Answered step by step

Verified Expert Solution

Question

1 Approved Answer

please help solve question 2. it's urgent please the question is there. question 2 Vent In Mercy Lid wt the cost of the wine cas

please help solve question 2. it's urgent

please the question is there. question 2

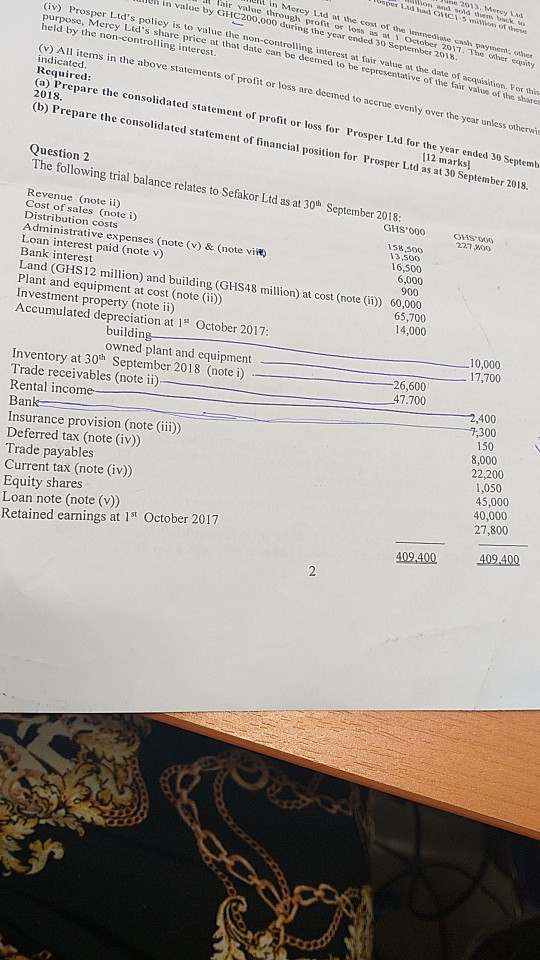

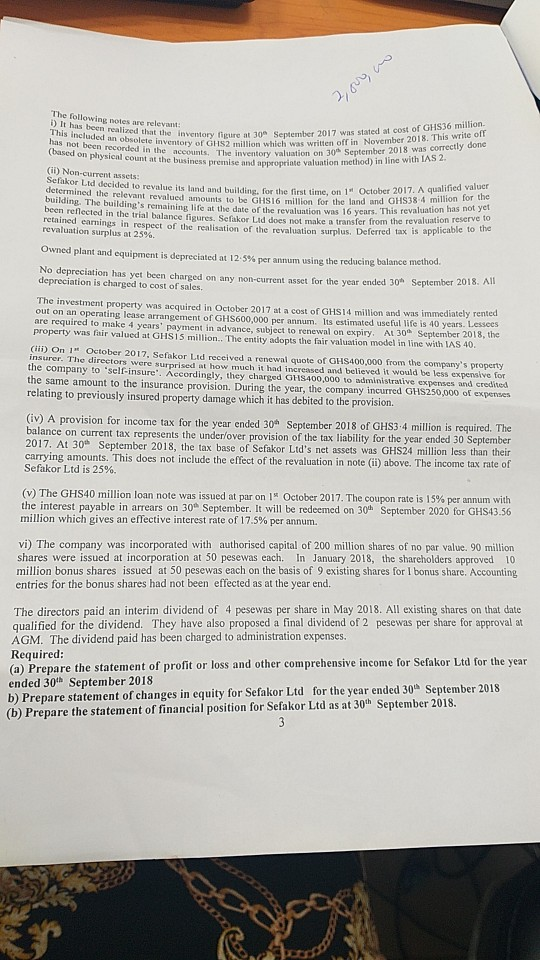

Vent In Mercy Lid wt the cost of the wine cas altair value through profit or loss us October 2017. The Un in value by GHC200,000 during the year ended 30 September 2018 TIPY per la A (iv) Prosper Lid's policy is to value the non-controlling interest at fair value of the date of acquisition of this purpose, Mercy Ltd's share prices that date can be deemed to be representative of the fair value of the show held by the non-controlling interest. 2013. Mere Them OAC millions of these (v) All items in the above statements of profit or loss are deemed to accrue evenly over the year unless otherwis indicated. Required: e ver equity 2018. (a) Prepare the consolidated statement of profit or loss for Prosper Lid for the year ended 30 Septemb 112 marks] (b) Prepare the consolidated statement of financial position for Prosper Ltd as at 30 September 2018 Question 2 The following trial balance relates to Sefakor Ltd as at 30 September 2018: GHS'000 ONS 000 22. 700 Revenue (note ii) Cost of sales (note i) Distribution costs 158,500 Administrative expenses (note (V) & (note vi 13,500 Loan interest paid (note v) 16,500 Bank interest 6,000 Land (GHS12 million) and building (GHS48 million) at cost (note (ii) 60,000 900 Plant and equipment at cost (note (11) Investment property (note ii) 65,700 Accumulated depreciation at 1" October 2017: 14,000 building owned plant and equipment Inventory at 30th September 2018 (notei) -26,600 Trade receivables (note ii) - 47.700 Rental income Bank Insurance provision (note (iii)) Deferred tax (note (iv)) Trade payables Current tax (note (iv) Equity shares Loan note (note (v)) Retained earnings at 1st October 2017 10,000 17,700 2,400 7,300 150 8,000 22,200 1,050 45,000 40,000 27,800 409,400 409,400 2,oro, no The following notes are relevant has been realized that the inventory figure at J DCH included an obsolete inventory or GHS2 million which was written off in Noven is not been recorded in the accounts. The inventory valuation on 30 Sep Coased on physical count at the business remise and appropriate valuation method) in (ii) Non-current assets: Sefakor Ltd decided to revalue its land and buildine for the first time, on 1" October 2011 determined the relevant revalued amounts to be GHS16 million for the land and GHS The evaluation has not yet ding. The building's remaining life at the date of the revaluation was 16 years. This revaluation make a transfer from the revaluation reserve the con rellected in the trial balance fisures. Selskar Luddes evaluation reserve to retnined earnings in respect of the realisation of the evaluation surplus. Deferred tax is applicate revaluation surplus at 25% gure at 30 September 2017 was stated at cost of GHS36 million was written of in November 2018. This write off luation on 30 September 2018 was correctly done emise and appropriate valuation method) in line with IAS 2 hirst time, on 1" October 2017. A qualified valuer $10 million for the land and OHS38-4 million for the Owned plant and equipment is depreciated at 12.5% per annum using the reducing balance method No depreciation has yet been charged on any non-current asset for the year ended 30 depreciation is charged to cost of sales. September 2016. A The investment property was acquired in October 2017 at a cost of GHS14 million and was immediately rented out on an operating lease arrangement of GHS600,000 per annum. Its estimated useful life is 40 years. Lessces are required to make 4 years' payment in advance subiect to renewal on expiry AL 30 September 2018, the property was fair valued at GHSIS million.. The entity adopts the fair valuation model in line with LAS 40. CH) On 1 October 2017. Sefakor Lid received a renewal quote of GHS400.000 from the company's property insurer. The directors were surprised at how much it had increased and believed it would be less expensive for the company to 'self-insure'. Accordingly, they charged GHS400,000 to administrative expenses and credited the same amount to the insurance provision. During the year, the company incurred GHS250,000 of expenses relating to previously insured property damage which it has debited to the provision. (iv) A provision for income tax for the year ended 30 September 2018 of GHS3-4 million is required. The balance on current tax represents the under/over provision of the tax liability for the year ended 30 September 2017. At 30 September 2018, the tax base of Sefakor Lid's net assets was GHS24 million less than their carrying amounts. This does not include the effect of the revaluation in note (il) above. The income tax rate of Sefakor Ltd is 25%. (v) The GHS40 million loan note was issued at par on 1 October 2017. The coupon rate is 15% per annum with the interest payable in arrears on 30 September. It will be redeemed on 304 September 2020 for GHS43.56 million which gives an effective interest rate of 17.5% per annum. vi) The company was incorporated with authorised capital of 200 million shares of no par value. 90 million shares were issued at incorporation at 50 pesewas each. In January 2018, the shareholders approved 10 million bonus shares issued at 50 pesewas each on the basis of 9 existing shares for I bonus share. Accounting entries for the bonus shares had not been effected as at the year end. The directors paid an interim dividend of 4 pesewas per share in May 2018. All existing shares on that date qualified for the dividend. They have also proposed a final dividend of 2 pesewas per share for approval at AGM. The dividend paid has been charged to administration expenses. Required: (a) Prepare the statement of profit or loss and other comprehensive income for Sefakor Ltd for the year ended 30th September 2018 b) Prepare statement of changes in equity for Sefakor Ltd for the year ended 30 September 2018 (b) Prepare the statement of financial position for Sefakor Ltd as at 30th September 2018Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Corporate Risk Management

Authors: Faisal F. Al-Thani, Tony Merna

2nd Edition

0470518332, 978-0470518335