Question

PLEASE PLEASE HELP , Financial Needs and Constraints Analysis Jack and Natalie Novak, aged 32 and 30 respectively, are living in a house they bought

PLEASE PLEASE HELP ,

Financial Needs and Constraints Analysis

Jack and Natalie Novak, aged 32 and 30 respectively, are living in a house they bought last year. They have only one child, Martin, aged 3, but they plan to have another child in two or three years. They have become a little concerned about their finances lately Jack is an engineer for a large auto parts manufacturer and Natalie is a legal secretary. Jacks gross salary is $65,000 per year, but after all deductions, he takes home $3,700 per month. Natalie gets $31,000 per year and nets about $1,950 per month. Jacks eight-year-old Volvo has been giving him lots of costly troubles in the last year, so he has asked the bank about a car loan. Also, the Novaks are interested in getting a personal line of credit as they sometimes experience cash-flow problems. They have been asked by the bank to supply a personal balance sheet and an income and expenditure statement. They have asked you to prepare these for them. They have provided you with a list of financial information as follows:

Cash on hand $ 175

Bank account balance 950

Term deposit 5,000

Canada Savings Bond 1,800

Home 250,000

Home mortgage balance 180,000

Jacks car (8 years old) 3,000

Natalies car (1 year old) 15,000

Car loan on Natalies car 12,500

Monthly mortgage payment 1,292

Monthly car-loan payment 403

Bills outstanding:

Telephone 35

Hydro 95

Visa (minimum due $83) 2,816

Master Card (minimum due $10) 150

Insurance (cars) 2,220

Estimated monthly expenditures:

Groceries 800

Gas and auto expenses 180

Daycareursery 600

Utilities 350

Newspaper and magazines 50

Alcohol and cigarettes 100

Entertainment 300

Clothes 200

Miscellaneous 200

Personal assets 20,000

Jacks RRSP (in term deposits) 3,000

Natalies RRSP (in a stock mutual fund) 6,000

Jack comments further, Before we bought the house last year we had no money problems. By the way, I have forgotten the property tax of about $1,800 and the home insurance premium of $450. Last year, I spent over $700 on landscaping. We really enjoy the home and the neighbors are nice, but it is costing us a lot more than we thought. I borrowed $25,000 from my father for the down payment. He is kind enough to charge me no interest, but I hope to pay him back as soon as possible, like several thousand dollars a year. Fortunately, I have a nice job and the benefits are good medical and drug plan, pension plan, life and disability insurance ... You name it, I have it! Natalie does not get any of those things, but my medical plans cover the whole family. Last year, we got tax refunds of $500 and $250, which we spent on a one-week vacation. We usually take a vacation once a year. How much does it cost? Well, it depends on where we go ... about $2,000, I would say.

Required:

Using the information provided, prepare a statement of net worth, (Table 4.3) and a personal income statement (Table 4.9 and 4.10) for the Novaks.

Based on the statements you prepared, discuss and comment on the Novaks financial situation. (Refer to the Debt management guidelines for the Woodhaven Family in the text and on DC Connect for an example.)

Table 4.10 How Much Did You Save?

Canada/Qubec Pension Plan: employer and employee portions + Employer pension: employees contributions + interest + Employer pension: employers cont. + interest, if vested + Mortgage principal repayments + Deferred profit sharing plan cont. and interest + Unrealized capital gains on investments = Net cash flow

Debt Management Guidelines - Application to the Woodhaven Family

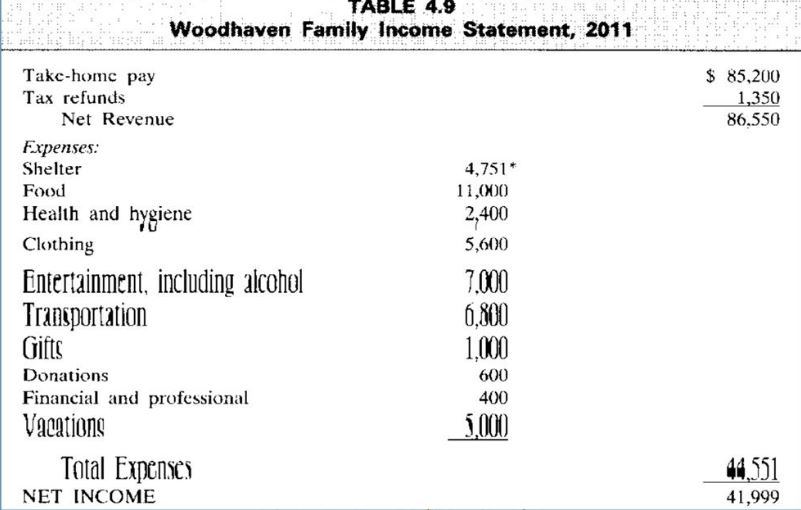

1. We note that their consumer debt of $41,500 (credit card balances of $36,000 and car loan of $5,500) exceed 20% of their take-home pay (20% $85,200) or $17,040. According to this guideline, this family has too much consumer debt.

2. The family should pay down or pay off consumer debt as soon as possible. But, where does the family find money to do so? The Woodhaven Family can sell $30,000 of their mutual fund to pay off the credit card balance, resulting in substantial savings in interest payments. See next point.

3. Convert consumer loan to investment loan. The Woodhaven family has $30,000 of a mutual fund and $36,000 of credit card balance. They can sell $30,000 of the mutual fund, use the proceeds to retire $30,000 of credit card balance, and then borrow $30,000 to invest in a similar mutual fund. By doing so, they will have converted a consumer debt to an investment loan. The credit card balances charge high-interest rate. An investment loan to buy mutual fund charges much lower interest says 5%. In addition, the interest expense on the investment loan is tax deductible. There are two benefits of this conversion. First, they save on interest expense. They will pay off the credit cards in descending order of interest rates, i.e., $4,000 of department store charge card at 24%, $20,000 of Visa card that charges 18% interest, and $6,000 of Master Card that charges 16% interest. Total interest savings will be ($4,000 .24) + ($20,000 .18) + ($6,000 .16) = $5,520 per year. The interest on the $30,000 investment loan at 5% is equal to (.05 $30,000) or $1,500. In addition, the interest expense is tax deductible. If their marginal tax rate is 30%, they will save ($1,500 .30) or $450 in taxes. Total savings will be $5,520 $1,500 + $450 = $4,470 per year.

4. Check negative cash flow and payment for it. If the mutual fund they purchase does not pay the dividend, the investment loan will have a negative cash flow of $1,500 per year. This is relieved by a tax saving of $450. But they have paid off $30,000 of credit card balances with substantial savings in interest expense. The savings is more than enough to pay for the negative cash flow of the investment loan.

Other Debt Management Guidelines - Application to the Woodhaven Family

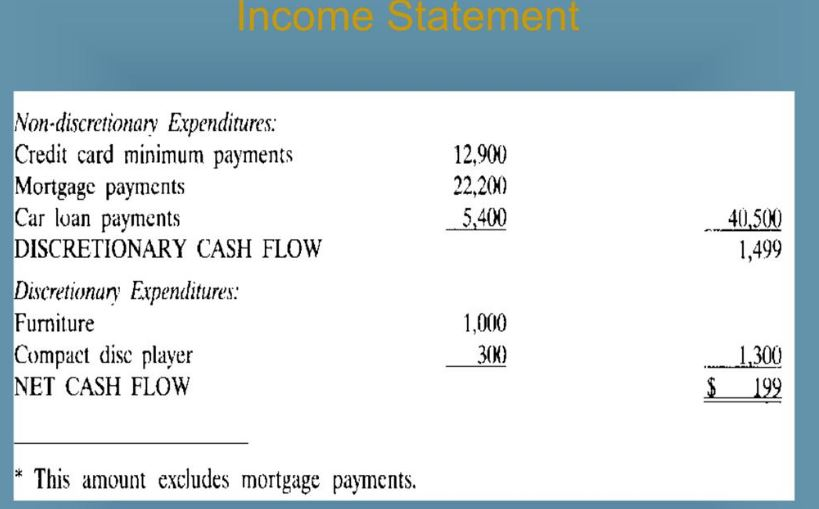

1. They should save ($85,200 .10) or $8,520 per year. Last year, they saved only $199, which means they should save a lot more.

2. They will write a cheque to themselves every month before paying anyone else. Deposit the cheque in an investment account, and let the money accumulate for long-term investment later. Make a commitment not to touch the money. The cheque will be about $8,520 12 or $710 per month.

3. They have only $1,000 cash, which is too low. Aim for at least three months take-home pay, which is equal to $21,300. Leave the money in a liquid interest-bearing account to cover emergencies or unevenness of cash flow.

4. Set short-term goal, such as cutting expenses, and set deadlines for the goals. 5. Set long-term goals, such as retirement goals.

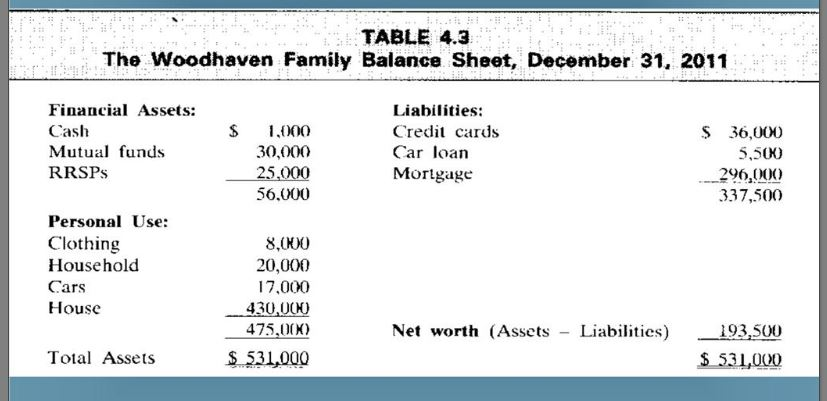

TABLE 4.3 The Woodhaven Family Balance Sheet, December 31, 2011 Financial Assets: Liabilities: Cash 1.0000 Credit cards S 36,000) Mutual funds 30,000 Car loan 5.500 25,000 RRSPs Mortgage 290,0000) 56.000 337,500 Personal Use Clothing 8,0NO 20,000 Household Cars 17,000 House 430,000 475,0(K) Net worth (Assets Liabilities) 193,500 Total Assets D00 53,000Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Environmental And Safety Auditing Program Strategies For Legal International And Financial Issues

Authors: Unhee Kim, John F. Falkenbury, Timothy A. Wilkins, Ralph Rhodes, Richard J. Satterfield

1st Edition

1566702461, 978-1566702461