Answered step by step

Verified Expert Solution

Question

1 Approved Answer

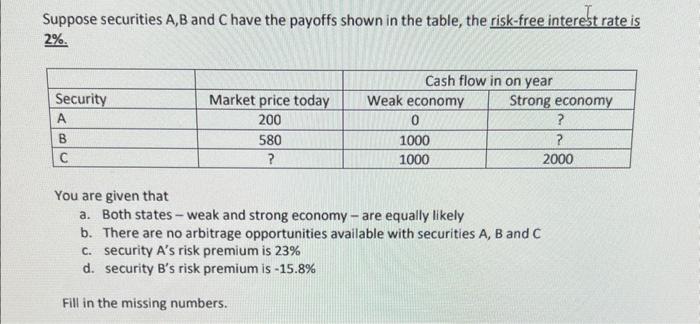

Please provide solutions Suppose securities A,B and C have the payoffs shown in the table, the risk-free interest rate is 2%. You are given that

Please provide solutions

Suppose securities A,B and C have the payoffs shown in the table, the risk-free interest rate is 2%. You are given that a. Both states - weak and strong economy - are equally likely b. There are no arbitrage opportunities available with securities A, B and C c. security A's risk premium is 23% d. security B 's risk premium is 15.8% Fill in the missing numbers Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Corporate Governance In Japan Institutional Change And Organizational Diversity

Authors: Masahiko Aoki , Gregory Jackson, Hideaki Miyajima

1st Edition

0199284520,0191536385