Answered step by step

Verified Expert Solution

Question

1 Approved Answer

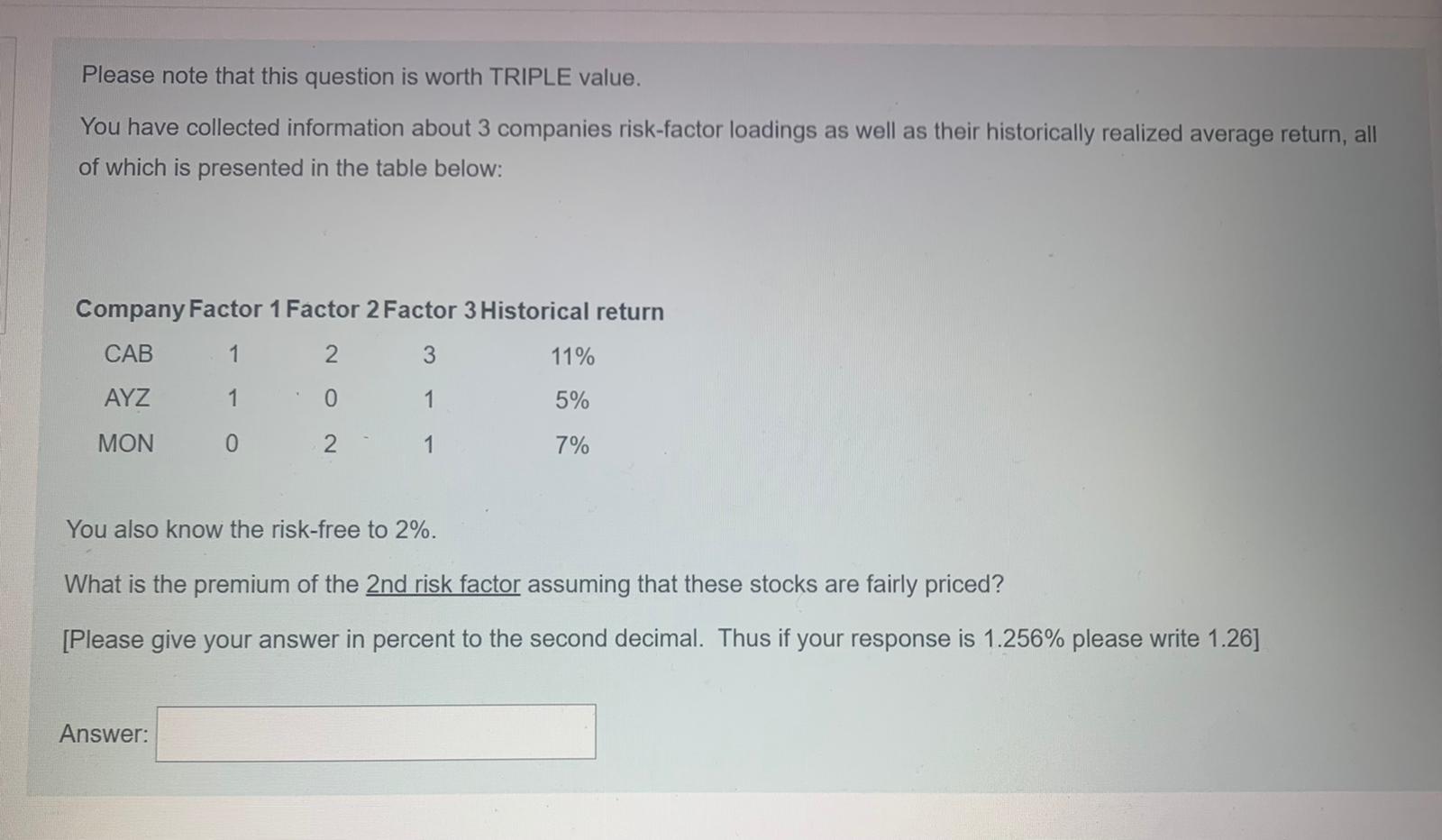

Please note that this question is worth TRIPLE value. You have collected information about 3 companies risk-factor loadings as well as their historically realized average

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Asset Allocation And International Investments

Authors: G. Gregoriou

1st Edition

023001917X,0230626513