Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please provide solution with all workings. I will upvote. Thanks in advance. Monte Company acquired 70% of the stock of Mo Company on 1 January

Please provide solution with all workings. I will upvote. Thanks in advance.

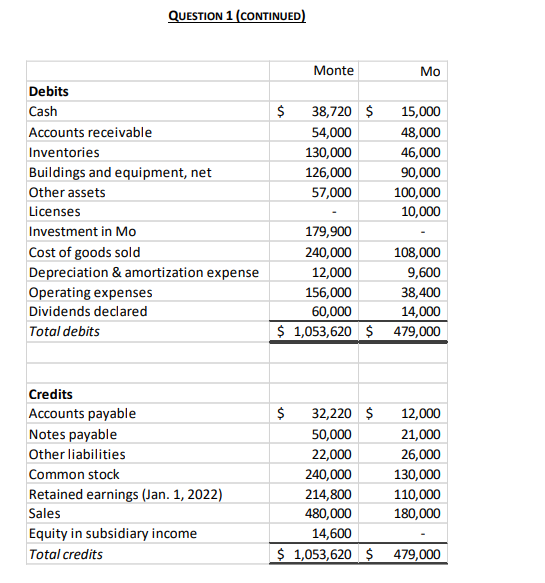

Monte Company acquired 70% of the stock of Mo Company on 1 January 2018, for $150,000. On this date, the balances of Mo's stockholders' equity accounts were: Common Stock, $130,000, and Retained Earnings, $14,000. On 1 January 2018, the market value for the 30% of shares not purchased by Monte was $63,800. On 1 January 2018, Mo's recorded book values were equal to fair values for all items except: (1) accounts receivable had a book value of $40,000 and a fair value of $36,000, (2) buildings and equipment, net, had a book value of $35,000 and a fair value of $53,000, (3) the licenses intangible asset had a book value of $10,000 and a fair value of $52,000, and (4) notes payable had a book value of $24,000 and a fair value of $18,000. Both companies use the FIFO inventory method and sell all of their inventories at least once per year. The net balance of trade receivables are collected in the following year. On the acquisition date, the subsidiary's buildings and equipment, net, had a remaining useful life of 6 years, licenses had a remaining useful life of 7 years, and notes payable had a remaining term of 4 years. On 1 January 2021, Monte sold a building to Mo for $65,000. On this date, the building was carried on Monte's books (net of accumulated depreciation) at $50,000. Both companies estimated that the building has a remaining life of 6 years on the intercompany sale date, with no salvage value. Each company routinely sells merchandise to the other company, with a gross profit margin of 25 percent (regardless of the direction of the sale). During 2022, intercompany sales amount to $15,000, of which $8,000 of merchandise remains in the ending inventory of the parent. On 31 December 2022, $4,000 of these intercompany sales remained unpaid. Additionally, the subsidiary's 31 December 2021 inventory includes $12,000 of merchandise purchased in 2021 from the parent. During 2021, intercompany sales amount to $20,000, and on 31 December 2021, $7,000 of these intercompany sales remained unpaid. Monte uses the equity method to account for its investment in Mo. The pre-closing trial balances for the two companies for the year ended 31 December 2022, are provided on the following page. Required: Prepare a consolidation worksheet and the appropriate eliminating entries to determine consolidated balances for external financial reporting as of 31 December 2022. QUESTION 1 (CONTINUED) Monte Debits Cash Accounts receivable Inventories Buildings and equipment, net Other assets Licenses Investment in Mo Cost of goods sold Depreciation & amortization expense Operating expenses Dividends declared Total debits $ 38,720 $ 15,000 54,000 48,000 130,000 46,000 126,000 90,000 57,000 100,000 10,000 179,900 240,000 108,000 12,000 9,600 156,000 38,400 60,000 14,000 $ 1,053,620 $ 479,000 Credits Accounts payable Notes payable Other liabilities Common stock Retained earnings (Jan. 1, 2022) Sales Equity in subsidiary income Total credits $ 32,220 $ 12,000 50,000 21,000 22,000 26,000 240,000 130,000 214,800 110,000 480,000 180,000 14,600 $ 1,053,620 $ 479,000 Monte Company acquired 70% of the stock of Mo Company on 1 January 2018, for $150,000. On this date, the balances of Mo's stockholders' equity accounts were: Common Stock, $130,000, and Retained Earnings, $14,000. On 1 January 2018, the market value for the 30% of shares not purchased by Monte was $63,800. On 1 January 2018, Mo's recorded book values were equal to fair values for all items except: (1) accounts receivable had a book value of $40,000 and a fair value of $36,000, (2) buildings and equipment, net, had a book value of $35,000 and a fair value of $53,000, (3) the licenses intangible asset had a book value of $10,000 and a fair value of $52,000, and (4) notes payable had a book value of $24,000 and a fair value of $18,000. Both companies use the FIFO inventory method and sell all of their inventories at least once per year. The net balance of trade receivables are collected in the following year. On the acquisition date, the subsidiary's buildings and equipment, net, had a remaining useful life of 6 years, licenses had a remaining useful life of 7 years, and notes payable had a remaining term of 4 years. On 1 January 2021, Monte sold a building to Mo for $65,000. On this date, the building was carried on Monte's books (net of accumulated depreciation) at $50,000. Both companies estimated that the building has a remaining life of 6 years on the intercompany sale date, with no salvage value. Each company routinely sells merchandise to the other company, with a gross profit margin of 25 percent (regardless of the direction of the sale). During 2022, intercompany sales amount to $15,000, of which $8,000 of merchandise remains in the ending inventory of the parent. On 31 December 2022, $4,000 of these intercompany sales remained unpaid. Additionally, the subsidiary's 31 December 2021 inventory includes $12,000 of merchandise purchased in 2021 from the parent. During 2021, intercompany sales amount to $20,000, and on 31 December 2021, $7,000 of these intercompany sales remained unpaid. Monte uses the equity method to account for its investment in Mo. The pre-closing trial balances for the two companies for the year ended 31 December 2022, are provided on the following page. Required: Prepare a consolidation worksheet and the appropriate eliminating entries to determine consolidated balances for external financial reporting as of 31 December 2022. QUESTION 1 (CONTINUED) Monte Debits Cash Accounts receivable Inventories Buildings and equipment, net Other assets Licenses Investment in Mo Cost of goods sold Depreciation & amortization expense Operating expenses Dividends declared Total debits $ 38,720 $ 15,000 54,000 48,000 130,000 46,000 126,000 90,000 57,000 100,000 10,000 179,900 240,000 108,000 12,000 9,600 156,000 38,400 60,000 14,000 $ 1,053,620 $ 479,000 Credits Accounts payable Notes payable Other liabilities Common stock Retained earnings (Jan. 1, 2022) Sales Equity in subsidiary income Total credits $ 32,220 $ 12,000 50,000 21,000 22,000 26,000 240,000 130,000 214,800 110,000 480,000 180,000 14,600 $ 1,053,620 $ 479,000Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Measurement And Internal Audit Operations

Authors: Andrew Fight

1st Edition

184112401X, 978-1841124018