Answered step by step

Verified Expert Solution

Question

1 Approved Answer

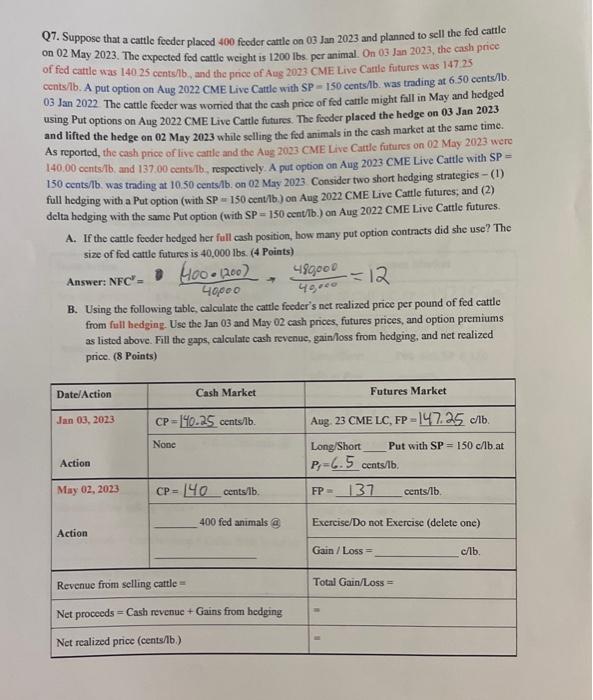

PLEASE HELP! Q7. Suppose that a cattle feeder placed 400 feeder cattle on 03 Jan 2023 and planned to sell the fed eartle on 02

PLEASE HELP!

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Governing The Modern Corporation Capital Markets Corporate Control And Economic Performance

Authors: Roy C. Smith, Ingo Walter

1st Edition

0195171675,0199924015