Please kindly read the case study, use the notes I have provided and external resources as well,

ANSWER ONLY QUESTION 2

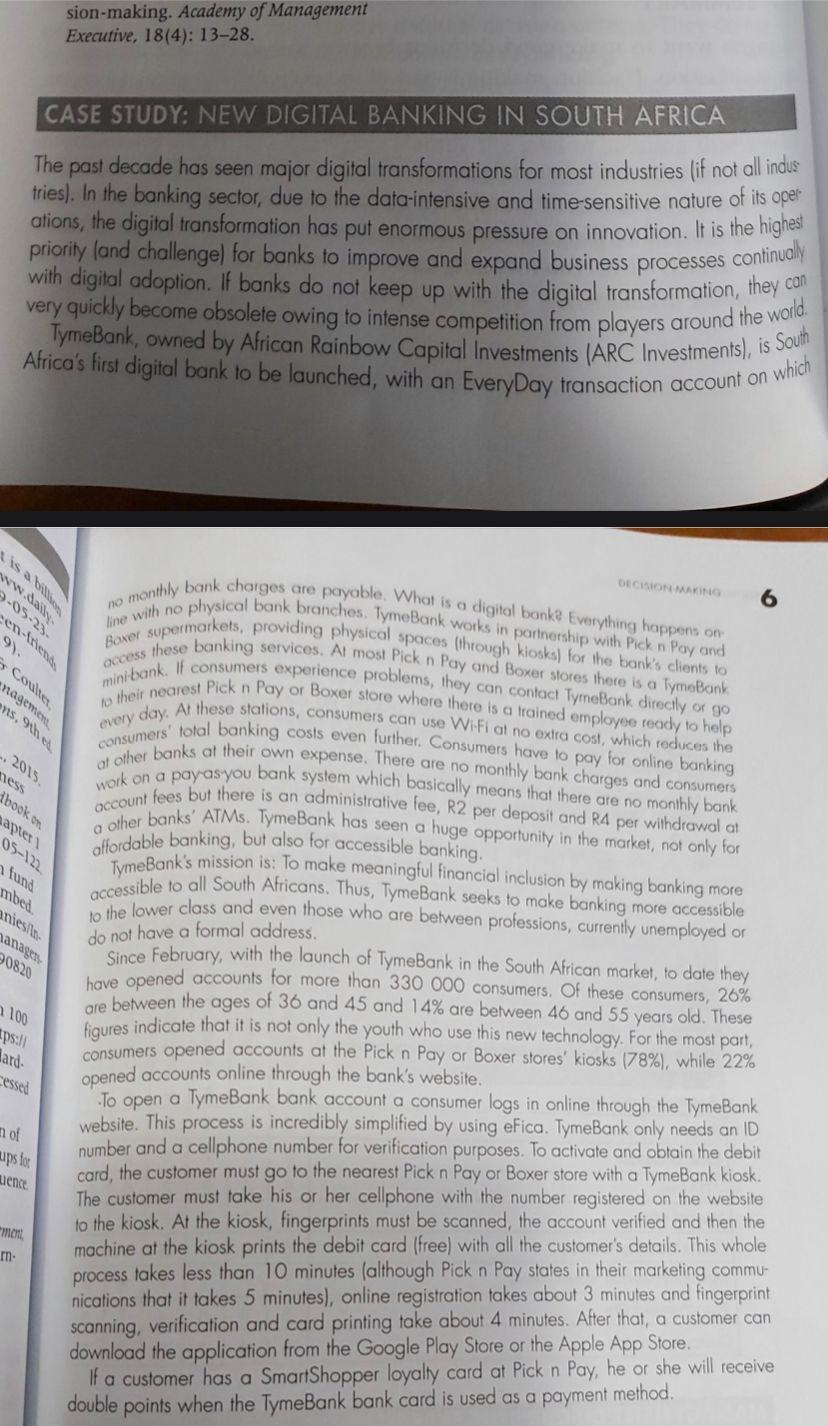

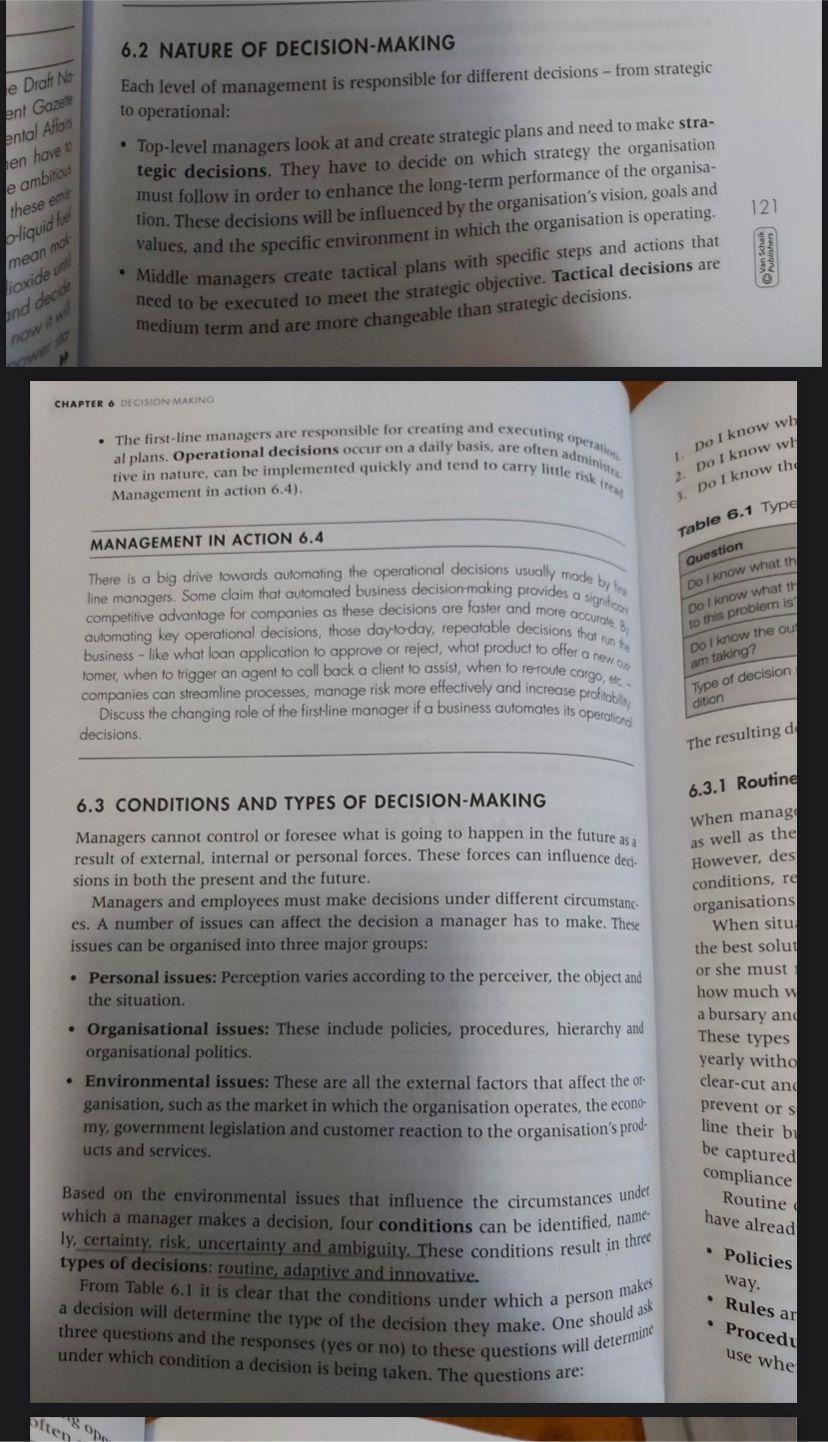

sion-making. Academy of Management Executive, 18(4): 13-28. CASE STUDY: NEW DIGITAL BANKING IN SOUTH AFRICA The past decade has seen major digital transformations for most industries (if not all indus tries). In the banking sector, due to the data-intensive and time-sensitive nature of its oper ations, the digital transformation has put enormous pressure on innovation. It is the highest priority (and challenge) for banks to improve and expand business processes continually with digital adoption. If banks do not keep up with the digital transformation, they can very quickly become obsolete owing to intense competition from players around the world. Africa's first digital bank to be launched, with an EveryDay transaction account on which TymeBank, owned by African Rainbow Capital Investments (ARC Investments), is South DECISION MAKING no monthly bank charges are payable. What is a digital bank? Everything happens on line with no physical bank branches. TymeBank works in partnership with Pick n Pay and Boxer supermarkets, providing physical spaces (through kiosks) for the bank's clients to mini-bank. If consumers experience problems, they can contact TymeBank directly or go access these banking services. At most Pick n Pay and Boxer stores there is a TymeBank to their nearest Pick n Pay or Boxer store where there is a trained employee ready to help every day. At these stations, consumers can use Wi-Fi at no extra cost, which reduces the consumers' total banking costs even further. Consumers have to pay for online banking at other banks at their own expense. There are no monthly bank charges and consumers work on a pay-as-you bank system which basically means that there are no monthly bank account fees but there is an administrative fee, R2 per deposit and R4 per withdrawal at a other banks' ATMs. TymeBank has seen a huge opportunity in the market, not only for affordable banking, but also for accessible banking. TymeBank's mission is: To make meaningful financial inclusion by making banking more accessible to all South Africans. Thus, TymeBank seeks to make banking more accessible to the lower class and even those who are between professions, currently unemployed or do not have a formal address. Since February, with the launch of TymeBank in the South African market, to date they have opened accounts for more than 330 000 consumers. Of these consumers, 26% are between the ages of 36 and 45 and 14% are between 46 and 55 years old. These figures indicate that it is not only the youth who use this new technology. For the most part, consumers opened accounts at the Pick n Pay or Boxer stores' kiosks (78%), while 22% opened accounts online through the bank's website. To open a TymeBank bank account a consumer logs in online through the TymeBank website. This process is incredibly simplified by using efica. TymeBank only needs an ID number and a cellphone number for verification purposes. To activate and obtain the debit card, the customer must go to the nearest Pick n Pay or Boxer store with a TymeBank kiosk. The customer must take his or her cellphone with the number registered on the website to the kiosk. At the kiosk, fingerprints must be scanned, the account verified and then the machine at the kiosk prints the debit card (free) with all the customer's details. This whole process takes less than 10 minutes (although Pick n Pay states in their marketing commu- nications that it takes 5 minutes), online registration takes about 3 minutes and fingerprint scanning, verification and card printing take about 4 minutes. After that, a customer can download the application from the Google Play Store or the Apple App Store. If a customer has a SmartShopper loyalty card at Pick n Pay, he or she will receive double points when the TymeBank bank card is used as a payment method. is a billion www.daily 9-05-23. en-friends Coulter, nagemen ns. 9th ed 2015. ness book on apter 1 05-122 n fund mbed. anies/In managers 90820 100 ps:// ard- cessed of ups for ence ment m- 6.2 NATURE OF DECISION-MAKING Each level of management is responsible for different decisions - from strategic to operational: 121 Top-level managers look at and create strategic plans and need to make stra- tegic decisions. They have to decide on which strategy the organisation must follow in order to enhance the long-term performance of the organisa- tion. These decisions will be influenced by the organisation's vision, goals and values, and the specific environment in which the organisation is operating. Middle managers create tactical plans with specific steps and actions that need to be executed to meet the strategic objective. Tactical decisions are medium term and are more changeable than strategic decisions. CHAPTER 6 DECISION-MAKING . The first-line managers are responsible for creating and executing operation tive in nature, can be implemented quickly and tend to carry little risk (read al plans. Operational decisions occur on a daily basis, are often administra Management in action 6.4). Do I know wh 2. Do I know wh Do I know the 3. MANAGEMENT IN ACTION 6.4 Table 6.1 Type Question There is a big drive towards automating the operational decisions usually made by fes line managers. Some claim that automated business decision-making provides a significan automating key operational decisions, those day-to-day, repeatable decisions that run th competitive advantage for companies as these decisions are faster and more accurate. By business-like what loan application to approve or reject, what product to offer a new tomer, when to trigger an agent to call back a client to assist, when to re-route cargo, etc. companies can streamline processes, manage risk more effectively and increase profitabil Discuss the changing role of the first-line manager if a business automates its operational Do I know what th Do I know what th to this problem is? Do I know the ou am taking? Type of decision dition decisions. The resulting d 6.3 CONDITIONS AND TYPES OF DECISION-MAKING Managers cannot control or foresee what is going to happen in the future as a result of external, internal or personal forces. These forces can influence deci. sions in both the present and the future. Managers and employees must make decisions under different circumstanc es. A number of issues can affect the decision a manager has to make. These issues can be organised into three major groups: Personal issues: Perception varies according to the perceiver, the object and the situation. Organisational issues: These include policies, procedures, hierarchy and organisational politics. Environmental issues: These are all the external factors that affect the or ganisation, such as the market in which the organisation operates, the econo- my, government legislation and customer reaction to the organisation's prod- ucts and services. Based on the environmental issues that influence the circumstances under which a manager makes a decision, four conditions can be identified, name ly, certainty, risk, uncertainty and ambiguity. These conditions result in three types of decisions: routine, adaptive and innovative. From Table 6.1 it is clear that the conditions under which a person makes a decision will determine the type of the decision they make. One should ask three questions and the responses (yes or no) to these questions will determine under which condition a decision is being taken. The questions are: often e Draft No ent Gazete ental Affairs en have to e ambitious these ema o-liquid hel mean mak ioxide until and decide now it d Van Schaik Publishers 6.3.1 Routine When manage as well as the However, des conditions, re organisations When situ the best solut or she must how much w a bursary and These types yearly witho clear-cut and prevent or s line their bu be captured compliance Routine have alread Policies way. Rules ar Procedu use whe A. QUESTIONS (CASE STUDY: Chapter 6 Page 138-140 of the prescribed book) 1.To start Tyme bank, what type of decision did African Rainbow Capital Investments (ARC Investments) make and under what condition is this decision typically made? Motivate your answer. 2. Apply the steps of rational decision-making to the decision of the CEO Tauriq Keraan to launch an account for small businesses, responsibly offering consumers unsecured credit. 3. Apply the steps of rational decision-making to the decision of a consumer at Absa who is unhappy with the fees to switch to Tyme Bank. 4. During step three of the decision-making process the consumer decides to use the weighted average model. Based on the information below, which bank will be the best for the consumer? 1 sion-making. Academy of Management Executive, 18(4): 13-28. CASE STUDY: NEW DIGITAL BANKING IN SOUTH AFRICA The past decade has seen major digital transformations for most industries (if not all indus tries). In the banking sector, due to the data-intensive and time-sensitive nature of its oper ations, the digital transformation has put enormous pressure on innovation. It is the highest priority (and challenge) for banks to improve and expand business processes continually with digital adoption. If banks do not keep up with the digital transformation, they can very quickly become obsolete owing to intense competition from players around the world. Africa's first digital bank to be launched, with an EveryDay transaction account on which TymeBank, owned by African Rainbow Capital Investments (ARC Investments), is South DECISION MAKING no monthly bank charges are payable. What is a digital bank? Everything happens on line with no physical bank branches. TymeBank works in partnership with Pick n Pay and Boxer supermarkets, providing physical spaces (through kiosks) for the bank's clients to mini-bank. If consumers experience problems, they can contact TymeBank directly or go access these banking services. At most Pick n Pay and Boxer stores there is a TymeBank to their nearest Pick n Pay or Boxer store where there is a trained employee ready to help every day. At these stations, consumers can use Wi-Fi at no extra cost, which reduces the consumers' total banking costs even further. Consumers have to pay for online banking at other banks at their own expense. There are no monthly bank charges and consumers work on a pay-as-you bank system which basically means that there are no monthly bank account fees but there is an administrative fee, R2 per deposit and R4 per withdrawal at a other banks' ATMs. TymeBank has seen a huge opportunity in the market, not only for affordable banking, but also for accessible banking. TymeBank's mission is: To make meaningful financial inclusion by making banking more accessible to all South Africans. Thus, TymeBank seeks to make banking more accessible to the lower class and even those who are between professions, currently unemployed or do not have a formal address. Since February, with the launch of TymeBank in the South African market, to date they have opened accounts for more than 330 000 consumers. Of these consumers, 26% are between the ages of 36 and 45 and 14% are between 46 and 55 years old. These figures indicate that it is not only the youth who use this new technology. For the most part, consumers opened accounts at the Pick n Pay or Boxer stores' kiosks (78%), while 22% opened accounts online through the bank's website. To open a TymeBank bank account a consumer logs in online through the TymeBank website. This process is incredibly simplified by using efica. TymeBank only needs an ID number and a cellphone number for verification purposes. To activate and obtain the debit card, the customer must go to the nearest Pick n Pay or Boxer store with a TymeBank kiosk. The customer must take his or her cellphone with the number registered on the website to the kiosk. At the kiosk, fingerprints must be scanned, the account verified and then the machine at the kiosk prints the debit card (free) with all the customer's details. This whole process takes less than 10 minutes (although Pick n Pay states in their marketing commu- nications that it takes 5 minutes), online registration takes about 3 minutes and fingerprint scanning, verification and card printing take about 4 minutes. After that, a customer can download the application from the Google Play Store or the Apple App Store. If a customer has a SmartShopper loyalty card at Pick n Pay, he or she will receive double points when the TymeBank bank card is used as a payment method. is a billion www.daily 9-05-23. en-friends Coulter, nagemen ns. 9th ed 2015. ness book on apter 1 05-122 n fund mbed. anies/In managers 90820 100 ps:// ard- cessed of ups for ence ment m- 6.2 NATURE OF DECISION-MAKING Each level of management is responsible for different decisions - from strategic to operational: 121 Top-level managers look at and create strategic plans and need to make stra- tegic decisions. They have to decide on which strategy the organisation must follow in order to enhance the long-term performance of the organisa- tion. These decisions will be influenced by the organisation's vision, goals and values, and the specific environment in which the organisation is operating. Middle managers create tactical plans with specific steps and actions that need to be executed to meet the strategic objective. Tactical decisions are medium term and are more changeable than strategic decisions. CHAPTER 6 DECISION-MAKING . The first-line managers are responsible for creating and executing operation tive in nature, can be implemented quickly and tend to carry little risk (read al plans. Operational decisions occur on a daily basis, are often administra Management in action 6.4). Do I know wh 2. Do I know wh Do I know the 3. MANAGEMENT IN ACTION 6.4 Table 6.1 Type Question There is a big drive towards automating the operational decisions usually made by fes line managers. Some claim that automated business decision-making provides a significan automating key operational decisions, those day-to-day, repeatable decisions that run th competitive advantage for companies as these decisions are faster and more accurate. By business-like what loan application to approve or reject, what product to offer a new tomer, when to trigger an agent to call back a client to assist, when to re-route cargo, etc. companies can streamline processes, manage risk more effectively and increase profitabil Discuss the changing role of the first-line manager if a business automates its operational Do I know what th Do I know what th to this problem is? Do I know the ou am taking? Type of decision dition decisions. The resulting d 6.3 CONDITIONS AND TYPES OF DECISION-MAKING Managers cannot control or foresee what is going to happen in the future as a result of external, internal or personal forces. These forces can influence deci. sions in both the present and the future. Managers and employees must make decisions under different circumstanc es. A number of issues can affect the decision a manager has to make. These issues can be organised into three major groups: Personal issues: Perception varies according to the perceiver, the object and the situation. Organisational issues: These include policies, procedures, hierarchy and organisational politics. Environmental issues: These are all the external factors that affect the or ganisation, such as the market in which the organisation operates, the econo- my, government legislation and customer reaction to the organisation's prod- ucts and services. Based on the environmental issues that influence the circumstances under which a manager makes a decision, four conditions can be identified, name ly, certainty, risk, uncertainty and ambiguity. These conditions result in three types of decisions: routine, adaptive and innovative. From Table 6.1 it is clear that the conditions under which a person makes a decision will determine the type of the decision they make. One should ask three questions and the responses (yes or no) to these questions will determine under which condition a decision is being taken. The questions are: often e Draft No ent Gazete ental Affairs en have to e ambitious these ema o-liquid hel mean mak ioxide until and decide now it d Van Schaik Publishers 6.3.1 Routine When manage as well as the However, des conditions, re organisations When situ the best solut or she must how much w a bursary and These types yearly witho clear-cut and prevent or s line their bu be captured compliance Routine have alread Policies way. Rules ar Procedu use whe A. QUESTIONS (CASE STUDY: Chapter 6 Page 138-140 of the prescribed book) 1.To start Tyme bank, what type of decision did African Rainbow Capital Investments (ARC Investments) make and under what condition is this decision typically made? Motivate your answer. 2. Apply the steps of rational decision-making to the decision of the CEO Tauriq Keraan to launch an account for small businesses, responsibly offering consumers unsecured credit. 3. Apply the steps of rational decision-making to the decision of a consumer at Absa who is unhappy with the fees to switch to Tyme Bank. 4. During step three of the decision-making process the consumer decides to use the weighted average model. Based on the information below, which bank will be the best for the consumer? 1