PLEASE ONLY SOLVE C8.48- DO NOT SOLVE C8.46 OR C8.47(they are only for reference) C8446 LOB.1 8.2 8.3 8.4 B. 5 8.6 CBAT LOB.13 Activity-based

PLEASE ONLY SOLVE C8.48- DO NOT SOLVE C8.46 OR C8.47(they are only for reference)

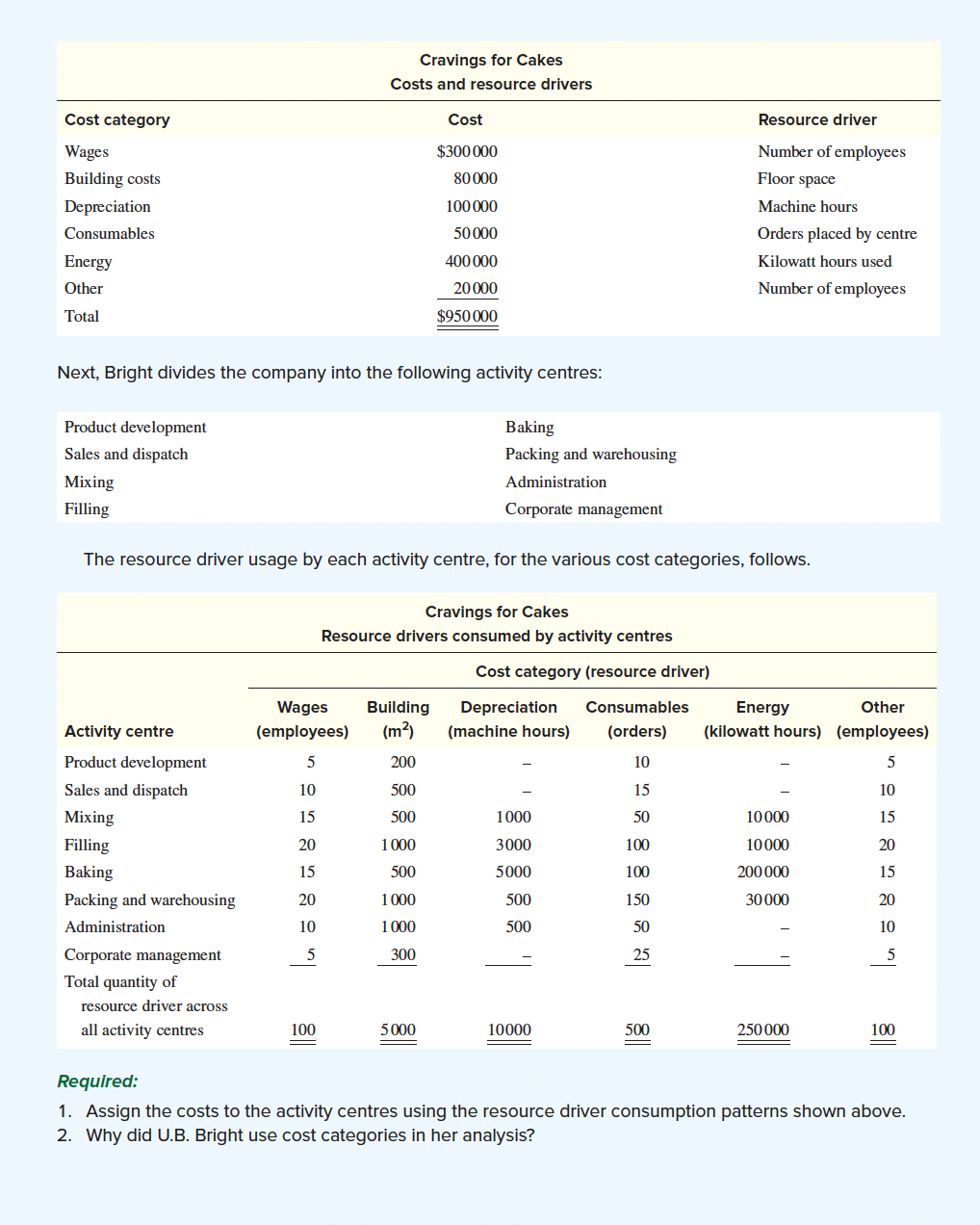

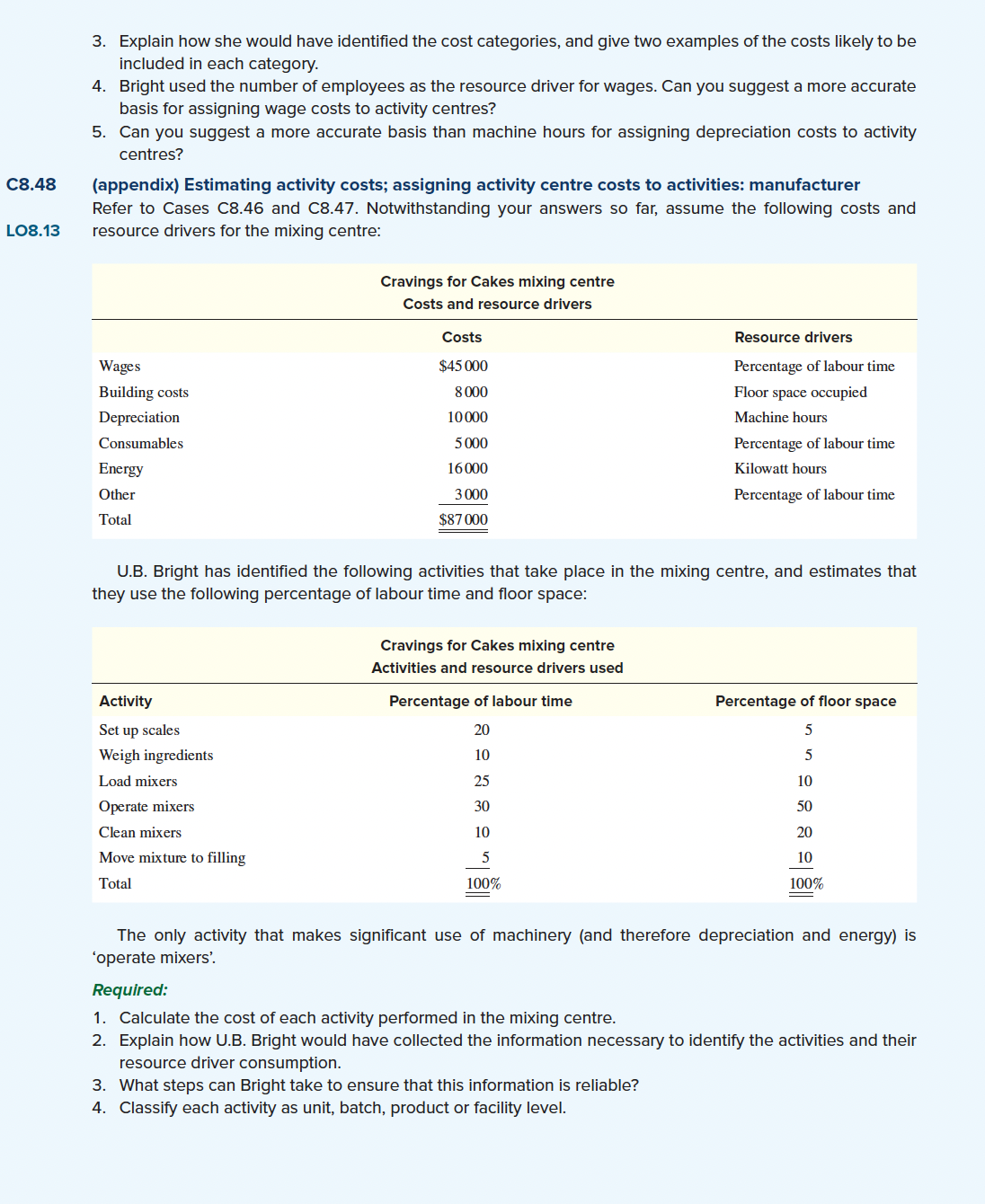

C8446 LOB.1 8.2 8.3 8.4 B. 5 8.6 CBAT LOB.13 Activity-based costing; traditional costing: manufacturer Cravings for Cakes Pty Ltd manufactures a wide range of delicious cakes and pastries. At the annual Christmas party, the company's owner. LM. Craving, treated his employees to a nostalgic review of the rms history. He told them: Twenty years ago we had only three product linespies, finger buns and lamingtons. We were at out producing large volumes of each product, using very simple machinery and a lot of hard work. My how things have changed! We still make and sell a lot of pies and lamingtons, but we also produce a wide range of low-volume lines, such as Danish pastries, doughnuts and vanilla slices. i hear you sighing, and no wonder; these low-volume products are a pain in the neck. They are complex to produce and their short production runs involve a lot of extra machinery setups and material handling. But the accountants tell me that these speciality lines have wonderful prot margins, so we must not complain. Craving then outlined the dramatic changes that had occurred within the business over the past 20 years. In the factory he had seen the introduction of computer-controlled mixing machines and ovens that replaced a lot of the direct labour operations, and an increased emphasis on quality and delivery performance. Indeed, right across the business. more and more effort had been placed on keeping the customer happy. However, his speech cast a gloomy shadow across the Christmas festivities when he warned: Despite all this progress, the company seems to be struggling. Our prots are declining, and if things don 't improve over the next few months, this may be our last Christmas together. To survive we must all work very hard. We must focus on increasing sales, particularly of our high-margin speciality products. The company's management accountant, Ursula B. Bright, had become concerned about the conventional product costing system at Cravings for Cakes. The manufacturing people were also sure that the costing system was distorting product costs. Required: 1. 2. Describe the changes in cost structure that are likely to have occurred at Cravings for Cakes over the last 20 years. and explain their causes. Do you think that the existing costing system understates or overstates the cost of: {a} lamingtons (b) Danish pastries? Explain your answers. Explain how activity-based costing could overcome the deciencies inherent in the existing costing system. What factors should U.B. Bright consider when deciding whether to use: {a} a simple activity-based costing system to assign manufacturing overhead to products {b} an activity-based system that includes both manufacturing overhead and non-manufacturing costs {c} a comprehensive activity-based system that includes all product-related costs except direct material? (appendix) Estimating activity costs; assigning costs to activity centres: manufacturer Refer to Case C8.46. Assume that U.B. Bright decided to implement an activity-based costing system that included all costs except direct material. She identies the following costs, by cost category, for the past year and selects the following resource drivers: Cravings for Cakes Costs and resource drivers Cost category Cost Resource driver Wages $300 000 Number of employees Building costs 80 000 Floor space Depreciation 100 000 Machine hours Consumables 50 000 Orders placed by centre Energy 400 000 Kilowatt hours used Other 20 000 Number of employees Total $950 000 Next, Bright divides the company into the following activity centres: Product development Baking Sales and dispatch Packing and warehousing Mixing Administration Filling Corporate management The resource driver usage by each activity centre, for the various cost categories, follows. Cravings for Cakes Resource drivers consumed by activity centres Cost category (resource driver) Wages Building Depreciation Consumables Energy Other Activity centre (employees) (m?) (machine hours) (orders) (kilowatt hours) (employees) Product development 5 200 10 Sales and dispatch 10 500 15 10 Mixing 15 500 1000 50 10000 15 Filling 20 1 000 3000 100 10 000 20 Baking 15 500 5000 100 200 000 15 Packing and warehousing 20 1 000 500 150 30 000 20 Administration 10 1 000 500 50 10 Corporate management 5 300 25 Total quantity of resource driver across all activity centres 100 5000 10000 500 250 000 100 Required: 1. Assign the costs to the activity centres using the resource driver consumption patterns shown above. 2. Why did U.B. Bright use cost categories in her analysis?CBA-B LOB.13 3. Explain how she would have identied the cost categories, and give two exampies of the costs likely to be included in each category. 4. Bright used the number of employees as the resource driver for wages. Can you suggest a more accurate basis for assigning wage costs to activity centres? 5. Can you suggest a more accurate basis than machine hours for assigning depreciation costs to activity centres? {appendix} Estimating activity costs; assigning activity centre costs to activities: manufacturer Refer to Cases (28.46 and C8.47. Notwithstanding your answers so far. assume the following costs and resource drivers for the mixing centre: Cravings for Cakes mixing centre Costs and resource drivers Costs Resource drivers Wages $45000 Percentage of labour time Building costs 8000 Floor space occupied Depreciation 10000 Machine hours Consumables 5000 Percentage of labour time Energyr 16000 Kilowatt hours Other 3000 Percentage of labour time Total $8? 000 U.B. Bright has identied the following activities that take place in the mixing centre, and estimates that they use the following percentage of labour time and floor space: Cravings for Cakes mixing centre Activities and resource drivers used Activity Percentage of labour time Percentage of floor space Set up scales 20 5 Weigh ingredients 10 5 Load mixers 25 10 Operate mixers 30 50 Clean mixers 10 20' Move mixture to lling _5 E Total @936 @% The only activity that makes signicant use of machinery {and therefore depreciation and energy) is 'operate mixers'. Required: 1. Calculate the cost of each activity performed in the mixing centre. 2. Explain how U.B. Bright would have collected the information necessary to identify the activities and their resource driver consumption. 3. What steps can Bright take to ensure that this information is reliable? Classify each activity as unit, batch, product or facility level. P

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance