Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please help me with filling the missing value (in Brown) ---- Thanks Calculate the Value of the Call Option using the Black Scholes Model and

Please help me with filling the missing value (in Brown) ---- Thanks

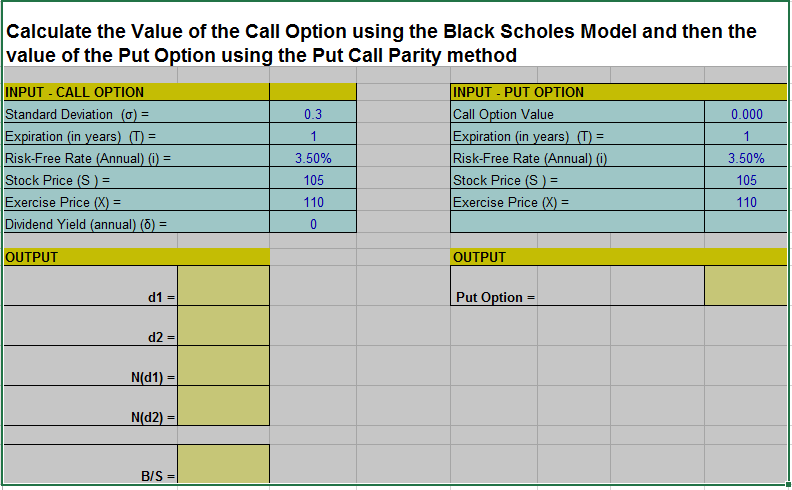

Calculate the Value of the Call Option using the Black Scholes Model and then the value of the Put Option using the Put Call Parity method

Calculate the Value of the Call Option using the Black Scholes Model and then the value of the Put Option using the Put Call Parity method INPUT CALL OPTION Standard Deviation ()= Expiration (in vears Risk-Free Rate (Annual) (i) = Stock Price (S ) = Exercise Price (X = Dividend Yield (annual) (6) = INPUT- PUT OPTION Call Option Value Expiration (in vears Risk-Free Rate (Annual Stock Price (S ) = Exercise Price (X = 0.3 0.000 3.50% 105 110 3.50% 105 110 OUTPUT OUTPUT Put Option = d2 = N(d1) = N(d2) = B/S =Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Final Audit In Pursuit Of Nazi War Booty Compulsively Readable And Superbly Narrated Dlied With Love Suspense Insight Wisdom And Dry Humor

Authors: Carnie Matisonn

1st Edition

1452094845, 978-1452094847