Please help me with how to calculate the below entries that are not correct.

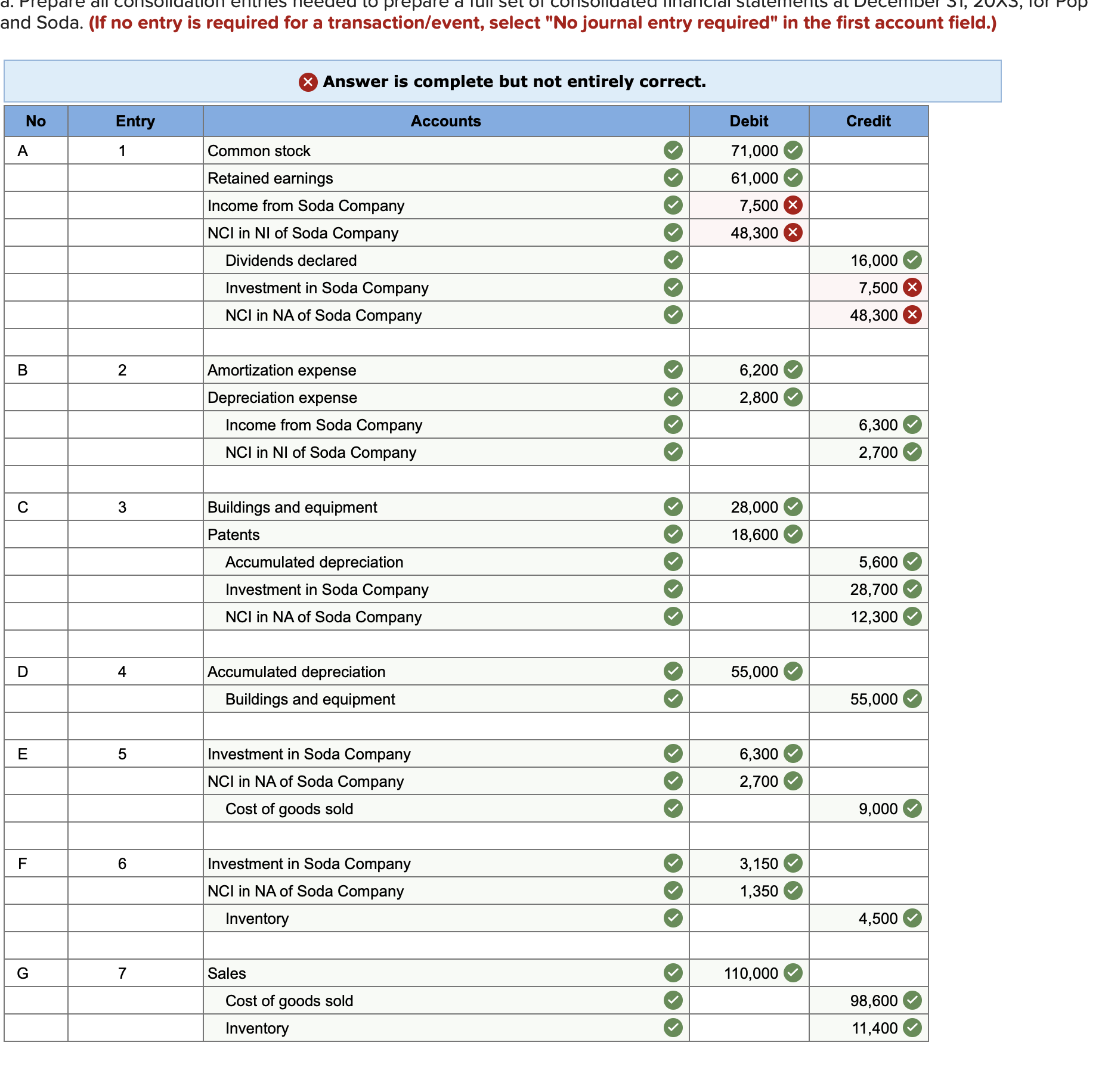

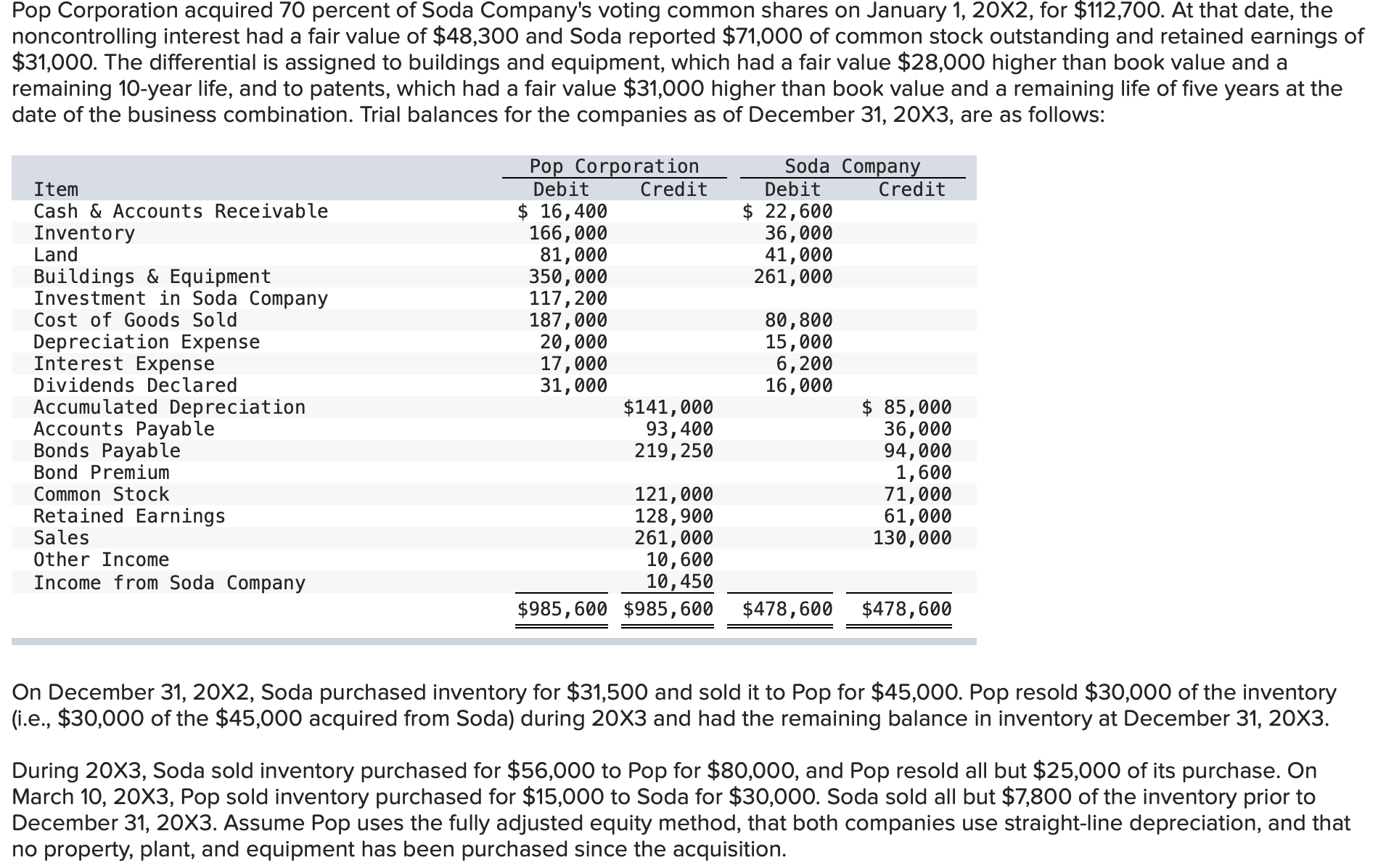

and Soda. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field.) x Answer is complete but not entirely correct. No Entry Accounts Debit Credit A 1 Common stock 71,000 Retained earnings 61,000 Income from Soda Company O 7,500 X NCI in NI of Soda Company 48,300 X Dividends declared 16,000 Investment in Soda Company 7,500 X NCI in NA of Soda Company 48,300 X B 2 Amortization expense 6,200 Depreciation expense 2,800 Income from Soda Company 6,300 NCI in NI of Soda Company 2,700 C 3 Buildings and equipment 28,000 Patents 18,600 Accumulated depre 5,600 Investment in Soda Company 28,700 NCI in NA of Soda Company 12,300 D 4 Accumulated depreciation 65,000 Buildings and equipment 55,000 E 5 Investment in Soda Company 6,300 NCI in NA of Soda Company O 2,700 Cost of goods sold 9,000 F 6 Investment in Soda Company 3, 150 NCI in NA of Soda Company 1,350 Inventory 4,500 G 7 Sales 110,000 Cost of goods sold 98,600 nventory 11,400Pop Corporation acquired 70 percent of Soda Company's voting common shares on January 1, 20x2, for $112,700. At that date, the noncontrolling interest had a fair value of $48,300 and Soda reported $71,000 of common stock outstanding and retained earnings of $31,000. The differential is assigned to buildings and equipment, which had a fair value $28,000 higher than book value and a remaining 10year life, and to patents, which had a fair value $31,000 higher than book value and a remaining life of five years at the date of the business combination. Trial balances for the companies as of December 31, 20x3, are as follows: Pop Corporation Soda Company Item Debit Credit Debit Credit Cash & Accounts Receivable $ 16.400 $ 22.500 Inventory 166,000 36,000 Land 81,000 41,000 Buildings & Equipment 350,000 261,000 Investment in Soda Company 117,200 Cost of Goods Sold 187,000 80,800 Depreciation Expense 20,000 15,000 Interest Expense 17,000 6,200 Dividends Declared 31,000 16,000 Accumulated Depreciation $141,000 $ 85,000 Accounts Payable 93,400 36,000 Bonds Payable 219,250 94,000 Bond Premium 1,600 Common Stock 121,000 71,000 Retained Earnings 128,900 61,000 Sales 261,000 130,000 Other Income 10,600 Income from Soda Company 10,450 $985,600 $985,600 $478,600 $478,600 On December 31, 20x2, Soda purchased inventory for $31,500 and sold it to Pop for $45,000. Pop resold $30,000 of the inventory (i.e., $30,000 of the $45,000 acquired from Soda) during 20x3 and had the remaining balance in inventory at December 31, 20x3. During 20x3, Soda sold inventory purchased for $56,000 to Pop for $80,000, and Pop resold all but $25,000 of its purchase. On March 10, 20x3, Pop sold inventory purchased for $15,000 to Soda for $30,000. Soda sold all but $7,800 of the inventory prior to December 31, 20x3. Assume Pop uses the fully adjusted equity method, that both companies use straight-line depreciation, and that no property, plant, and equipment has been purchased since the acquisition