Answered step by step

Verified Expert Solution

Question

1 Approved Answer

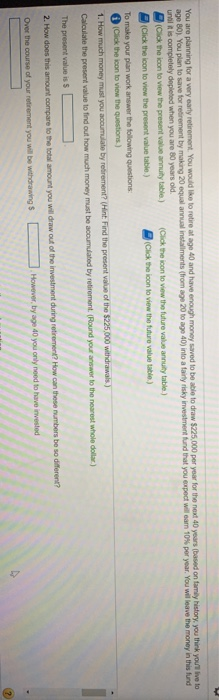

please print clearly. Thank you! You are planning for a very early retirement you would like to retire at age 40 and have enough money

please print clearly. Thank you!

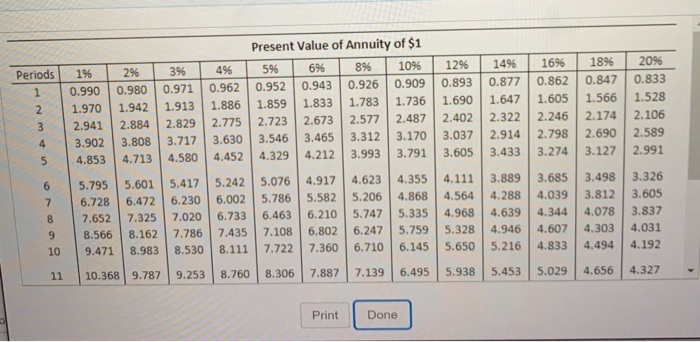

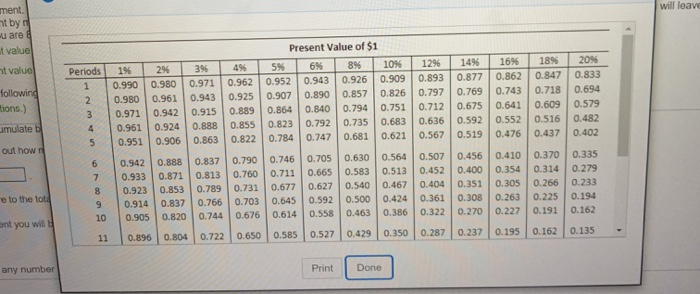

You are planning for a very early retirement you would like to retire at age 40 and have enough money Saved to be able to draw $225,000 per year for the next 40 years based on my history. you think you live to age 80). You plan to save for retirement by making 20 equal annual installments (fromage 20 to age 40) into a fairly risky investment fund that you expect will com 10% per year. You will leave the money in this fund unal is completely depicted when you are 50 years old (Cick the icon to view the present value annuity table.) (Click the icon to view the future value annuity table) Click the icon to view the present value table) Click the icon to view the future value table.) To make your plan work answer the following questions: Click the icon to view the questions.) 1. How much money must you accumulate by retirement? (Hint Find the present value of the $225,000 withdrawals.) Calculate the present value to find out how much money must be accumulated by retirement. (Round your answer to the nearest whole dollar) The present value is $ 2. How does this amount compare to the total amount you will draw out of the investment during retirement? How can these numbers be so different? However, by age 40 you only need to have invested Over the course of your retirement you will be withdrawing $ Periods 1 2 3 Present Value of Annuity of $1 1% 2% 3% 496 5% 6% 8% 10% 12% 14% 0.990 0.980 0.971 0.962 0.952 0.943 0.926 0.9090.893 0.877 1.970 1.942 1.913 1.886 1.859 1.833 1.783 1.736 1.690 1.647 2.941 2.884 2.8292.775 2.723 2.673 2.577 2.487 2.402 2.322 3.902 3.808 3.717 3.630 3.546 3.465 3.312 3.170 3.037 2.914 4.8534.713 4.580 4.452 4.329 4.212 3.993 3.791 3.605 3.433 5.795 5.601 5.417 5.2425.076 4.917 4.623 4.355 4.111 3.889 6.728 6.472 5.786 5.582 5.206 4.868 4.5644.288 7.652 7.3257.020 6.733 6.463 6.210 5.747 5.335 4.968 4.639 8.566 8.162 | 7.786 7.435 7.108 6.802 6.247 5.759 5.328 4.946 9.471 8.983 7.722 7.360 6.710 6.145 5.650 5.216 10.368 9.787 9.253 8.760 8.306 7.887 7.139 6.495 5.938 5.453 16% 0.862 1.605 2.246 2.798 3.274 18% 0.847 1.566 2.174 2.690 3.127 20% 0.833 1.528 2.106 2.589 2.991 3.685 4.039 4.344 4.607 4.833 5.029 3.498 3.498 3.812 4.078 4.303 4.494 4.656 3.326 3.605 3.837 4.031 4.192 4.327 Print Done till leav Nel it by u are value it valuo Periods following mons.) mulate out how 1% 0.990 0.980 0.971 0.961 0.951 3 4 2% 0.980 0.961 0.942 0.924 0.906 3% 0.971 0.943 0.915 0.888 0.863 4% 0.962 0.925 0.889 0.855 0.822 Present Value of $1 5% 6% 8% 10% 0.952 0.943 0.926 0.909 0.907 0.890 0.8570.826 0.864 0.840 0.794 0.751 0.823 0.792 0.735 0.683 0.784 0.747 0.681 0.621 1696 18% 0.862 0.847 0.7430.718 0.641 0.609 0.552 0.516 0.476 0.437 20% 0.833 0.694 0.579 0.482 0.402 0.335 0.279 12% 14% 0.893 0.877 0.797 0.769 0.712 0.675 0.636 0.592 0.567 0.519 0.507 0.456 0.4520.400 0.404 0.351 0.361 0.308 0.322 0.270 0.287 0.237 7 8 0.942 0.933 0.923 0.914 0.905 0.896 e to the tota 0.888 0.837 0.871 0.813 0.853 0.789 0.837 0.766 0.820 0.744 0.804 0.722 0.790 0.746 0.705 0.7600.711 0.665 0.731 0.677 0.627 0.703 0.6450.592 0.676 0.614 0.558 0.650 0.58 0.527 0.630 0.564 0.583 0.513 0.540 0.467 0.500 0.424 0.463 0.386 0.429 0.350 0.410 0.354 0.305 0.263 0.227 0.19 0.370 0.314 0.266 0.225 0.191 0.162 ent you will 0.194 0.162 0.135 11 - any number Print | Done Future Value of $1 Periods 6 1030 1.061 1.093 1.126 1.159 1.040 1.082 1.125 1.170 1.217 1.050 1.103 1.158 1.216 1.276 12 1010 1020 1.020 1.040 1.030 1.061 1.041 1.082 1.051 1.104 1.062 1.126 1.072 1.149 1.083 1.172 1.034 1.195 1.105 1.219 1.060 1. 124 1.191 1.262 1.338 1.080 1.166 1.260 1.360 1.469 10% 1.100 1.210 1.331 1.454 1.611 12% 1.120 1.254 1.405 1.574 1.762 14 1.140 1300 1.482 1.689 1.925 1.346 1.561 1.811 2.100 1200 1.440 1.728 2.074 2.488 1.392 1.643 1.939 2.288 2.700 3.165 1.194 2.986 3.583 1.230 1.265 1.316 1.369 1.423 1.480 1.340 1.407 1.477 1.551 1.629 1.419 1.500 1.594 1.689 1.257 1.587 1.714 1.851 1.999 2.159 1.772 1.949 2.144 2.358 2.594 1.974 2.211 2.476 2.773 3.106 2.195 2.502 2 353 3.252 1207 2.436 2.826 3.278 3.803 1.305 3.160 6.192 1.344 411 5.234 Print Done These numbers are different because OA You need to have far more accumulated than what you wil withdraw because you wil withdraw a large portion of the investment every year the balance remains invested where it continues to earn 10% interest OD You need to have for loss acumulated than what you will withdraw s you only withdraw a portion of the investment every year the balance romans invested where I continues to earn 109 inforest c. You need to have the same accumulated as you will withdraw because you will not earn further interest on your investment when you reach retirement OD. None of the above Choose from any list or enter any number in the input fields and then continue to the next question 3. How much must you pay into the investment each year for the first twenty years? Hint Your answer from Requirement becomes the future value of this aruty Round your answer to the nearest whole dollar) You must pay $ into the investment each year for the first twenty years 4. How does the total out-of-pocket vos compare to the investment's value at the end of the worlar sawgs period and the withdrawals you will make agrement (Use the investment rounded to the nors who uber that you could bove, then found your finalen er lo there who do The total out-of-pocket savings amounts to $ This is for than the investment's worth of the end of twenty years and remarkably than the amount of money you will eventually withdraw from the investment Com m on I n ter any number in the input fields and then continue to the next question You are planning for a very early retirement you would like to retire at age 40 and have enough money Saved to be able to draw $225,000 per year for the next 40 years based on my history. you think you live to age 80). You plan to save for retirement by making 20 equal annual installments (fromage 20 to age 40) into a fairly risky investment fund that you expect will com 10% per year. You will leave the money in this fund unal is completely depicted when you are 50 years old (Cick the icon to view the present value annuity table.) (Click the icon to view the future value annuity table) Click the icon to view the present value table) Click the icon to view the future value table.) To make your plan work answer the following questions: Click the icon to view the questions.) 1. How much money must you accumulate by retirement? (Hint Find the present value of the $225,000 withdrawals.) Calculate the present value to find out how much money must be accumulated by retirement. (Round your answer to the nearest whole dollar) The present value is $ 2. How does this amount compare to the total amount you will draw out of the investment during retirement? How can these numbers be so different? However, by age 40 you only need to have invested Over the course of your retirement you will be withdrawing $ Periods 1 2 3 Present Value of Annuity of $1 1% 2% 3% 496 5% 6% 8% 10% 12% 14% 0.990 0.980 0.971 0.962 0.952 0.943 0.926 0.9090.893 0.877 1.970 1.942 1.913 1.886 1.859 1.833 1.783 1.736 1.690 1.647 2.941 2.884 2.8292.775 2.723 2.673 2.577 2.487 2.402 2.322 3.902 3.808 3.717 3.630 3.546 3.465 3.312 3.170 3.037 2.914 4.8534.713 4.580 4.452 4.329 4.212 3.993 3.791 3.605 3.433 5.795 5.601 5.417 5.2425.076 4.917 4.623 4.355 4.111 3.889 6.728 6.472 5.786 5.582 5.206 4.868 4.5644.288 7.652 7.3257.020 6.733 6.463 6.210 5.747 5.335 4.968 4.639 8.566 8.162 | 7.786 7.435 7.108 6.802 6.247 5.759 5.328 4.946 9.471 8.983 7.722 7.360 6.710 6.145 5.650 5.216 10.368 9.787 9.253 8.760 8.306 7.887 7.139 6.495 5.938 5.453 16% 0.862 1.605 2.246 2.798 3.274 18% 0.847 1.566 2.174 2.690 3.127 20% 0.833 1.528 2.106 2.589 2.991 3.685 4.039 4.344 4.607 4.833 5.029 3.498 3.498 3.812 4.078 4.303 4.494 4.656 3.326 3.605 3.837 4.031 4.192 4.327 Print Done till leav Nel it by u are value it valuo Periods following mons.) mulate out how 1% 0.990 0.980 0.971 0.961 0.951 3 4 2% 0.980 0.961 0.942 0.924 0.906 3% 0.971 0.943 0.915 0.888 0.863 4% 0.962 0.925 0.889 0.855 0.822 Present Value of $1 5% 6% 8% 10% 0.952 0.943 0.926 0.909 0.907 0.890 0.8570.826 0.864 0.840 0.794 0.751 0.823 0.792 0.735 0.683 0.784 0.747 0.681 0.621 1696 18% 0.862 0.847 0.7430.718 0.641 0.609 0.552 0.516 0.476 0.437 20% 0.833 0.694 0.579 0.482 0.402 0.335 0.279 12% 14% 0.893 0.877 0.797 0.769 0.712 0.675 0.636 0.592 0.567 0.519 0.507 0.456 0.4520.400 0.404 0.351 0.361 0.308 0.322 0.270 0.287 0.237 7 8 0.942 0.933 0.923 0.914 0.905 0.896 e to the tota 0.888 0.837 0.871 0.813 0.853 0.789 0.837 0.766 0.820 0.744 0.804 0.722 0.790 0.746 0.705 0.7600.711 0.665 0.731 0.677 0.627 0.703 0.6450.592 0.676 0.614 0.558 0.650 0.58 0.527 0.630 0.564 0.583 0.513 0.540 0.467 0.500 0.424 0.463 0.386 0.429 0.350 0.410 0.354 0.305 0.263 0.227 0.19 0.370 0.314 0.266 0.225 0.191 0.162 ent you will 0.194 0.162 0.135 11 - any number Print | Done Future Value of $1 Periods 6 1030 1.061 1.093 1.126 1.159 1.040 1.082 1.125 1.170 1.217 1.050 1.103 1.158 1.216 1.276 12 1010 1020 1.020 1.040 1.030 1.061 1.041 1.082 1.051 1.104 1.062 1.126 1.072 1.149 1.083 1.172 1.034 1.195 1.105 1.219 1.060 1. 124 1.191 1.262 1.338 1.080 1.166 1.260 1.360 1.469 10% 1.100 1.210 1.331 1.454 1.611 12% 1.120 1.254 1.405 1.574 1.762 14 1.140 1300 1.482 1.689 1.925 1.346 1.561 1.811 2.100 1200 1.440 1.728 2.074 2.488 1.392 1.643 1.939 2.288 2.700 3.165 1.194 2.986 3.583 1.230 1.265 1.316 1.369 1.423 1.480 1.340 1.407 1.477 1.551 1.629 1.419 1.500 1.594 1.689 1.257 1.587 1.714 1.851 1.999 2.159 1.772 1.949 2.144 2.358 2.594 1.974 2.211 2.476 2.773 3.106 2.195 2.502 2 353 3.252 1207 2.436 2.826 3.278 3.803 1.305 3.160 6.192 1.344 411 5.234 Print Done These numbers are different because OA You need to have far more accumulated than what you wil withdraw because you wil withdraw a large portion of the investment every year the balance remains invested where it continues to earn 10% interest OD You need to have for loss acumulated than what you will withdraw s you only withdraw a portion of the investment every year the balance romans invested where I continues to earn 109 inforest c. You need to have the same accumulated as you will withdraw because you will not earn further interest on your investment when you reach retirement OD. None of the above Choose from any list or enter any number in the input fields and then continue to the next question 3. How much must you pay into the investment each year for the first twenty years? Hint Your answer from Requirement becomes the future value of this aruty Round your answer to the nearest whole dollar) You must pay $ into the investment each year for the first twenty years 4. How does the total out-of-pocket vos compare to the investment's value at the end of the worlar sawgs period and the withdrawals you will make agrement (Use the investment rounded to the nors who uber that you could bove, then found your finalen er lo there who do The total out-of-pocket savings amounts to $ This is for than the investment's worth of the end of twenty years and remarkably than the amount of money you will eventually withdraw from the investment Com m on I n ter any number in the input fields and then continue to the next Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Merchandising Math A Managerial Approach

Authors: Doris Kincade, Fay Gibson, Ginger Woodard

1st Edition

0130995886, 978-0130995889