Question

Please help me with these questions. I really need some help. Please answers ALL 8 questions. Please show work for each question that required any

Please help me with these questions. I really need some help. Please answers ALL 8 questions. Please show work for each question that required any mathematical solution.

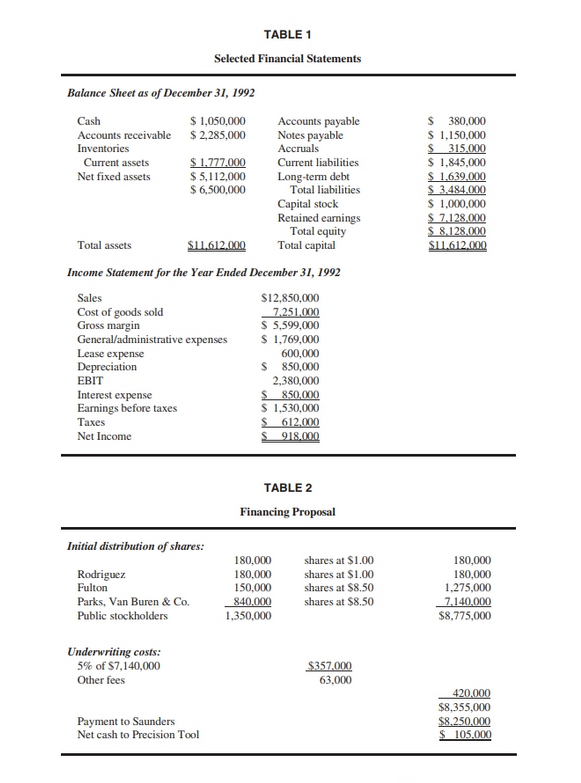

In late 1992, two executives of Workman Tool, Inc., the largest privately owned corporation in Ohio, decided to start a company of their own. There were two primary reasons for their decision. First, both men had the entrepreneurial spirit and longed to have a shot at their own business. Second, Workmans ownership structure precluded managers from receiving stock options as part of their compensation package. Thus, although the firm was generous in its salaries and bonuses, everything was subject to immediate taxation. Both men thought that a new business would give them the opportunity to defer taxes on a large part of their overall compensation. The two men, Julio Rodriguez and Toby Fulton, found a medium-sized precision tool company that was on the market. The company, Precision Tool Company, is wholly owned by its founder, Nick Sanders. Although the company is in sound condition, Sanders, who is in his late 40s, recently suffered a heart attack and was advised by his doctor to sell the firm and relaxor else. Sanders is asking $8,250,000 for the firm, which works out to a Price/Earnings ratio of approximately 9x, and he has given Rodriguez and Fulton a 6-month purchase option to allow the pair time to arrange financing. Rodriguez contacted Paul Van Buren, a partner in the New York City investment banking firm of Aberwald, Butler, Van Buren & Company, to help arrange the needed financing. Rodriguez and Fulton each have some savings to put into the purchase, but they need a substantial amount of outside capital to complete the deal. Although the funds could probably be borrowed, Van Buren is not enthusiastic about this alternative. For one thing, Precision Tools debt ratio is currently at 30 percent, which is the industry average (see Table 1). Second, Rodriguez and Fulton envision using Precision Tool as a vehicle to acquire several smaller companies, and some reserve debt capacity would be needed if this strategy is pursued. Van Buren proposes that the two partners obtain funds to purchase Precision Tool in accordance with the schedule shown in Table 2. Precision Tool would be restructured with 6 million common shares authorized1,350,000 shares to be issued at the time of the sale and 4,650,000 shares to be held in reserve for future acquisitions. Rodriguez and Fulton would each purchase 180,000 shares at a price of $1 per share, the par value. Aberwald, Butler, Van Buren & Company would purchase 150,000 shares at a price of $8.50 and the remaining 840,000 shares would be sold to the public at the $8.50 price. The underwriting fee to Aberwald, Butler, Van Buren & Company would be 5 percent of the proceeds from the public sale, or $357,000. Legal fees, accounting fees, and other charges would amount to $63,000, for total underwriting costs of $420,000. After deducting the underwriting charges and the payment to Sanders, the restructured Precision Tool would have an additional $105,000 in its cash account. Also as part of the agreement would be a provision which grants 1-year options to purchase additional shares. Rodriguez and Fulton could collectively purchase an additional 120,000 shares, while Parks, Van Buren & Company could purchase an additional 100,000 shares, all at $8.50.

A second financing alternative is also being considered, although Van Buren is less

enthusiastic about this approach. Van Buren has made some preliminary inquiries to Silverman Sachs, a San Francisco investment-banking house which specializes in junk-bond financing. It looks like $6 million of high yield bonds could be sold to help finance the acquisition. However, these bonds would require a coupon rate of 18 percent. With the alternatives in mind, Rodriguez and Fulton must now make their financing

decision. Van Buren believes that the financing could be obtained within ninety days once the decision is made. He also suggested that the partners develop some pro forma income statements for 1993, which reflect the impact of the two alternative financing plans. The partners believe that sales would grow by 10 percent under

their leadership, and that cost of goods sold and

general/administrative expenses would be about the same percentage of sales as in 1992. Lease and depreciation expenses would remain at their 1992 levels, while interest expense would be the 1992 level plus interest on any new debt percent issued. The firms federal-plus-state tax rate is 40.

1. Using the data in Table 2, calculate the total flotation costs as a percentage of external funds raised. How does this amount compare with published averages for the cost of selling new common stock? (For now, ignore the value of the options.)

2. Assume that Precision Tools stock price one year from now has the following probability distribution

| probability | price |

| 0.05 | 3.50 |

| 0.10 | 7.00 |

| 0.35 | 12.50 |

| 0.35 | 13.90 |

| 0.10 | 19.40 |

| 0.05 | 22.90 |

a. What is the additional expected dollar benefit to Aberwald, Butler, Van Buren & Company from the option package?

b. Disregarding the time value of money, what would be the total underwriting expense expressed as a percentage of funds raised?

3. Considering that the public would be paying $8.50 per share, should Rodriguez and Fulton be allowed to purchase their shares for $1.00? Should the public be informed that the insiders are paying a lower price, and if so, how?

4. In light of your answer to Question 3, should Aberwald, Butler, Van Buren & Company be allowed to purchase its shares for $1.00 per share?

5. As stated at the beginning of the case, Rodriguez and Fulton are motivated partly by the urge to own and run their own firm. What would be the partners ownership position under the proposal?

6. One goal of the proposal is to generate excess cash now that could potentially be used in the future for acquisitions. What are the pros and cons of raising the funds now rather than when needed?

7. Now consider the junk bond financing alternative. a. Construct pro forma income statements for 1993 for the two financing alternatives. b. What are the times-interest-earned, fixed charge coverage, and cash flow coverage ratios under each alternative?

8. What should Rodriguez and Fultons final decision be? Fully support your answer. Are there any other financing alternatives that should be considered

TABLE 1 Selected Financial Statements Balance Sheet as of December 31, 1992 S 380,000 1,150,000 S 1,845,000 S1639.000 S 1,000,000 Cash S1,050,000 Accounts payable Accounts receivable 2,285,000 Notes payable Current assets Net fixed assets S1,777,000 5,112,000 $ 6,500,000 Accruals Current liabilities Long-term debt Total iabilities Capital stock Retained earnings Total equity Total assets SL612.000 capital Income Statement for the Year Ended December 31, 1992 Sales Cost of goods sold Gross margin General/administrative expenses Lease expense $12,850,000 7251000 S 5,599,000 S 1,769,000 600,000 S 850,000 2,380,000 EBIT Interest expense Earnings before taxes Taxes Net Income 50,00 S 1,530,000 TABLE 2 Financing Proposal Initial distribution of shares 180,000 180,000 150,000 shares at $1.00 shares at $1.00 shares at $8.50 shares at $8.50 180,000 180,000 1,275,000 7.140,000 $8,775,000 Rodriguez Fulton Parks, Van Buren& Co.-840000 Public stockholders 1,350,000 Underwriting costs: 5% of S7, 140.000 Other fees $357000 63,000 $8,355.000 Payment to Saunders Net cash to Precision Tool TABLE 1 Selected Financial Statements Balance Sheet as of December 31, 1992 S 380,000 1,150,000 S 1,845,000 S1639.000 S 1,000,000 Cash S1,050,000 Accounts payable Accounts receivable 2,285,000 Notes payable Current assets Net fixed assets S1,777,000 5,112,000 $ 6,500,000 Accruals Current liabilities Long-term debt Total iabilities Capital stock Retained earnings Total equity Total assets SL612.000 capital Income Statement for the Year Ended December 31, 1992 Sales Cost of goods sold Gross margin General/administrative expenses Lease expense $12,850,000 7251000 S 5,599,000 S 1,769,000 600,000 S 850,000 2,380,000 EBIT Interest expense Earnings before taxes Taxes Net Income 50,00 S 1,530,000 TABLE 2 Financing Proposal Initial distribution of shares 180,000 180,000 150,000 shares at $1.00 shares at $1.00 shares at $8.50 shares at $8.50 180,000 180,000 1,275,000 7.140,000 $8,775,000 Rodriguez Fulton Parks, Van Buren& Co.-840000 Public stockholders 1,350,000 Underwriting costs: 5% of S7, 140.000 Other fees $357000 63,000 $8,355.000 Payment to Saunders Net cash to Precision ToolStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

ISE Essentials Of Investments

Authors: Zvi Bodie, Alex Kane, Alan Marcus

12th International Edition

1265450099, 9781265450090