Answered step by step

Verified Expert Solution

Question

1 Approved Answer

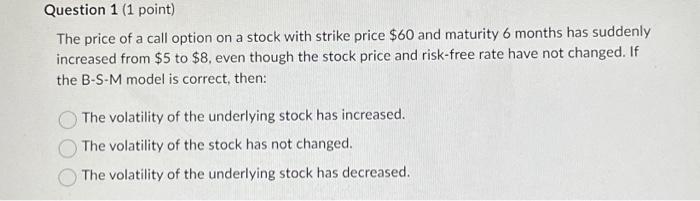

please help The price of a call option on a stock with strike price $60 and maturity 6 months has suddenly increased from $5 to

please help

The price of a call option on a stock with strike price $60 and maturity 6 months has suddenly increased from $5 to $8, even though the stock price and risk-free rate have not changed. If the B-S-M model is correct, then: The volatility of the underlying stock has increased. The volatility of the stock has not changed. The volatility of the underlying stock has decreased Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance And Economics Discussion Series Monetary Policy And The Housing Bubble

Authors: United States Federal Reserve Board, Jane Dokko

1st Edition

1288704682, 9781288704682