Answered step by step

Verified Expert Solution

Question

1 Approved Answer

please I need help.thank you Ch 03: End-of-Chapter Problems - Risk and Return: Part II eBook Characteristic Line You are given the following set of

please I need help.thank you

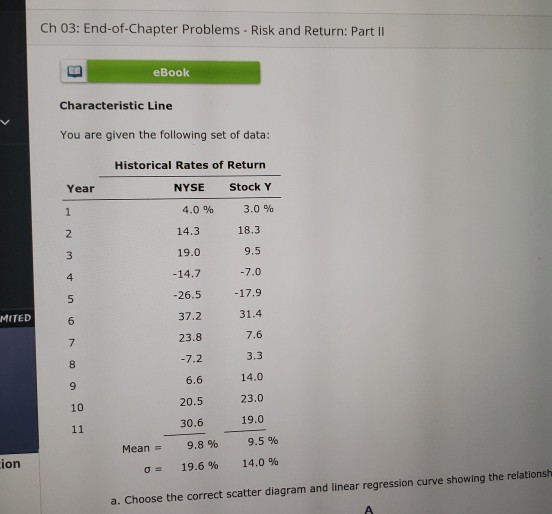

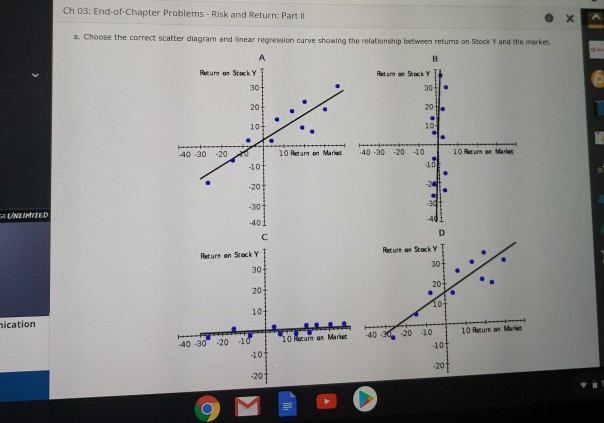

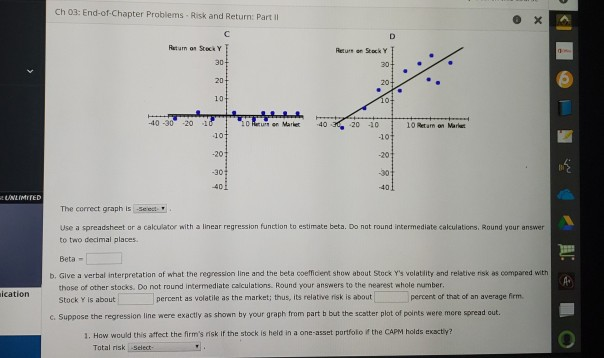

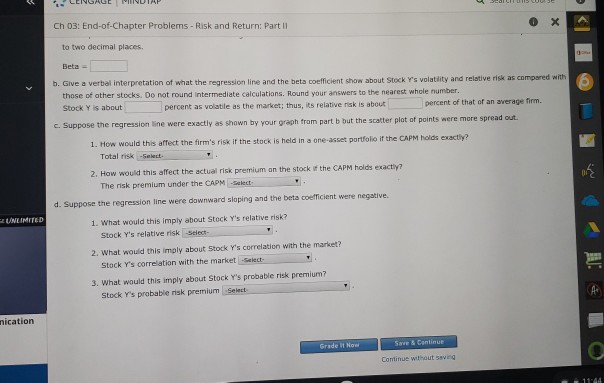

Ch 03: End-of-Chapter Problems - Risk and Return: Part II eBook Characteristic Line You are given the following set of data: Historical Rates of Return Year NYSE Stock Y 3.0 % 1 4.0 % 14.3 18.3 19.0 9.5 3 -7.0 -14.7 4 -17.9 -26.5 MITED 31.4 37.2 6 7.6 23.8 7 3.3 -7.2 8 14.0 6.6 23.0 20.5 10 19.0 30.6 11 9.5 % 9.8 % Mean ion 14.0 % 19.6 % a. Choose the correct scatter diagram and linear regression curve showing the relationsh st Ch 03: End-of-Chapter Problems- Risk and Return: Part Il a. Choose the correct scatter diagram and linear reqression curve showing the relationship between returns on Stock Y and the market. A Return on Stock Y3 Ratan an Stock Y 30- 30 20 20 10t 10- 40-30 20 10 Retarn on Markat 40-30 -20 -10 10 Ret un on Market 101 10 -20 -30 UNLIMITED 40 D C Ret ure on Scock Y Ret urn on Steck Y 30t 30- 20+ 20 104 10- ication 10 Return on Marlet -20 10 40 10 Return on Market -20 10 40 -30 101 -10 201 20 Ch 03: End-of-Chapter Problems - Risk and Return: Part I C D Rturn on Stock Y Return gn Stock Y 30t 30 20t 20- 10- 10- -40-30 -10 -20 10 Rur on Market 40 -30 20 -10 10 Retarn on Marl 101 -101 201 20 -30 -301 40i 40 UNLIMITED The correct graph is Seeat Use a spreadsheet or a calculator with a linear regression function to estimate beta. Do not round intermediate calculations, Round vour answer to two decimal places Beta- b. Glve a verbal interpretation of what the regression line and the beta coefficient show about Stock Y's volatility and relative risk as compared with those of other stocks. Do not round internmediate calculations. Round your answers to the nearest whole number. ication percent of that of an average firm percent as volatile as the market; thus, its relative risk is about Stock Y is about c. Suppose the regression Iline were exactly as shown by your graph from part b but the scatter plot of points were more spread out. 1. How would this affect the firm's risk if the stock is held in a one-asset portfolo if the CAPM holds exactly? Total risk-Select- Ch 03: End-of-Chapter Problems- Risk and Return: Part II to two decimal places. Beta b. Give a verbal interpretation of what the regression line and the beta coefficient show about Stock Y's volatility and relative risk as compared with those of ather stocks, Do not round Intermediate calculations, Round your answers to the nearest whole number Stock Y is about percent as volatile as the market; thus, its relative risk is about percent of that of an average firm. c. Suppose the regression line were exactly as shown by your graph from part b but the scatter plot of points were more spread out 1. How would this affect the firm's risk if the stock is held in a one-asset portfolio if the CAPM holds exactly? Total risk -select 2. How would this affect the actual risk premium an the stock if the CAPM holds exactly? The risk premium under the CAPMSelect- d. Suppose the regression line were dawnward sloping and the beta coefficient were negative. UNLIMITED 1. What would this imply about Stock Y's relative risk? Stock Y's relative risk -seiect 2. What would this imply about Stock Y's correlation with the market? Stock Y's correlation with the market -select- 3. What would this imply about Stock Y's probable risk premium? Stock Y's probable risk premium Select- nication Save&Centinue Grade it Now Continue without seving 1144Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Software Reviews And Audits A How To Guide For Project Staff

Authors: Dr David Tuffley

1st Edition

1461130468, 978-1461130468