Answered step by step

Verified Expert Solution

Question

1 Approved Answer

please help me to solve this question, thx: ) i am stuck in it. Consider the following riskless bonds which can be bought or sold

please help me to solve this question, thx: )

i am stuck in it.

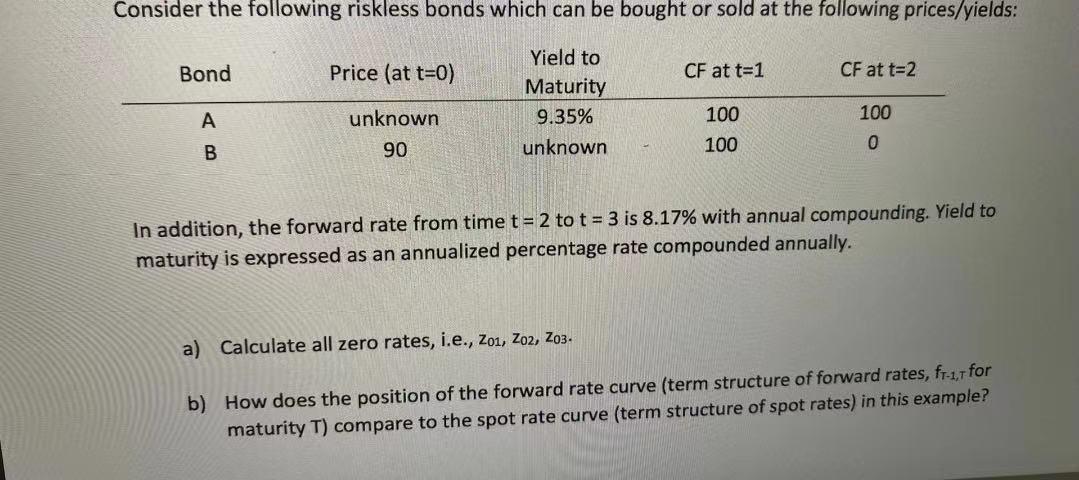

Consider the following riskless bonds which can be bought or sold at the following prices/yields: Bond Price (at t=0) CF at t=1 CF at t=2 Yield to Maturity 9.35% unknown 100 unknown 90 100 0 100 B In addition, the forward rate from time t = 2 to t = 3 is 8.17% with annual compounding. Yield to maturity is expressed as an annualized percentage rate compounded annually. a) Calculate all zero rates, i.e., 201, 202, 203. b) How does the position of the forward rate curve (term structure of forward rates, fr-1,7 for maturity T) compare to the spot rate curve (term structure of spot rates) in this exampleStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Money Banking And Financial Markets

Authors: Stephen G. Cecchetti

1st Edition

0072452692, 9780072452693