Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please Please answer Question #6 all highlighted parts. Thanks CASE12.5 Murchison Technoloaies, lnc Evaluating an Attorney's Response and ldentifying the Proper Audit Report MARK S.

Please Please answer Question #6 all highlighted parts. Thanks

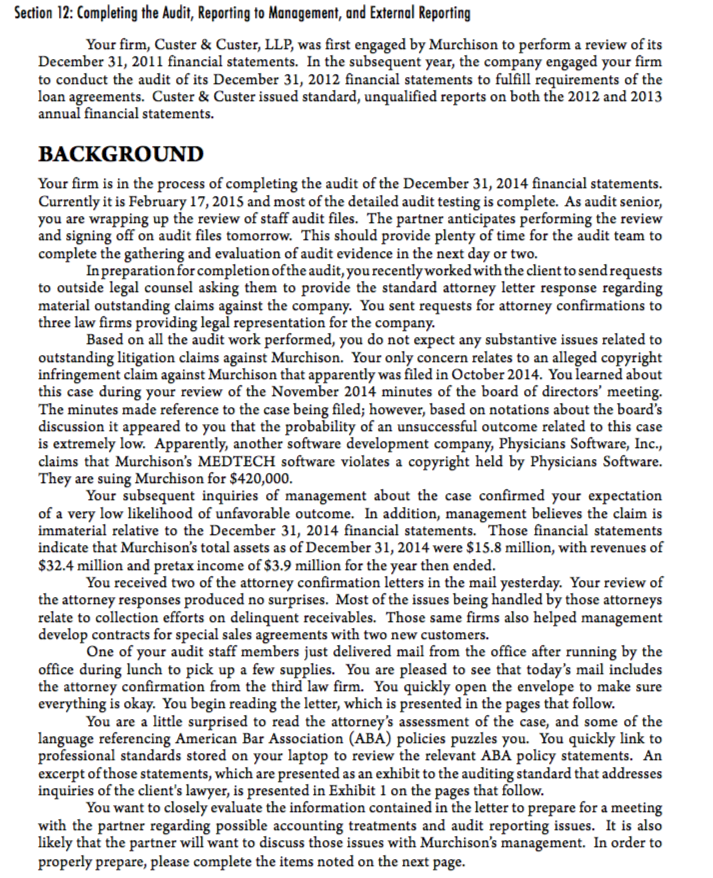

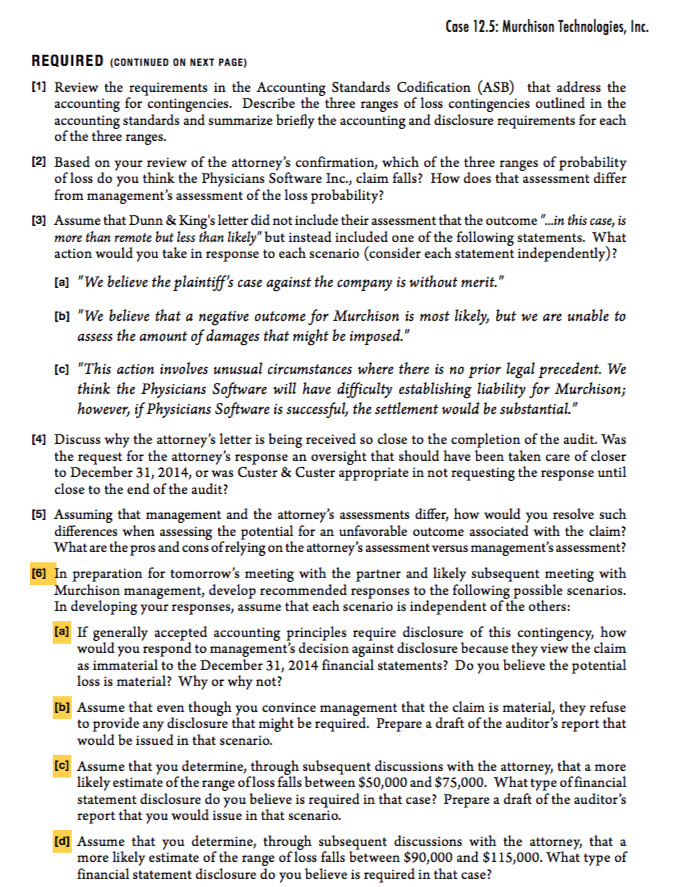

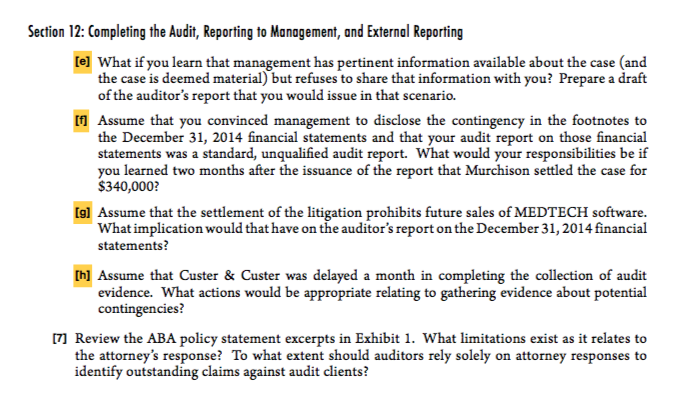

CASE12.5 Murchison Technoloaies, lnc Evaluating an Attorney's Response and ldentifying the Proper Audit Report MARK S. BEASLEY FRANK A. BUCKLESS STEVEN M. GLOVER DOUGLAS F. PRAWITT LEARNING OBJECTIVES After completing and discussing this case you should be able to [11 Understand the role and timing o Go to page 9 3Evaluate proper accounting treatment for attorney responses to the auditor material uncertainties 2 Interpret information contained in an attorney's 4] Identify the correct audit report in light of response letter varying circumstances INTRODUCTION Murchison Technologies, Inc. recently developed a patient-billing software system that it markets to physicians and dentists. Jim Archer and Janice Johnson founded the company in Austin, Texas five years ago after working at IBM for more than 15 years. Jim worked as a software programmer and Janice worked as a sales representative, frequently calling on stand-alone medical practices. Together, they identified a need for software to help physician and dental offices track charges for patient services provided by doctors and their staff. With the initial backing of three local venture capitalists, they left IBM, created Murchison Technologies, and devoted their full-time efforts to the development of the billing system software. For more than three years, they worked on developing the software. After extensive pilot testing, the company shipped its firstproduct to customers in early 2012. Sales have been surprisingly strong for the product, which is marketed as MEDTECH Software. Feedback from physicians and dentists has been extremely positive. Most note that billing clerks and office staff find the system quite flexible in tracking numerous types of services for large numbers of patients. Most are pleased with the ability to customize system features for their unique practice needs. Another key to the product's success is the relative cost of the software and the minimal upgrades required of the office microcomputers and networks to operate the software. The company has gradually added employees to its staff. Currently, Murchison employs mers who continually update the software for emerging about 60 people, including software program technological developments. Janice serves as chief executive officer (CEO), and Jim serves as president. While both serve on the board of directors, they ultimately are accountable to the board, which also includes representatives from the three venture capitalists and two local bankers who financed company expansions through commercial loans issued three years ago. Murchison continues to be privately held. Case 12.5: Murchison Technologies, Inc. REQUIRED (CONTINUED ON NEXT PAGE) [11 Review the requirements in the Accounting Standards Codification (ASB) that address the accounting for contingencies. Describe the three ranges of loss contingencies outlined in the accounting standards and summarize briefly the accounting and disclosure requirements for each of the three ranges. 21 Based on your review of the attorney's confirmation, which of the three ranges of probability of loss do you think the Physicians Software Inc., claim falls? How does that assessment differ from management's assessment of the loss probability? [3] Assume that Dunn & King's letter did not include their assessment that the outcome .in this case, is more than remote but less than likely" but instead included one of the following statements. What action would you take in response to each scenario (consider each statement independently)? [al "We believe the plaintiff's case against the company is without merit." [bl "We believe that a negative outcome for Murchison is most likely, but we are unable to assess the amount of damages that might be imposed." [cl "This action involves unusual circumstances where there is no prior legal precedent. We think the Physicians Software will have difficulty establishing liability for Murchison; however, if Physicians Software is successful, the settlement would be substantial." [4] Discuss why the attorney's letter is being received so close to the completion of the audit. Was the request for the attorney's response an oversight that should have been taken care of closer to December 31,2014, or was Custer&Custer appropriate in not requesting the response until close to the end of the audit? [5] Assuming that management and the attorney's assessments differ, how would you resolve such differences when assessing the potential for an unfavorable outcome associated with the claim? What are the pros and cons of relying on the attorney's assessment versus management's assessment? [61 In preparation for tomorrow's meeting with the partner and likely subsequent meeting with Murchison management, develop recommended responses to the following possible scenarios. In developing your respo nses, assume that each scenario is independent of the others: [al If generally accepted accounting principles require disclosure of this contingency, how would you respond to management's decision against disclosure because they view the claim as immaterial to the December 31, 2014 financial statements? Do you believe the potential loss is material? Why or why not? bl Assume that even though you convince management that the claim is material, they refuse to provide any disclosure that might be required. Prepare a draft of the auditor's report that would be issued in that scenario. el Assume that you determine, through subsequent discussions with the attorney, that a more likely estimate of the range ofloss falls between $50,000 and $75,000. What type of financial statement disclosure do you believe is required in that case? Prepare a draft of the auditor's report that you would issue in that scenario. [d] Assume that you determine, through subsequent discussions with the attorney, that a more likely estimate of the range of loss falls between $90,000 and $115,000. What type of financial statement disclosure do you believe is required in that case? Section 12: Completing the Audit, Reporting to Management, and External Reporting el What if you learn that management has pertinent information available about the case (and the case is deemed material)but refuses to share that information with you? Prepare a draft of the auditor's report that you would issue in that scenario. Assume that you convinced management to disclose the contingency in the footnotes to the December 31, 2014 financial statements and that your audit report on those financial statements was a standard, unqualified audit report. What would your responsibilities be if you learned two months after the issuance of the report that Murchison settled the case for $340,000? sl Assume that the settlement of the litigation prohibits future sales of MEDTECH software. What implication would that have on the auditor's report on the December 31, 2014 financial statements? h] Assume that Custer &Custer was delayed a month in completing the collection of audit evidence. What actions would be appropriate relating to gathering evidence about potential contingencies? 7] Review the ABA policy statement excerpts in Exhibit 1. What limitations exist as it relates to the attorney's response? To what extent should auditors rely solely on attorney responses to identify outstanding claims against audit clientsStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Audit Customer Satisfaction Marketing Added Value

Authors: Cindy E. Cosmas

1st Edition

089413373X, 978-0894133732