Answered step by step

Verified Expert Solution

Question

1 Approved Answer

PLEASE NOTICE THAT THIS IS COST METHOD not entity method. Financial statements for P and S for the year ended December 31, 2016, were as

PLEASE NOTICE THAT THIS IS COST METHOD not entity method.

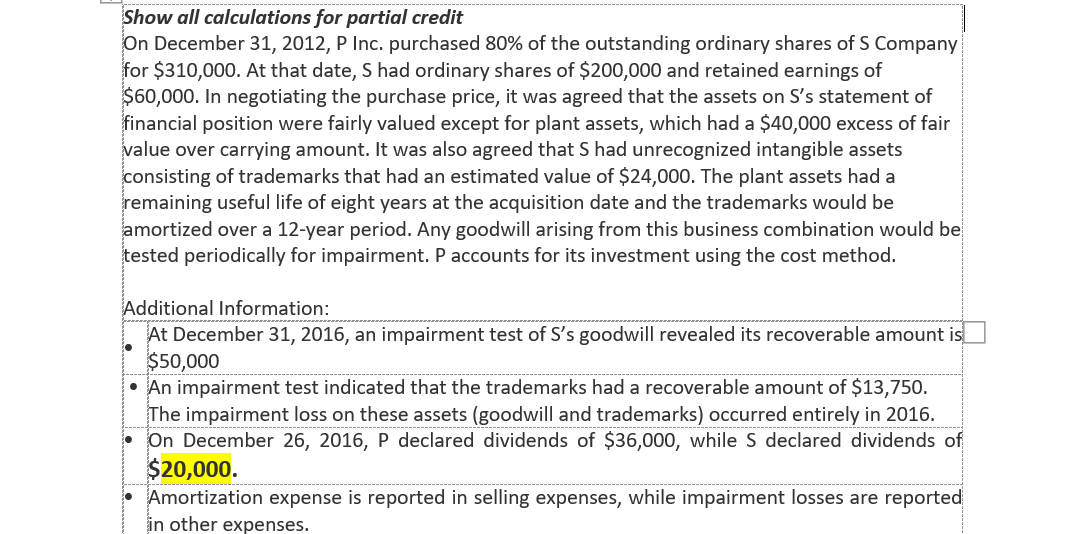

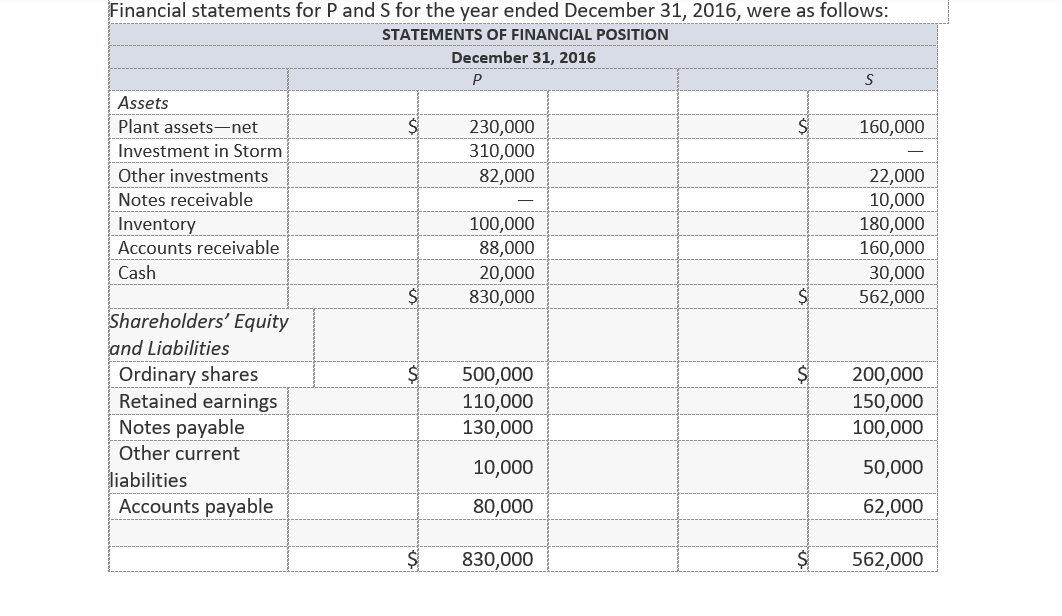

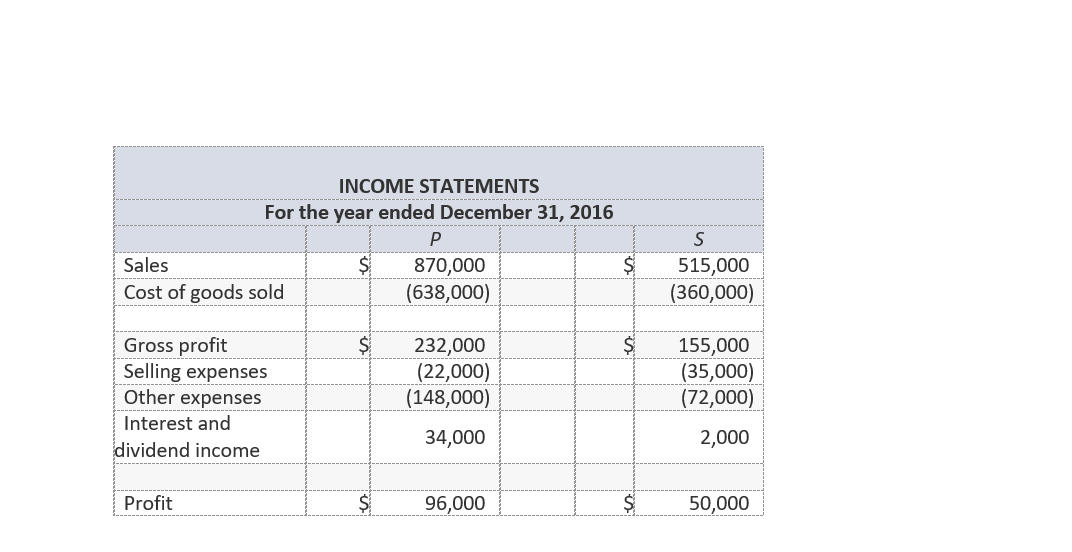

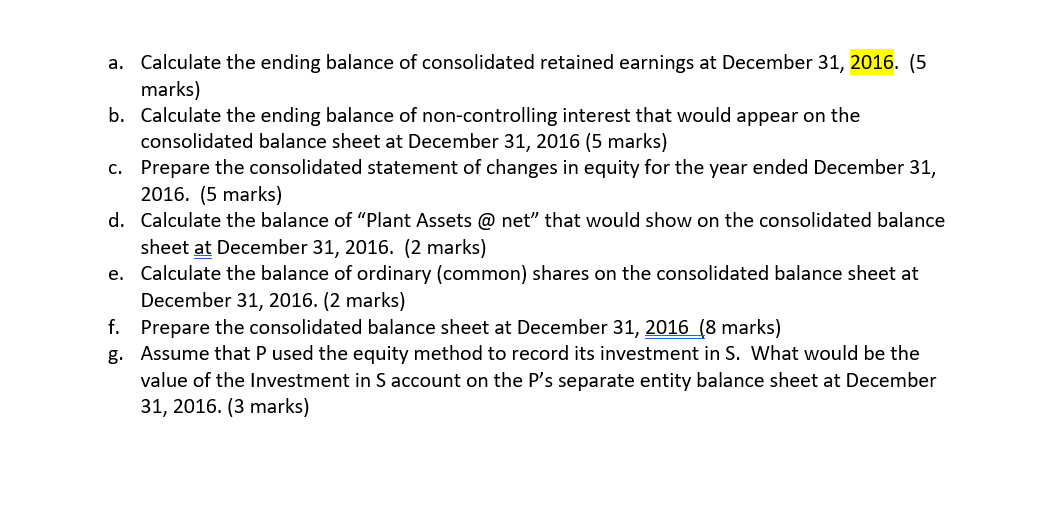

Financial statements for P and S for the year ended December 31, 2016, were as follows: STATEMENTS OF FINANCIAL POSITION December 31, 2016 INCOME STATEMENTS \begin{tabular}{|c|c|c|c|c|} \hline \multicolumn{5}{|c|}{ INCOME STATEMENTS } \\ \hline \multicolumn{5}{|c|}{ For the year ended December 31, 2016} \\ \hline & & P & & s \\ \hline Sales & $ & 870,000 & $ & 515,000 \\ \hline Cost of goods sold & & (638,000) & & (360,000) \\ \hline Gross profit & $ & 232,000 & $ & 155,000 \\ \hline Selling expenses & & (22,000) & & (35,000) \\ \hline Other expenses & & (148,000) & & (72,000) \\ \hline \begin{tabular}{l} Interest and \\ dividend income \end{tabular} & & 34,000 & & 2,000 \\ \hline Profit & $ & 96,000 & $ & 50,000 \\ \hline \end{tabular} Show all calculations for partial credit On December 31, 2012, P Inc. purchased 80% of the outstanding ordinary shares of S Company for $310,000. At that date, S had ordinary shares of $200,000 and retained earnings of $60,000. In negotiating the purchase price, it was agreed that the assets on Ss statement of financial position were fairly valued except for plant assets, which had a $40,000 excess of fair value over carrying amount. It was also agreed that S had unrecognized intangible assets consisting of trademarks that had an estimated value of $24,000. The plant assets had a remaining useful life of eight years at the acquisition date and the trademarks would be amortized over a 12-year period. Any goodwill arising from this business combination would be tested periodically for impairment. P accounts for its investment using the cost method. Additional Information: At December 31, 2016, an impairment test of S's goodwill revealed its recoverable amount is $50,000 - An impairment test indicated that the trademarks had a recoverable amount of $13,750. The impairment loss on these assets (goodwill and trademarks) occurred entirely in 2016. - On December 26, 2016, P declared dividends of $36,000, while S declared dividends of $20,000. - Amortization expense is reported in selling expenses, while impairment losses are reported in other expenses. a. Calculate the ending balance of consolidated retained earnings at December 31, 2016. (5 marks) b. Calculate the ending balance of non-controlling interest that would appear on the consolidated balance sheet at December 31, 2016 (5 marks) c. Prepare the consolidated statement of changes in equity for the year ended December 31, 2016. (5 marks) d. Calculate the balance of "Plant Assets @ net" that would show on the consolidated balance sheet at December 31, 2016. (2 marks) e. Calculate the balance of ordinary (common) shares on the consolidated balance sheet at December 31, 2016. (2 marks) f. Prepare the consolidated balance sheet at December 31, 2016 (8 marks) g. Assume that P used the equity method to record its investment in S. What would be the value of the Investment in S account on the P 's separate entity balance sheet at December 31, 2016

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

ACC 120 Wake Tech Financial Accounting W Connect Plus Access

Authors: J. David Spiceland

1st Edition

1308168926, 978-1308168920