Question

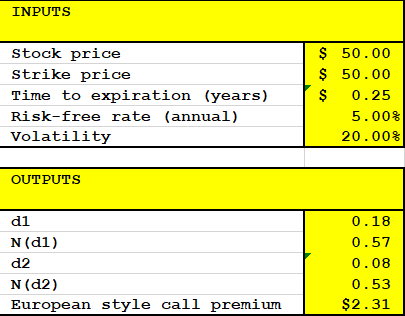

Please make a spreadsheet that implements a five-step binomial option pricing model (a five-step tree has six terminal nodes). The ASU Index is currently at

Please make a spreadsheet that implements a five-step binomial option pricing model (a five-step tree has six terminal nodes).

The ASU Index is currently at 650. At each time-step it can either rise of fall by 10 percent. The risk-free interest rate is five percent per year. Each time step is one month. Use your spreadsheet to calculate prices (premiums) for a European call, American call, European put, and American put, all with a strike price of 650 and a total time to expiration of five months.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Management For Decision Makers

Authors: Peter Atrill

7th Edition

129201606X, 978-1292016061