please help provide statement of cashflows

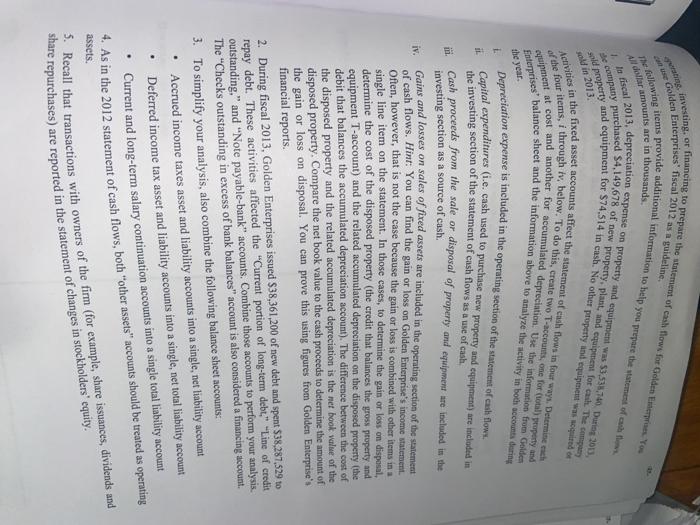

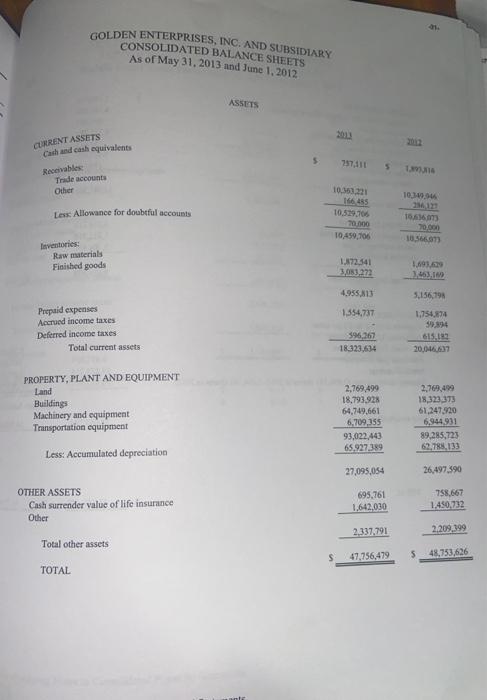

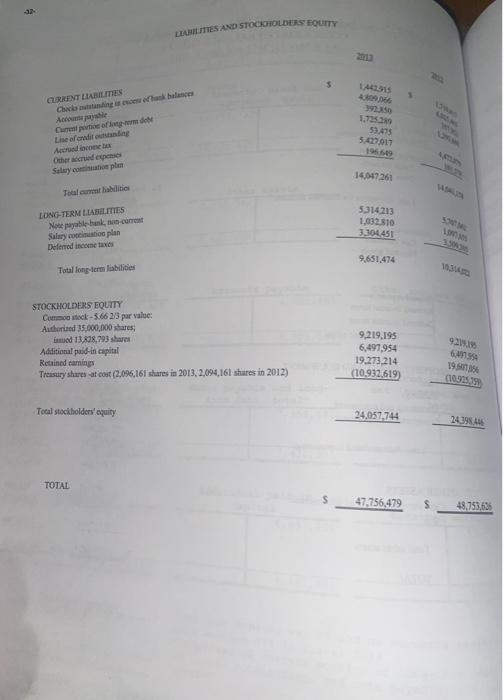

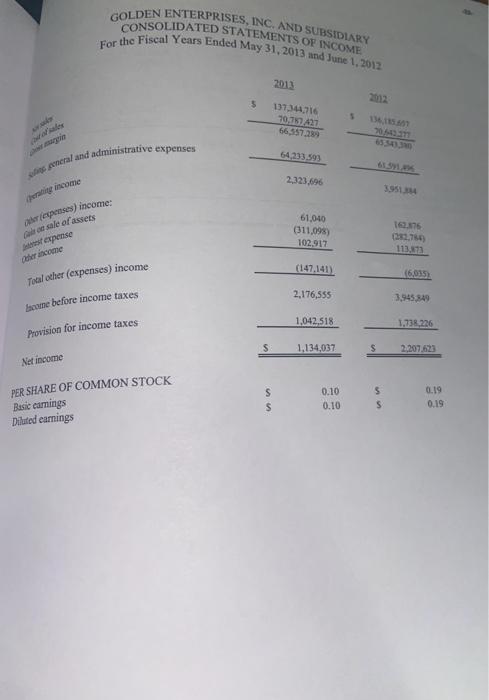

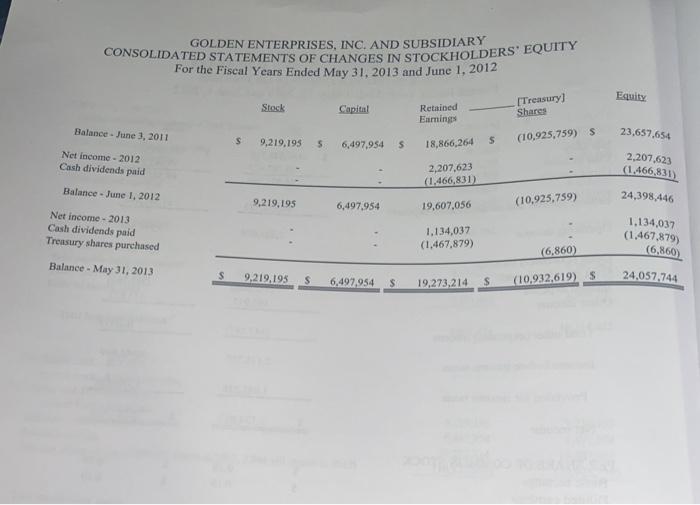

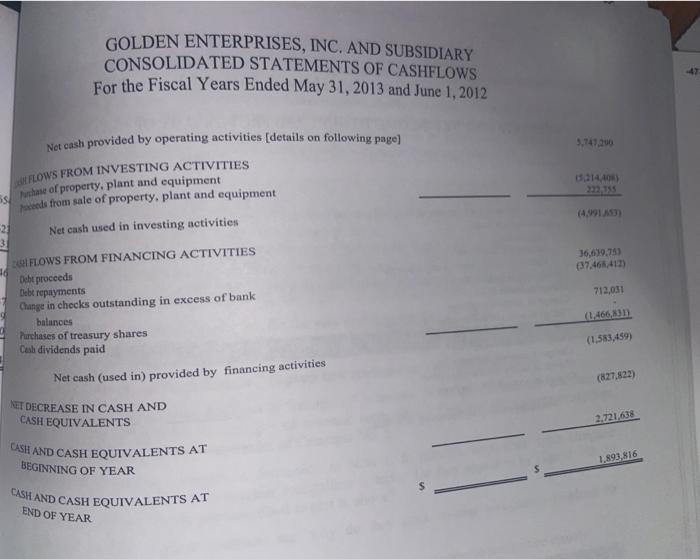

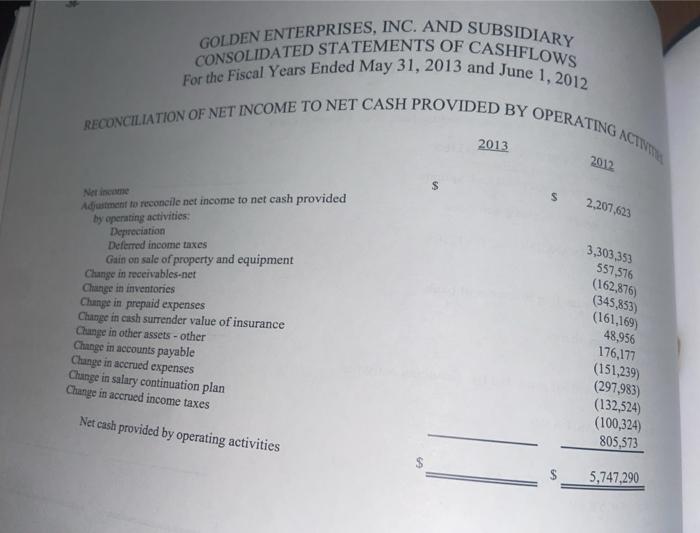

8. Construct the 2013 statement of cash flows for Golden Enterprises using the indirect method. Recall that the change in cash (i.e., the statement of cash flows) is algebraically related to the balance sheet as follows: A Cash - A Liabilities + A Owners' Equity - A All Other Assets Thus, if you can "explain the change in each of the noncash balance sheet accounts (and only those accounts), you will have generated a statement of cash flows. Use a set of T-accounts for the balance sheet accounts (T-accounts are included at the end of the case) or a spreadsheet to help you organize your efforts. For each balance sheet account, consider what transactions and activities explain the change in the account. Classify each transaction and activity as Or financing to prepare the statement of cash flows for Golden Eve You rate, investing the year cose Golden Enterprises fiscal 2012 as a guideline The following items provide additional information to help you prepare the statement of the se company purchased $4,149,678 of new property, plant, and equipment for cash. The company sold property and equipment for $74.514 in cash. No other property and equipment of the four items, i through tv, below. To do this, create two T-accounts, one for (total property and Activities in the fixed asset accounts affect the statement of cash flows in four ways. Determinach Enterprises balance sheet and the information above to analyze the activity in both scoring Depreciation expense is included in the operating section of the statement of cash flow Capital expenditures of the ashensed to purchase new property and equipment) are included in the investing section of the statement of cash flows as a use of cash. Cash proceeds from the sale or disposal of property and equipment are included in the investing section as a source of cash. Gains and losses on sales of fixed assets are included in the operating section of the statement of cash flows. Hint: You can find the gain or loss on Golden Enterprise's income statement. Often, however, that is not the case because the gain or loss is combined with other items in a single line item on the statement. In those cases, to determine the gain or loss on disposal, determine the cost of the disposed property (the credit that balances the gross property and equipment T-account) and the related accumulated depreciation on the disposed property (the debit that balances the accumulated depreciation account). The difference between the cost of the disposed property and the related accumulated depreciation is the net book value of the disposed property. Compare the net book value to the cash proceeds to determine the amount of the gain or loss on disposal. You can prove this using figures from Golden Enterprise's financial reports. iv. . 2. During fiscal 2013, Golden Enterprises issued $38,361,200 of new debt and spent $38,287,529 to repay debt. These activities affected the "Current portion of long-term debt," "Line of credit outstanding," and "Note payable-bank accounts. Combine those accounts to perform your analysis. The "Checks outstanding in excess of bank balances" account is also considered a financing account 3. To simplify your analysis, also combine the following balance sheet accounts: Accrued income taxes asset and liability accounts into a single, net liability account Deferred income tax asset and liability accounts into a single, net total liability account Current and long-term salary continuation accounts into a single total liability account 4. As in the 2012 statement of cash flows, both other assets" accounts should be treated as operating Recall that transactions with owners of the firm (for example, share issuances, dividends and share repurchases) are reported in the statement of changes in stockholders' equity. . assets, GOLDEN ENTERPRISES, INC. AND SUBSIDIARY CONSOLIDATED BALANCE SHEETS As of May 31, 2013 and June 1, 2012 ASSETS CURRENT ASSETS 757411 Cash and cash equivalents Receivables Trade accounts Other 5 10.3.3 10.55321 166485 10.529,706 Less Allowance for doubtful accounts 19.663 70.000 10,566.07 10,459,706 Raw materials Finished goods 1.72.341 3,053.272 1.1939 4,955,313 5.156,798 1.354,737 1,754.74 Prepaid expenses Accrued income taxes Deferred income taxes Total current assets 596,267 615,19 20,046,67 18323,634 PROPERTY, PLANT AND EQUIPMENT Land Buildings Machinery and equipment Transportation equipment 2,769.499 18,793,928 64,749.661 6.209.255 93,022,443 65.927.389 2,769,499 18,323, 373 61,247.920 6,944,931 89,285,723 62 TR8,133 Less: Accumulated depreciation 27,095,054 26,497.390 OTHER ASSETS Cash surrender value of life insurance Other 695,761 1.642.000 758.667 1.450,732 2,337,791 2,209,399 Total other assets TOTAL 47,756,479 5 48,753,636 LEARITIES AND STOCKHOLDERS LOCITY 1443315 1 CURRENT LLUITES Choice bu halen 1,7252 53.475 Liselotting Atomele 196649 Salaryotic plan 14.047261 Tallait LONG-TERM LIABILITIES Noteplehunk current Salaryotion plan Deferred income taxes 5.314213 1,032.810 3.304451 9,651,474 Total long-term liabilities STOCKHOLDERS EQUITY Como tock-5.66 2/3 par value: Authorized 35.000.000 dares, ud 13.808,793 shares Additional paid-in capital Retained camins Treasury shresat cost (2,096,161 shares in 2013,2,094,161 shares in 2012) 920. 9.219.195 6,497,954 19.273,214 (10.932.619 19.99 (10305 Total stockholders' equity 24,057,744 2439 TOTAL 47,756,479 48,753,636 GOLDEN ENTERPRISES, INC. AND SUBSIDIARY For the Fiscal Years Ended May 31, 2013 and June 1, 2012 2013 5 137.344.716 10,2427 66,67289 5 54233593 weral and administrative expenses 2.323.76 per income 61,040 (11.098) 102,917 kerepenses) income: o sale of assets expense 1625 113,73 Coler came (147,141) (6.035) 2.176,555 3.945,849 Toal other (expenses) income Income before income taxes Provision for income taxes 1,042.518 1,738,226 s 1,134,037 $ 2,207.623 Net income PER SHARE OF COMMON STOCK Basic earnings Dilated earnings S $ 0.10 0.10 5 S 0.19 0.19 GOLDEN ENTERPRISES, INC. AND SUBSIDIARY CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS' EQUITY For the Fiscal Years Ended May 31, 2013 and June 1, 2012 Equity Stock Capital Retained Earnings [Treasury] Shares Balance - June 3, 2011 s 23,657,654 9,219,195 5 (10,925,759) 6,497,954 5 $ 18,866,264 Net Income - 2012 Cash dividends paid 2,207,623 (1.466,831) 2,207,623 (1.466,831) Balance - June 1, 2012 9.219,195 24,398.446 (10,925,759) 6,497.954 19,607,056 Net income - 2013 Cash dividends paid Treasury shares purchased 1,134,037 (1,467,879) 1,134,037 (1,467,879) (6,860) (6.860) Balance - May 31, 2013 s 9,219,193 S 6,497,954 S 24.057,744 19,273,214 S (10.932.619) S GOLDEN ENTERPRISES, INC. AND SUBSIDIARY CONSOLIDATED STATEMENTS OF CASHFLOWS For the Fiscal Years Ended May 31, 2013 and June 1, 2012 0,214.40 Net cash provided by operating activities (details on following page) FLOWS FROM INVESTING ACTIVITIES 5 Puhase of property, plant and equipment eds from sale of property, plant and equipment 21 Net cash used in investing activities 3 FLOWS FROM FINANCING ACTIVITIES 16 Doht proceeds Debt repayments Change in checks outstanding in excess of bank balances Purchases of treasury shares Cash dividends paid Net cash (used in) provided by financing activities 36,619,711 (37,461,412) 712,031 (1.466, 31) (1.583,459 (827.822) 2,721,638 KET DECREASE IN CASH AND CASH EQUIVALENTS CASH AND CASH EQUIVALENTS AT BEGINNING OF YEAR CASH AND CASH EQUIVALENTS AT 1.893,816 END OF YEAR GOLDEN ENTERPRISES, INC. AND SUBSIDIARY For the Fiscal Years Ended May 31, 2013 and June 1, 2012 RECONCILIATION OF NET INCOME TO NET CASH PROVIDED BY OPERATING NCT S 2.207.623 Net income Adjustment to reconcile net income to net cash provided by operating activities Depreciation Deferred income taxes Gain on sale of property and equipment Change in receivables.net Change in inventories Change in prepaid expenses Change in cash surrender value of insurance Change in other assets - other Change in accounts payable Change in accrued expenses Change in salary continuation plan Change in accrued income taxes 3,303,353 557,576 (162,876) (345,853) (161,169) 48,956 176,177 (151,239) (297,983) Net cash provided by operating activities (132,524) (100,324) 805,573 5,747,290