Question

Please help provide a correct solution with a detailed explanation to part (e)-(g) . The same part (a)-(d) has been posted on Chegg as well,

Please help provide a correct solution with a detailed explanation to part (e)-(g). The same part (a)-(d) has been posted on Chegg as well, feel free to answer those part on the other post.

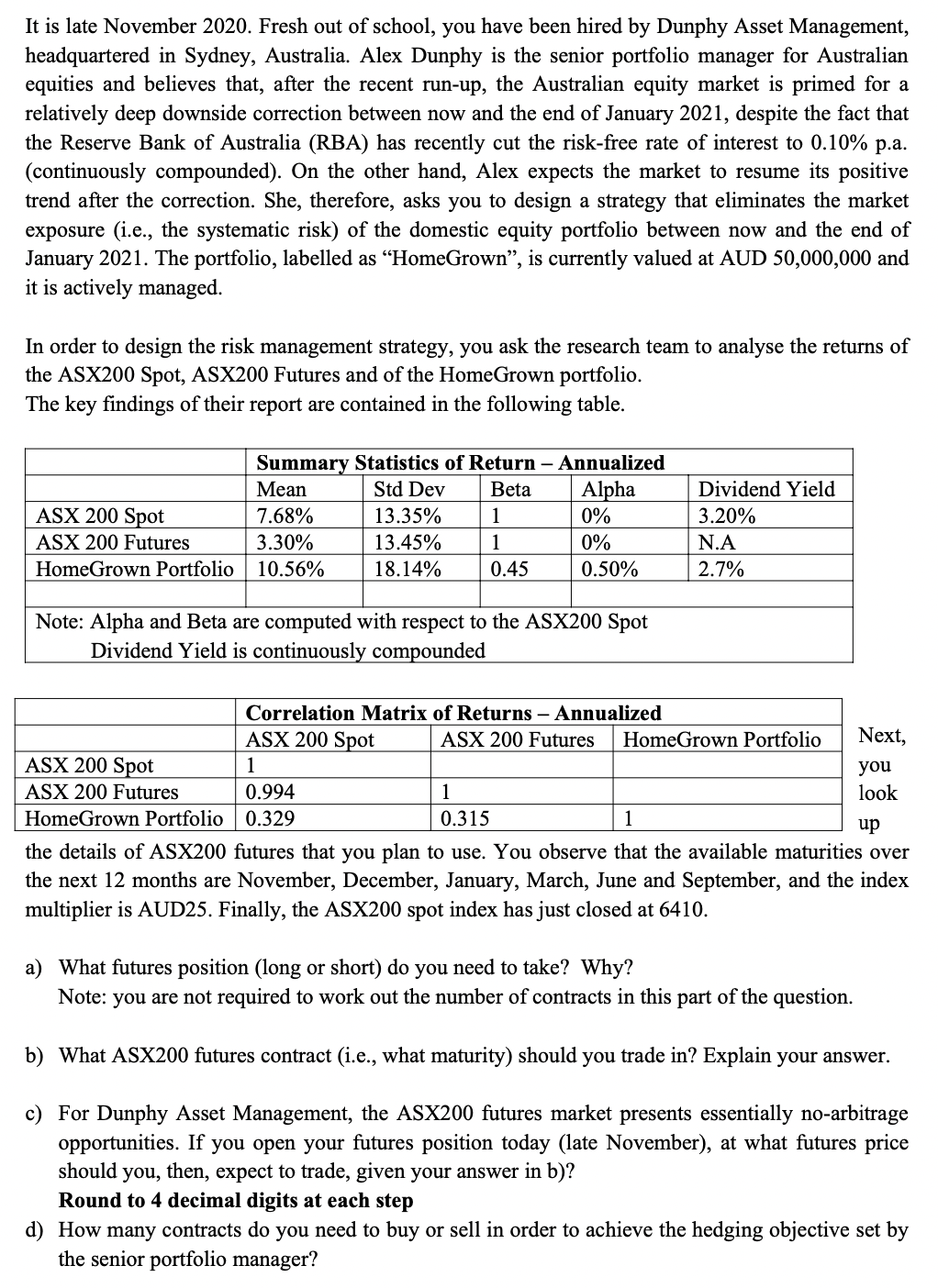

It is late November 2020. Fresh out of school, you have been hired by Dunphy Asset Management, headquartered in Sydney, Australia. Alex Dunphy is the senior portfolio manager for Australian equities and believes that, after the recent run-up, the Australian equity market is primed for a relatively deep downside correction between now and the end of January 2021, despite the fact that the Reserve Bank of Australia (RBA) has recently cut the risk-free rate of interest to 0.10% p.a. (continuously compounded). On the other hand, Alex expects the market to resume its positive trend after the correction. She, therefore, asks you to design a strategy that eliminates the market exposure (i.e., the systematic risk) of the domestic equity portfolio between now and the end of January 2021. The portfolio, labelled as HomeGrown, is currently valued at AUD 50,000,000 and it is actively managed. In order to design the risk management strategy, you ask the research team to analyse the returns of the ASX200 Spot, ASX200 Futures and of the Home Grown portfolio. The key findings of their report are contained in the following table. ASX 200 Spot ASX 200 Futures Home Grown Portfolio Summary Statistics of Return - Annualized Mean Std Dev Beta Alpha 7.68% 13.35% 1 0% 3.30% 13.45% 1 0% 10.56% 18.14% 0.45 0.50% Dividend Yield 3.20% N.A 2.7% Note: Alpha and Beta are computed with respect to the ASX200 Spot Dividend Yield is continuously compounded Correlation Matrix of Returns - Annualized ASX 200 Spot ASX 200 Futures Home Grown Portfolio Next ASX 200 Spot 1 you ASX 200 Futures 0.994 1 look Home Grown Portfolio 0.329 0.315 1 up the details of ASX200 futures that you plan to use. You observe that the available maturities over the next 12 months are November, December, January, March, June and September, and the index multiplier is AUD25. Finally, the ASX200 spot index has just closed at 6410. a) What futures position (long or short) do you need to take? Why? Note: you are not required to work out the number of contracts in this part of the question. b) What ASX200 futures contract (i.e., what maturity) should you trade in? Explain your answer. c) For Dunphy Asset Management, the ASX200 futures market presents essentially no-arbitrage opportunities. If you open your futures position today (late November), at what futures price should you, then, expect to trade, given your answer in b)? Round to 4 decimal digits at each step d) How many contracts do you need to buy or sell in order to achieve the hedging objective set by the senior portfolio manager? e) Does the hedging strategy that you recommend above leave the HomeGrown portfolio exposed to basis risk? Why or why not? f) Given the data above and given the hedging strategy you recommend, what do you expect the return on the hedged HomeGrown portfolio to be between late November 2020 and late January 2021? g) You also call a bank that quotes you a 2-month forward price of 6400.00 for the ASX200. Dunphy Asset Management prefers to stick with futures and does not want to hear about arbitrage strategies for the Home Grown portfolio. However, you can legally advise your good friend George Costanza about those opportunities. Mr. Costanza was given by his generous father-in-law a $100,000 equity portfolio which closely mirrors the ASX200. Do you see a free- lunch opportunity for Mr. Costanza? If so, what trading strategy would you recommend Mr. Costanza to implement on his own portfolio? Provide the details of the trading strategy and, hence, of the $ amount of the arbitrage profit (if any). It is late November 2020. Fresh out of school, you have been hired by Dunphy Asset Management, headquartered in Sydney, Australia. Alex Dunphy is the senior portfolio manager for Australian equities and believes that, after the recent run-up, the Australian equity market is primed for a relatively deep downside correction between now and the end of January 2021, despite the fact that the Reserve Bank of Australia (RBA) has recently cut the risk-free rate of interest to 0.10% p.a. (continuously compounded). On the other hand, Alex expects the market to resume its positive trend after the correction. She, therefore, asks you to design a strategy that eliminates the market exposure (i.e., the systematic risk) of the domestic equity portfolio between now and the end of January 2021. The portfolio, labelled as HomeGrown, is currently valued at AUD 50,000,000 and it is actively managed. In order to design the risk management strategy, you ask the research team to analyse the returns of the ASX200 Spot, ASX200 Futures and of the Home Grown portfolio. The key findings of their report are contained in the following table. ASX 200 Spot ASX 200 Futures Home Grown Portfolio Summary Statistics of Return - Annualized Mean Std Dev Beta Alpha 7.68% 13.35% 1 0% 3.30% 13.45% 1 0% 10.56% 18.14% 0.45 0.50% Dividend Yield 3.20% N.A 2.7% Note: Alpha and Beta are computed with respect to the ASX200 Spot Dividend Yield is continuously compounded Correlation Matrix of Returns - Annualized ASX 200 Spot ASX 200 Futures Home Grown Portfolio Next ASX 200 Spot 1 you ASX 200 Futures 0.994 1 look Home Grown Portfolio 0.329 0.315 1 up the details of ASX200 futures that you plan to use. You observe that the available maturities over the next 12 months are November, December, January, March, June and September, and the index multiplier is AUD25. Finally, the ASX200 spot index has just closed at 6410. a) What futures position (long or short) do you need to take? Why? Note: you are not required to work out the number of contracts in this part of the question. b) What ASX200 futures contract (i.e., what maturity) should you trade in? Explain your answer. c) For Dunphy Asset Management, the ASX200 futures market presents essentially no-arbitrage opportunities. If you open your futures position today (late November), at what futures price should you, then, expect to trade, given your answer in b)? Round to 4 decimal digits at each step d) How many contracts do you need to buy or sell in order to achieve the hedging objective set by the senior portfolio manager? e) Does the hedging strategy that you recommend above leave the HomeGrown portfolio exposed to basis risk? Why or why not? f) Given the data above and given the hedging strategy you recommend, what do you expect the return on the hedged HomeGrown portfolio to be between late November 2020 and late January 2021? g) You also call a bank that quotes you a 2-month forward price of 6400.00 for the ASX200. Dunphy Asset Management prefers to stick with futures and does not want to hear about arbitrage strategies for the Home Grown portfolio. However, you can legally advise your good friend George Costanza about those opportunities. Mr. Costanza was given by his generous father-in-law a $100,000 equity portfolio which closely mirrors the ASX200. Do you see a free- lunch opportunity for Mr. Costanza? If so, what trading strategy would you recommend Mr. Costanza to implement on his own portfolio? Provide the details of the trading strategy and, hence, of the $ amount of the arbitrage profit (if any)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cost Benefit Analysis

Authors: Harry F. Campbell, Richard P.C. Brown

3rd Edition

1032320753, 9781032320755