please illustrate using the triangle diagram & tell how Credir Agricole could avoid the situation

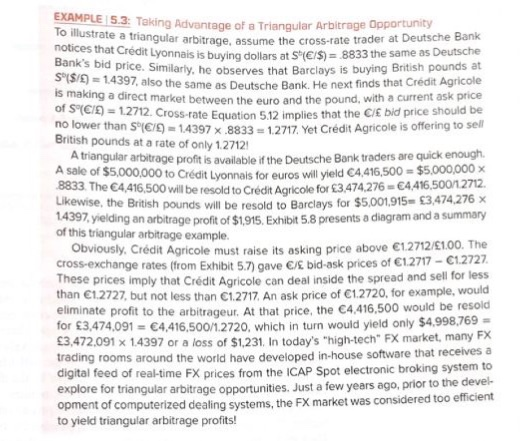

EXAMPLE 5.3: Taking Advantage of a Triangular Arbitrage Opport To illustrate a tria 1 mustrate a triangular arbitrage, assume the cross-rate trader at Deutsche Bank notices that Credit Lyonnais is buying dollars at mais is buying dollars at S(ES) = 8833 the same as Deutsche banks bid price. Similarly h a rves that Barclays is buying British pounds S5/2 = 1.4397, also the same as Deutsche Bank. He next finds that Crdit Agricole is making a direct market between the euro and ct market between the euro and the pound, with a current ask price of S"(C/A) = 12712. Cross-rate Equation 5.12 implies 2. Cross-rate Equation 5.12 implies that the C/E bid price should be no lower than Sf/)=14397.883312717 Yet Credit Agricole is offering to see British pounds at a rate of only 1.27121 A triangular arbitrage profit is available if the Deutsche Bank traders are quick enough A sale of $5,000,000 to Crdit Lyonnais for euros will yield 4,416,500 $5,000,000 x 5833 The 4,416,500 will be resold to Credit Agricole for 3.474,276 4.416,500/12712 Likewise, the British pounds will be resold to Barclays for $5.001,915 83,474,276 X 14397 yielding an arbitrage profit of $1.915. Exhibit 5,8 presents a diagram and a summary of this triangular arbitrage example, Obviously, Crdit Agricole must raise its asking price above 1.2712/1.00. The cross-exchange rates from Exhibit 5.7) cave / bid-ask prices of 12717-C1.2727 These prices imply that Crdit Agricole can deal inside the spread and sell for less than 1.2727, but not less than 1.2717 An ask price of C12720, for example, would eliminate profit to the arbitrageur. At that price, the 4.416,500 would be resold for 3,474,091 = 4,416,500/12720, which in turn would yield only $4.998,769 = $3,472,091 x 1.4397 or a loss of $1.231. In today's "high-tech" FX market, many FX trading rooms around the world have developed in-house software that receives a digital feed of real-time FX prices from the ICAP Spot electronic broking system to explore for triangular arbitrage opportunities. Just a few years ago, prior to the devel- opment of computerized dealing systems, the FX market was considered too efficient to yield triangular arbitrage profits! EXAMPLE 5.3: Taking Advantage of a Triangular Arbitrage Opport To illustrate a tria 1 mustrate a triangular arbitrage, assume the cross-rate trader at Deutsche Bank notices that Credit Lyonnais is buying dollars at mais is buying dollars at S(ES) = 8833 the same as Deutsche banks bid price. Similarly h a rves that Barclays is buying British pounds S5/2 = 1.4397, also the same as Deutsche Bank. He next finds that Crdit Agricole is making a direct market between the euro and ct market between the euro and the pound, with a current ask price of S"(C/A) = 12712. Cross-rate Equation 5.12 implies 2. Cross-rate Equation 5.12 implies that the C/E bid price should be no lower than Sf/)=14397.883312717 Yet Credit Agricole is offering to see British pounds at a rate of only 1.27121 A triangular arbitrage profit is available if the Deutsche Bank traders are quick enough A sale of $5,000,000 to Crdit Lyonnais for euros will yield 4,416,500 $5,000,000 x 5833 The 4,416,500 will be resold to Credit Agricole for 3.474,276 4.416,500/12712 Likewise, the British pounds will be resold to Barclays for $5.001,915 83,474,276 X 14397 yielding an arbitrage profit of $1.915. Exhibit 5,8 presents a diagram and a summary of this triangular arbitrage example, Obviously, Crdit Agricole must raise its asking price above 1.2712/1.00. The cross-exchange rates from Exhibit 5.7) cave / bid-ask prices of 12717-C1.2727 These prices imply that Crdit Agricole can deal inside the spread and sell for less than 1.2727, but not less than 1.2717 An ask price of C12720, for example, would eliminate profit to the arbitrageur. At that price, the 4.416,500 would be resold for 3,474,091 = 4,416,500/12720, which in turn would yield only $4.998,769 = $3,472,091 x 1.4397 or a loss of $1.231. In today's "high-tech" FX market, many FX trading rooms around the world have developed in-house software that receives a digital feed of real-time FX prices from the ICAP Spot electronic broking system to explore for triangular arbitrage opportunities. Just a few years ago, prior to the devel- opment of computerized dealing systems, the FX market was considered too efficient to yield triangular arbitrage profits