Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please provide a detailed analysis and calculations, I will rate your full star and recommendations, Thank you. Munzad Clock Company (A) As Adam Munzad, president

Please provide a detailed analysis and calculations, I will rate your full star and recommendations, Thank you.

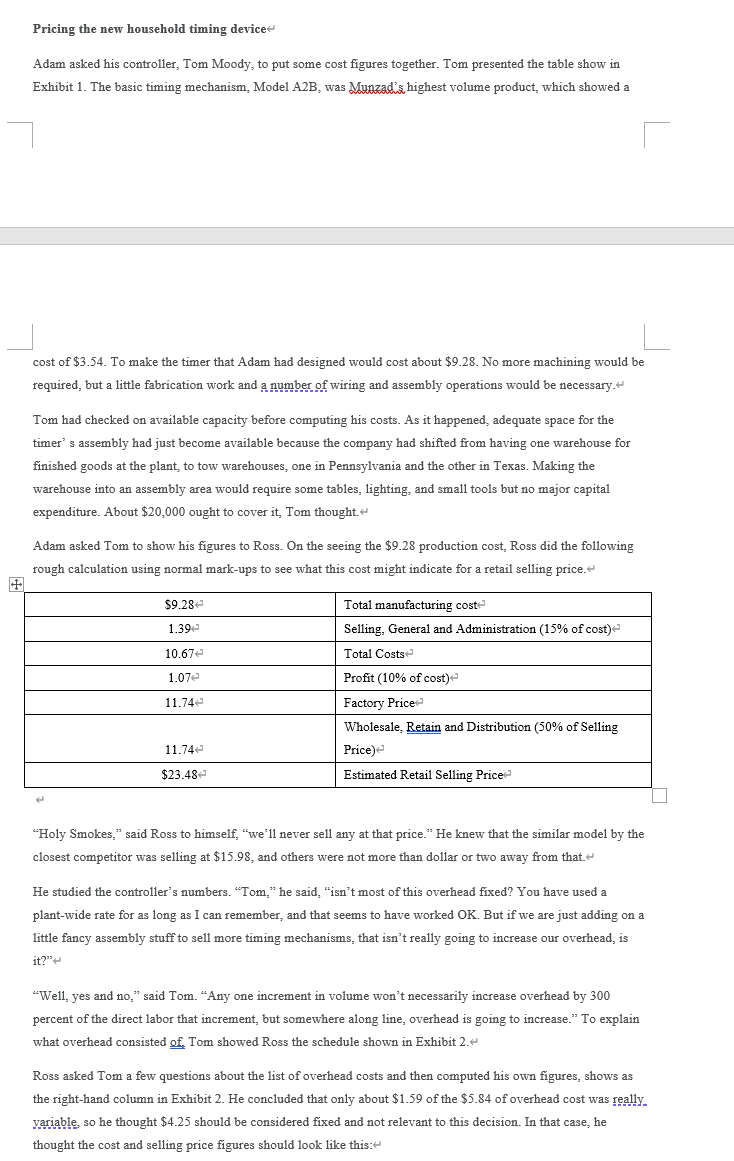

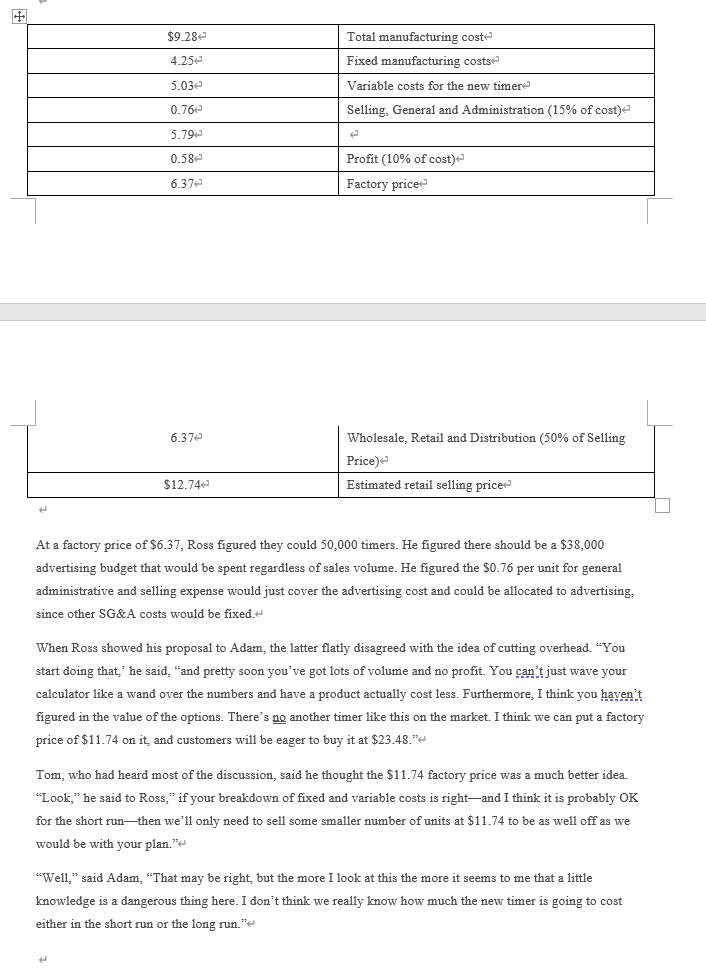

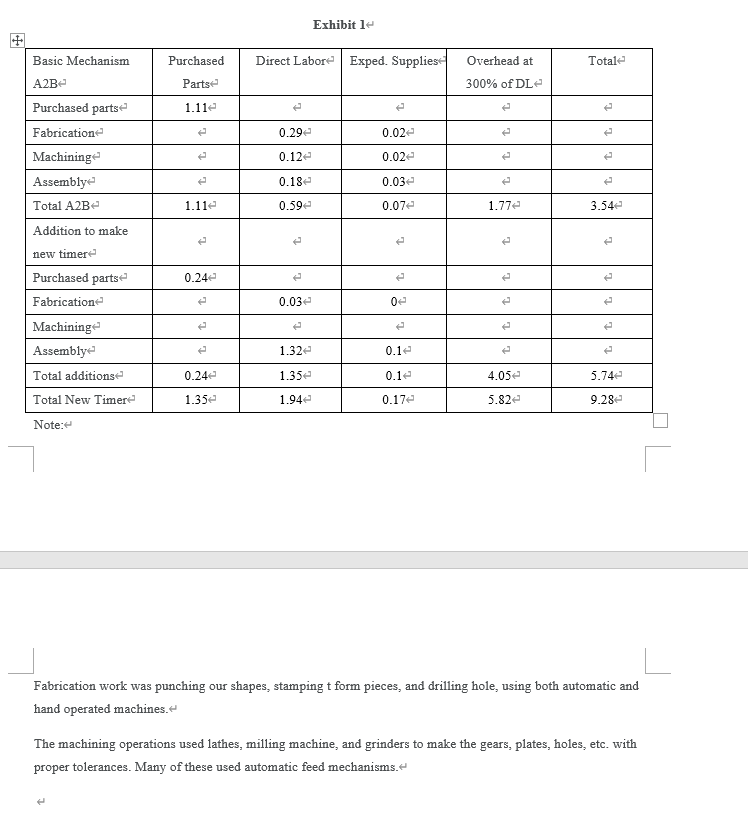

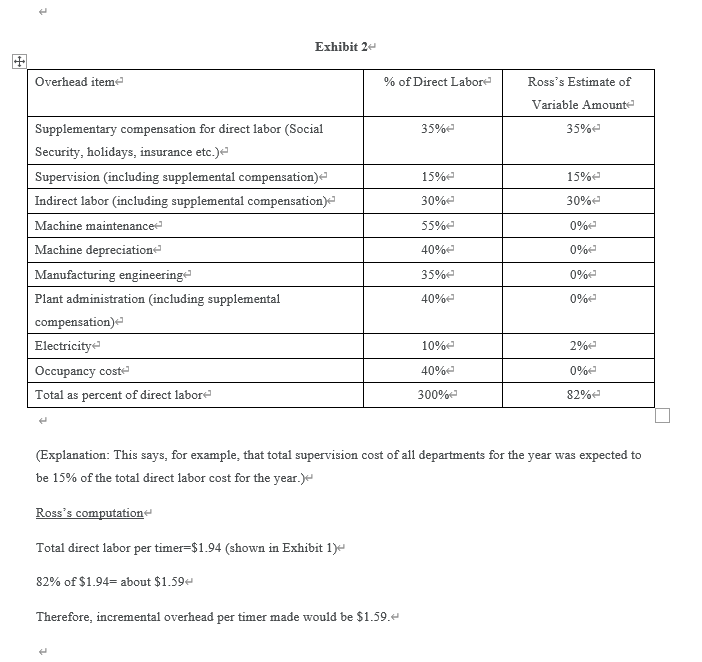

Munzad Clock Company (A)" As Adam Munzad, president of the Munzad Clock Company, stared at the numbers compiled by his controller, Tom Moody, and his sales manager Ross Taylor, the look on his face was one of confusion. The more I look at this the more it looks like we really don't know how much this new household timer is going to cost. We need to get a better handle on the costs of this thing or we will never abe able to decide how to price it." The Company Munzad Clock Company was started by Adam Munzad, the company's president, in 1995. In 2008. Munzad had sold out to Meghna Appliance Corporation, but he remained with the company as Munzad Clock's president. Originally, Munzad Clock made decorative electric clocks, but by 2002 Adam had decided he was much better at making the works than the decorations. So the company shifted to making accurate, durable, but inexpensive electric timing mechanisms. The company now made only three basic models, differing in size and strength. Slight modifications were made to fit each customer's needs. Sales had grown to over $50 million, and timing mechanisms were made to fit each customer's needs. Sales had grown to over $50 million, and the timing mechanisms were made entirely for producers of timed electrical appliances. About half of Munzadis output went to Meghna appliance and about half to other companies. The new household timing device It all started because sometime over the 2010 Labor Day weekend, Adam Munzad's house was burgled while he and his family were enjoying the last days of their summer vacation. Thereafter, though he knew he was closing the proverbial barn door after the cow had gone, Adam did a number of things to try to prevent a repetition Besides improving locks, he bought two timers that could be set to run on house lights in the evening. That is what gave him the idea to make a better timing mechanism for household use, one that head two features that he thought made his timer superior to those currently on the market. The Munzad timer had two options: a 48-hour cycle (so that lights would not turn on and off at the same time each day), or two different 24-hour cycles, so that one timer could operate two lights, each on a different 24-hour cycle. The design of these features was quite simple. There were two different 24-hour cycles, and for the 48-hour option, the timer switched back and forth. Adam's sales manager, Ross Taylor, was not sure how or valuable these options would be to the potential customer. Furthermore, this complete product would have to be sold through wholesalers and manufacturers representatives, which were new to Muuzad Clock. Price, he thought, would be an important factor since other timers were on the market. Pricing the new household timing device Adam asked his controller, Tom Moody, to put some cost figures together. Tom presented the table show in Exhibit 1. The basic timing mechanism, Model A2B, was Mynzadis highest volume product, which showed a cost of $3.54. To make the timer that Adam had designed would cost about $9.28. No more machining would be required, but a little fabrication work and a number of wiring and assembly operations would be necessary. Tom had checked on available capacity before computing his costs. As it happened adequate space for the timer's assembly had just become available because the company had shifted from having one warehouse for finished goods at the plant, to tow warehouses, one in Pennsylvania and the other in Texas. Making the warehouse into an assembly area would require some tables, lighting, and small tools but no major capital expenditure. About $20,000 ought to cover it, Tom thought. Adam asked Tom to show his figures to Ross. On the seeing the $9.28 production cost, Ross did the following rough calculation using normal mark-ups to see what this cost might indicate for a retail selling price. $9.282 1.39 10.67e 1.07 Total manufacturing coste Selling, General and Administration (15% of cost) Total Costs Profit (10% of cost) Factory Price Wholesale, Retain and Distribution (50% of Selling Price) Estimated Retail Selling Price 11.74 11.74 $23.48 "Holy Smokes," said Ross to himself, "we'll never sell any at that price." He knew that the similar model by the closest competitor was selling at $15.98, and others were not more than dollar or two away from that. He studied the controller's numbers. "Tom," he said, "isn't most of this overhead fixed? You have used a plant-wide rate for as long as I can remember, and that seems to have worked OK. But if we are just adding on a little fancy assembly stuff to sell more timing mechanisms, that isn't really going to increase our overhead, is it?" "Well, yes and 110," said Tom. "Any one increment in volume won't necessarily increase overhead by 300 percent of the direct labor that increment, but somewhere along line, overhead is going to increase." To explain what overhead consisted of. Tom showed Ross the schedule shown in Exhibit 2.- Ross asked Tom a few questions about the list of overhead costs and then computed his own figures, shows as the right-hand column in Exhibit 2. He concluded that only about $1.59 of the $5.84 of overhead cost was really. variable, so he thought $4.25 should be considered fixed and not relevant to this decision. In that case, he thought the cost and selling price figures should look like this: $9.28 4.25e Total manufacturing coste Fixed manufacturing costse Variable costs for the new timere Selling, General and Administration (15% of cost) 5.03 0.76 5.79 0.58 Profit (10% of cost) Factory price 6.374 6.37e Wholesale, Retail and Distribution (50% of Selling Price) Estimated retail selling price $12.742 At a factory price of $6.37, Ross figured they could 50,000 timers. He figured there should be a $38.000 advertising budget that would be spent regardless of sales volume. He figured the $0.76 per unit for general administrative and selling expense would just cover the advertising cost and could be allocated to advertising, since other SG&A costs would be fixed. When Ross showed his proposal to Adam, the latter flatly disagreed with the idea of cutting overhead. You start doing that," he said, "and pretty soon you've got lots of volume and no profit. You can't just wave your calculator like a wand over the numbers and have a product actually cost less. Furthermore, I think you haven't figured in the value of the options. There's no another timer like this on the market. I think we can put a factory price of $11.74 on it, and customers will be eager to buy it at $23.48." Tom, who had heard most of the discussion, said he thought the $11.74 factory price was a much better idea. Look," he said to Ross," if your breakdown of fixed and variable costs is right-and I think it is probably OK for the short runthen we'll only need to sell some smaller number of units at $11.74 to be as well off as we would be with your plan." --Well," said Adam, That may be right, but the more I look at this the more it seems to me that a little knowledge is a dangerous thing here. I don't think we really know how much the new timer is going to cost either in the short run or the long run." Exhibit le Purchased Direct Labore Exped. Supplies Overhead at Totale Partse 300% of De 1.11 0.29 0.022 0.12 0.022 0.182 0.03e 1.11e 0.59e 0.07e 1.77e 3.54 Basic Mechanism A2Be Purchased parts Fabricatione Machining Assembly Total A2B Addition to make new timere Purchased parts Fabricatione Machining Assemblye Total additions 0.24 0.03 je 1.32 0.1 0.24e 1.35e 0.1e 4.05 5.74 Total New Timere 1.35 1.94 0.17e 5.82e 9.28 Note: Fabrication work was punching our shapes, stamping t form pieces, and drilling hole, using both automatic and hand operated machines. The machining operations used lathes, milling machine, and grinders to make the gears, plates, holes, etc. with proper tolerances. Many of these used automatic feed mechanisms. Exhibit le Overhead item % of Direct Labore Ross's Estimate of Variable Amount- 35% 35% 15%e 15% 30% 30%e 55%e 0% 40% 0% Supplementary compensation for direct labor (Social Security, holidays, insurance etc.) Supervision (including supplemental compensation) Indirect labor (including supplemental compensation) Machine maintenance Machine depreciation Manufacturing engineering Plant administration (including supplemental compensation) Electricity Occupancy cost Total as percent of direct labore 35% 0% 40% 0% 10% 2%e 40% 0% 300%- 82% (Explanation: This says, for example, that total supervision cost of all departments for the year was expected to be 15% of the total direct labor cost for the year.) Ross's computation Total direct labor per timer=$1.94 (shown in Exhibit 1) 82% of $1.94= about $1.594 Therefore, incremental overhead per timer made would be $1.59. Questions Please answer the following questions: 1. Please analyze the context of the decision in light of your understanding of pricing strategies, cost behavior, and other relevant concepts in accounting. 2. What volume would have to be sold at the $11.74 factory price in order for Munzad to be as well off as it would be if it sold 50,000 units at $6.37? 3. If capacity for producing the A2B timer component is in fact limited, and therefore each sale of the household timer will eliminate the sale of an A2B component, how would you measure the household timer's profitability? 4. If, as Adam says, neither $11.74 nor $6.37 represents "the cost of the new timer, how would a better figure be computed? Munzad Clock Company (A)" As Adam Munzad, president of the Munzad Clock Company, stared at the numbers compiled by his controller, Tom Moody, and his sales manager Ross Taylor, the look on his face was one of confusion. The more I look at this the more it looks like we really don't know how much this new household timer is going to cost. We need to get a better handle on the costs of this thing or we will never abe able to decide how to price it." The Company Munzad Clock Company was started by Adam Munzad, the company's president, in 1995. In 2008. Munzad had sold out to Meghna Appliance Corporation, but he remained with the company as Munzad Clock's president. Originally, Munzad Clock made decorative electric clocks, but by 2002 Adam had decided he was much better at making the works than the decorations. So the company shifted to making accurate, durable, but inexpensive electric timing mechanisms. The company now made only three basic models, differing in size and strength. Slight modifications were made to fit each customer's needs. Sales had grown to over $50 million, and timing mechanisms were made to fit each customer's needs. Sales had grown to over $50 million, and the timing mechanisms were made entirely for producers of timed electrical appliances. About half of Munzadis output went to Meghna appliance and about half to other companies. The new household timing device It all started because sometime over the 2010 Labor Day weekend, Adam Munzad's house was burgled while he and his family were enjoying the last days of their summer vacation. Thereafter, though he knew he was closing the proverbial barn door after the cow had gone, Adam did a number of things to try to prevent a repetition Besides improving locks, he bought two timers that could be set to run on house lights in the evening. That is what gave him the idea to make a better timing mechanism for household use, one that head two features that he thought made his timer superior to those currently on the market. The Munzad timer had two options: a 48-hour cycle (so that lights would not turn on and off at the same time each day), or two different 24-hour cycles, so that one timer could operate two lights, each on a different 24-hour cycle. The design of these features was quite simple. There were two different 24-hour cycles, and for the 48-hour option, the timer switched back and forth. Adam's sales manager, Ross Taylor, was not sure how or valuable these options would be to the potential customer. Furthermore, this complete product would have to be sold through wholesalers and manufacturers representatives, which were new to Muuzad Clock. Price, he thought, would be an important factor since other timers were on the market. Pricing the new household timing device Adam asked his controller, Tom Moody, to put some cost figures together. Tom presented the table show in Exhibit 1. The basic timing mechanism, Model A2B, was Mynzadis highest volume product, which showed a cost of $3.54. To make the timer that Adam had designed would cost about $9.28. No more machining would be required, but a little fabrication work and a number of wiring and assembly operations would be necessary. Tom had checked on available capacity before computing his costs. As it happened adequate space for the timer's assembly had just become available because the company had shifted from having one warehouse for finished goods at the plant, to tow warehouses, one in Pennsylvania and the other in Texas. Making the warehouse into an assembly area would require some tables, lighting, and small tools but no major capital expenditure. About $20,000 ought to cover it, Tom thought. Adam asked Tom to show his figures to Ross. On the seeing the $9.28 production cost, Ross did the following rough calculation using normal mark-ups to see what this cost might indicate for a retail selling price. $9.282 1.39 10.67e 1.07 Total manufacturing coste Selling, General and Administration (15% of cost) Total Costs Profit (10% of cost) Factory Price Wholesale, Retain and Distribution (50% of Selling Price) Estimated Retail Selling Price 11.74 11.74 $23.48 "Holy Smokes," said Ross to himself, "we'll never sell any at that price." He knew that the similar model by the closest competitor was selling at $15.98, and others were not more than dollar or two away from that. He studied the controller's numbers. "Tom," he said, "isn't most of this overhead fixed? You have used a plant-wide rate for as long as I can remember, and that seems to have worked OK. But if we are just adding on a little fancy assembly stuff to sell more timing mechanisms, that isn't really going to increase our overhead, is it?" "Well, yes and 110," said Tom. "Any one increment in volume won't necessarily increase overhead by 300 percent of the direct labor that increment, but somewhere along line, overhead is going to increase." To explain what overhead consisted of. Tom showed Ross the schedule shown in Exhibit 2.- Ross asked Tom a few questions about the list of overhead costs and then computed his own figures, shows as the right-hand column in Exhibit 2. He concluded that only about $1.59 of the $5.84 of overhead cost was really. variable, so he thought $4.25 should be considered fixed and not relevant to this decision. In that case, he thought the cost and selling price figures should look like this: $9.28 4.25e Total manufacturing coste Fixed manufacturing costse Variable costs for the new timere Selling, General and Administration (15% of cost) 5.03 0.76 5.79 0.58 Profit (10% of cost) Factory price 6.374 6.37e Wholesale, Retail and Distribution (50% of Selling Price) Estimated retail selling price $12.742 At a factory price of $6.37, Ross figured they could 50,000 timers. He figured there should be a $38.000 advertising budget that would be spent regardless of sales volume. He figured the $0.76 per unit for general administrative and selling expense would just cover the advertising cost and could be allocated to advertising, since other SG&A costs would be fixed. When Ross showed his proposal to Adam, the latter flatly disagreed with the idea of cutting overhead. You start doing that," he said, "and pretty soon you've got lots of volume and no profit. You can't just wave your calculator like a wand over the numbers and have a product actually cost less. Furthermore, I think you haven't figured in the value of the options. There's no another timer like this on the market. I think we can put a factory price of $11.74 on it, and customers will be eager to buy it at $23.48." Tom, who had heard most of the discussion, said he thought the $11.74 factory price was a much better idea. Look," he said to Ross," if your breakdown of fixed and variable costs is right-and I think it is probably OK for the short runthen we'll only need to sell some smaller number of units at $11.74 to be as well off as we would be with your plan." --Well," said Adam, That may be right, but the more I look at this the more it seems to me that a little knowledge is a dangerous thing here. I don't think we really know how much the new timer is going to cost either in the short run or the long run." Exhibit le Purchased Direct Labore Exped. Supplies Overhead at Totale Partse 300% of De 1.11 0.29 0.022 0.12 0.022 0.182 0.03e 1.11e 0.59e 0.07e 1.77e 3.54 Basic Mechanism A2Be Purchased parts Fabricatione Machining Assembly Total A2B Addition to make new timere Purchased parts Fabricatione Machining Assemblye Total additions 0.24 0.03 je 1.32 0.1 0.24e 1.35e 0.1e 4.05 5.74 Total New Timere 1.35 1.94 0.17e 5.82e 9.28 Note: Fabrication work was punching our shapes, stamping t form pieces, and drilling hole, using both automatic and hand operated machines. The machining operations used lathes, milling machine, and grinders to make the gears, plates, holes, etc. with proper tolerances. Many of these used automatic feed mechanisms. Exhibit le Overhead item % of Direct Labore Ross's Estimate of Variable Amount- 35% 35% 15%e 15% 30% 30%e 55%e 0% 40% 0% Supplementary compensation for direct labor (Social Security, holidays, insurance etc.) Supervision (including supplemental compensation) Indirect labor (including supplemental compensation) Machine maintenance Machine depreciation Manufacturing engineering Plant administration (including supplemental compensation) Electricity Occupancy cost Total as percent of direct labore 35% 0% 40% 0% 10% 2%e 40% 0% 300%- 82% (Explanation: This says, for example, that total supervision cost of all departments for the year was expected to be 15% of the total direct labor cost for the year.) Ross's computation Total direct labor per timer=$1.94 (shown in Exhibit 1) 82% of $1.94= about $1.594 Therefore, incremental overhead per timer made would be $1.59. Questions Please answer the following questions: 1. Please analyze the context of the decision in light of your understanding of pricing strategies, cost behavior, and other relevant concepts in accounting. 2. What volume would have to be sold at the $11.74 factory price in order for Munzad to be as well off as it would be if it sold 50,000 units at $6.37? 3. If capacity for producing the A2B timer component is in fact limited, and therefore each sale of the household timer will eliminate the sale of an A2B component, how would you measure the household timer's profitability? 4. If, as Adam says, neither $11.74 nor $6.37 represents "the cost of the new timer, how would a better figure be computed

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals Of Corporate Finance

Authors: Jonathan Berk, Peter DeMarzo, Jarrad Harford

5th Edition

0135811600, 978-0135811603