Answered step by step

Verified Expert Solution

Question

1 Approved Answer

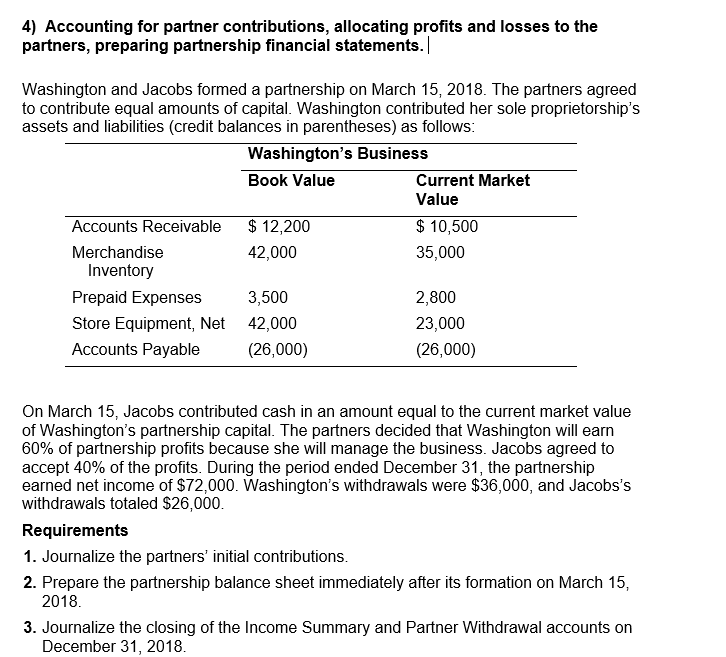

Please only answer this question if you feel confident you are correct; I will give you a like if you can. 4) Accounting for partner

Please only answer this question if you feel confident you are correct; I will give you a like if you can.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Auditing A Risk Based-Approach

Authors: Karla M Johnstone, Audrey A. Gramling, Larry E. Rittenberg

11th Edition

1337619455, 1337619450, 9781337670203 , 978-1337619455