing claims For each of the above two areas: state and justify a performance measure explain how relevant benchmarking data could be gathered. (5 marks) (Total for Question Two = 30 marks) (Total for Section B = 30 marks)Question Two (a) A manufacturing company uses a standard costing system. Extracts from the budget for April are shown below: Sales 1,400 units Production 2,000 units Direct costs 15 per unit Variable overhead 4 per unit The budgeted fixed production overhead costs for April were $12,800. The budgeted profit using marginal costing for April was $5,700. (1) Calculate the budgeted profit for April using absorption costing. (3 marks) (ii) Briefly explain two situations where marginal costing is more useful to management than absorption costing. (2 marks) (Total for sub-question (a) = 5 Marks) (b) The standard cost schedule for hospital care for a minor surgical procedure is shown below. Standard Cost of hospital care for a minor surgical procedure Staff: patient ratio is 0.75:1 E Nursing costs: 2 days x 0-75 x E320 per day 480 Space and food costs: 2 days x $175 per day 350 Drugs and specific materials 1 15 Hospital overheads: 2 days x 110 per day 220 Total standard cost 1.165 The actual data for the hospital care for one patient having the minor surgical procedure showed that the patient stayed in hospital for three days. The cost of the drugs and specific materials for this patient was E320. There were 0-9 nurses per patient on duty during the time that the patient was in hospital. The daily rates for nursing pay, space and food, and hospital overheads were as expected. Prepare a statement that reconciles the standard cost with the actual costs of hospital care for this patient. The statement should contain five variances that will give useful information to the manager who is reviewing the cost of hospital care for minor surgical procedures